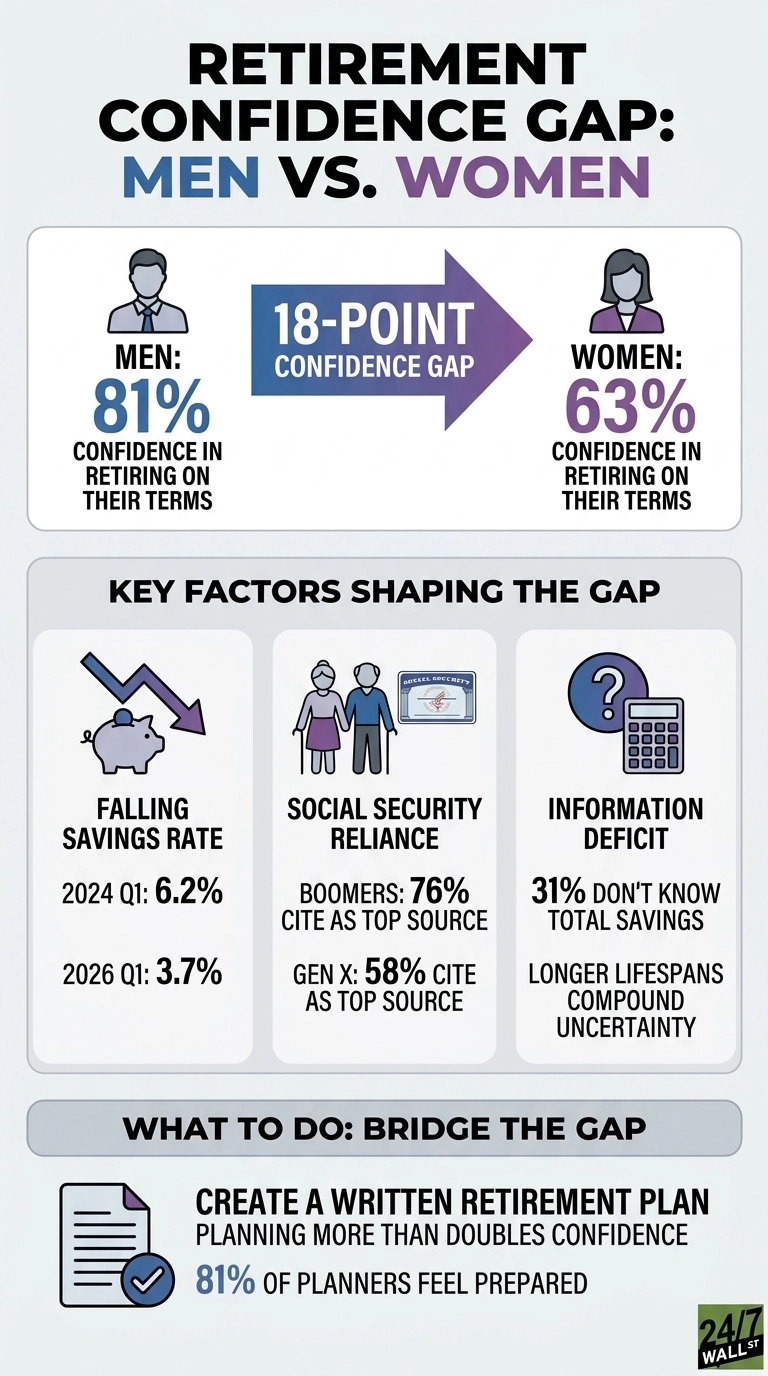

Fidelity’s 2026 Retirement Study captures a confidence gap that arrives years before any account statement confirms it. Men report 81% confidence in retiring on their own terms, while women report 63%. This 18-percentage-point gap tracks a set of structural conditions that compound over a working life and then compound again in retirement.

The income side of the equation explains part of the gap with average hourly earnings reached $37.53 in May 2026, up from $36.28 a year earlier, but that headline figure masks the persistent earnings differential between men and women that determines lifetime contributions to 401(k)s, IRAs, and Social Security. A wage gap measured in single digits per hour becomes a six-figure gap over a 40-year career, and widens further when career interruptions for caregiving reduce both the number of contribution years and the subsequent wage trajectory.

The savings environment is not helping, as the personal savings rate fell from 6.2% in the first quarter of 2024 to 3.7% in the first quarter of 2026, even as per capita disposable income rose to $68,359. Households are spending a larger share of their earnings, leaving less room for retirement contributions. Social Security transfers totaled $1.6 trillion in the first quarter of 2026, with Medicare adding another $1.3 trillion, underscoring how central these programs already are to household income.

That dependence on Social Security falls unevenly across groups. Among Boomers, 76% cite Social Security as a top source of retirement income. Meanwhile, younger generations lean most heavily on workplace plans, with 58% of Gen X, 48% of Millennials, and 44% of Gen Z. Women, who tend to live longer and have lower lifetime earnings, receive smaller Social Security checks for more years. The same benefit that anchors a male retiree’s plan may need to stretch across many more years for a female retiree, and the dollar amount itself is typically smaller to begin with.

Planning Is the Variable That Moves

The Fidelity data point to one factor that does shift outcomes: respondents with a retirement plan are more than twice as likely to feel confident about their prospects. Among retirees, 81% with a plan say they have enough money to last their lifetimes, compared with 45% without a plan. That 36-point difference inside the retiree population suggests the confidence gap reflects actual preparedness rather than disposition.

The information deficit is significant, with Roughly 31% of respondents not knowing how much they will have saved by retirement, a vulnerability that compounds with longer life expectancies. Without a target balance, withdrawal rate, or claiming strategy, the variables that drive retirement income remain undefined, and the gap between men’s and women’s confidence levels has room to widen further.

The Broader Backdrop

The macro environment is not adding a cushion, as the University of Michigan consumer sentiment reached 49.8 in April 2026, the lowest reading in the prior 12 months, and unemployment has drifted from 4.0% in January 2025 to 4.3% in May 2026. Core PCE, the Federal Reserve’s preferred inflation gauge, sat at 129.63 in April 2026, up from 126.1 a year earlier, eroding the real value of any fixed retirement income stream. The federal funds rate has fallen to 3.75% from 4.5% a year ago, reducing the yield available on the conservative savings vehicles that retirees often lean on.

What the Data Shows

The 18-point confidence gap exists before account balances confirm it because the inputs that produce it are already in place: lower lifetime earnings, longer expected lifespans, lower planning rates, and heavier reliance on Social Security benefits stretched over more years. The Fidelity finding that a written plan more than doubles confidence points to where the gap narrows. Closing the gap requires deliberate planning, and the macro backdrop of falling savings rates, elevated inflation, and softer sentiment continues to work against that effort.

Contact [email protected] for any questions or corrections.