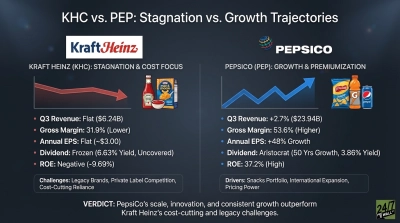

The recent market downturn has been rough for many sectors but, as implied in the name, consumer defensive stocks have held up reasonably well. One big Wall Street name thinks it has found a big winner within the group that could benefit greatly going forward.

[in-text-ad]

BMO Capital’s Kenneth Zaslow was the lead analyst on the call on Kraft Heinz Co. (NASDAQ: KHC | KHC Price Prediction). Basically, as a company that puts food on the shelves for many grocery chains across the nation, it can stand to benefit from some supply chain constraints and inflation because most of the goods Kraft Heinz produces are inelastic in nature.

[nativounit]

For the 2021 fiscal year, during the pandemic, Kraft Heinz pulled in just over $26 billion in revenue. This is only slightly lower than 2020 revenues, and about a quarter of a billion less than 2018. While the pandemic has made many of these companies a lot leaner and meaner, it is likely that Kraft Heinz has managed its portfolio of brands in such a way to set up for future success.

In terms of the actual call, BMO Capital upgraded the stock from Market Perform to Outperform. The unchanged price target of $46 suggests over 25% upside from the most recent closing price of $36.61.

[wallst_email_signup]

According to Zaslow, the company’s “strategic evolution” continues to be overlooked by the market, which creates a “compelling investment opportunity.” Even after exceeding expectations for eight consecutive quarters, increasing its long-term growth algorithm to align with its peers, and reducing its leverage to just over three-times, Kraft’s valuation discount to its peers expanded in 2022. Zaslow believes the company should benefit from moderating share losses, a “bifurcated consumer, a more resilient portfolio, strategic revenue management, and an improved supply chain.”

[recirclink id=1141600]

Kraft Heinz traded at $37.35 early Thursday, in a 52-week range of $32.78 to $44.87. The consensus price target is $42.88. The stock is up about 4% year to date, but down more than 6% in the past 52 weeks.

Contact [email protected] for any questions or corrections.