Kraft Heinz (NASDAQ: KHC | KHC Price Prediction) and PepsiCo (NASDAQ: PEP) both beat Q3 2025 earnings, but the results highlight two packaged food giants on starkly different trajectories. Kraft Heinz delivered a 4.47% surprise on $0.61 EPS while PepsiCo posted a 1.33% beat at $2.29 per share.

One Delivers Profit Growth, the Other Delivers Beats Without Progress

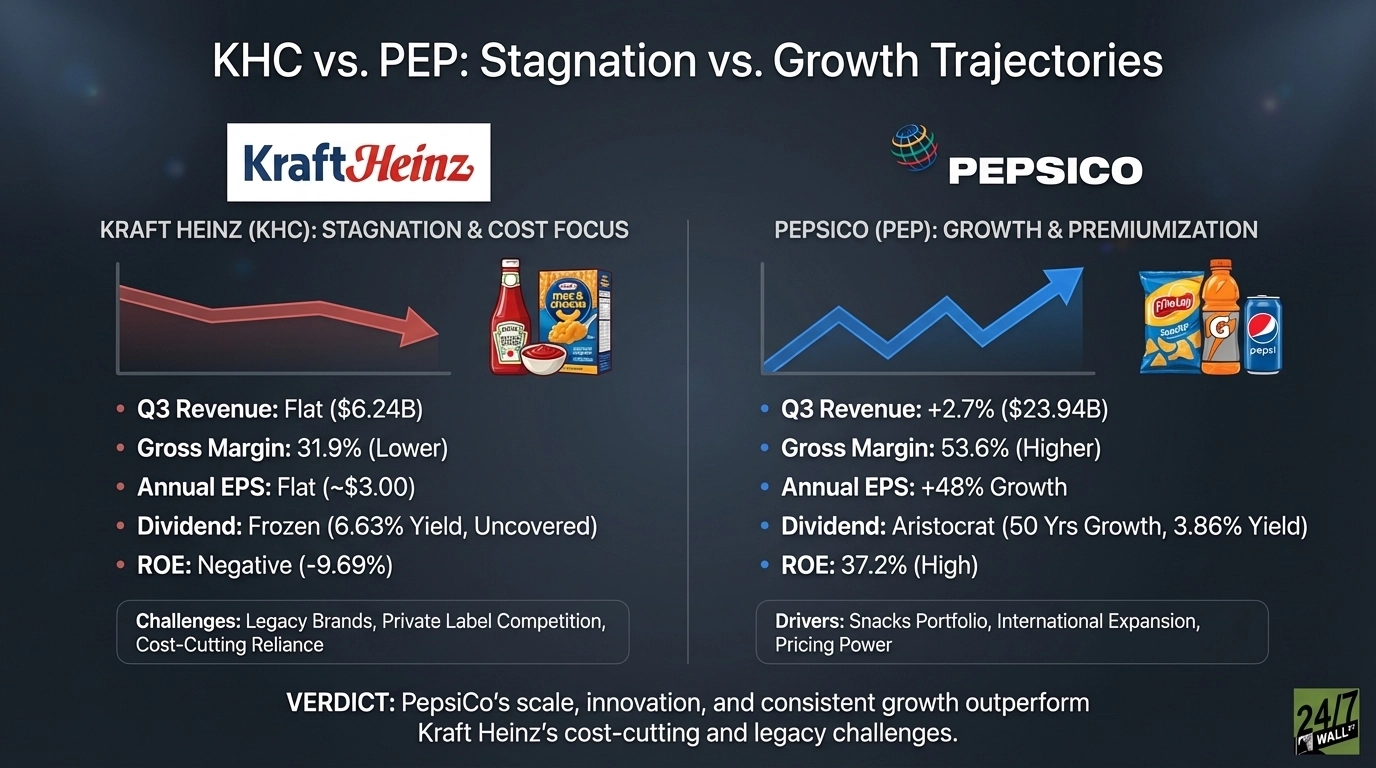

PepsiCo’s Q3 showed revenue climbing 2.7% year over year to $23.94 billion, driven by its Frito-Lay snacks portfolio and steady beverage demand. Gross margins reached 53.6%, reflecting pricing power across brands like Doritos, Cheetos, and Gatorade. Operating income hit $3.57 billion with a 14.9% margin. Management highlighted premiumization in snacks and international expansion as core drivers, with CFO Stephen Schmitt noting strength in convenience channels.

Kraft Heinz posted Q3 revenue of $6.24 billion, essentially flat, with gross margins at 31.9%. Operating income reached $1.03 billion on a 16.4% margin. The company beat estimates for the fourth consecutive quarter, yet annual EPS has stagnated between $2.78 and $3.06 since 2021. Brands like Oscar Mayer and Philadelphia cream cheese face intense private label competition, and management has struggled to reignite growth beyond cost-cutting.

| Metric | Kraft Heinz | PepsiCo |

| Q3 Gross Margin | 31.9% | 53.6% |

| Operating Margin | 16.4% | 14.9% |

| Annual EPS Growth (2020-2024) | Flat (~$2.80-$3.06) | +48% ($5.52 to $8.16) |

Scale, Portfolio Breadth, and Strategic Execution Separate Them

PepsiCo operates with nearly seven times Kraft Heinz’s market capitalization at $197.5 billion. Its dual-pillar strategy balancing beverages and snacks provides resilience. Frito-Lay alone generates higher margins than most of Kraft Heinz’s entire portfolio. PepsiCo’s return on equity stands at 37.2%, demonstrating efficient capital deployment, while Kraft Heinz shows negative 9.69% ROE due to losses.

Kraft Heinz relies heavily on legacy packaged foods facing secular headwinds. The company cut its dividend 36% in 2019 and hasn’t raised it since, leaving the payout frozen at $0.40 quarterly for over six years. With trailing twelve-month EPS of negative $3.71, the $1.60 annual dividend isn’t covered by earnings. PepsiCo has increased dividends for 50 consecutive years as a Dividend Aristocrat, with a sustainable 3.86% yield backed by positive $5.26 EPS.

Insider activity tells a story too. PepsiCo insiders made 20 acquisitions in recent months, including a $7 million purchase by CFO Schmitt. Kraft Heinz recorded just one transaction, a stock grant to a supply chain executive.

The Next Test Is Whether Kraft Heinz Can Prove Turnaround Credibility

PepsiCo faces questions about sustaining snack pricing power as inflation moderates and private label gains share. International markets, particularly Latin America and Asia, will determine whether growth can accelerate beyond low single digits. Product innovation cycles in zero-sugar beverages and better-for-you snacks matter for maintaining premiums.

Kraft Heinz needs to show it can grow revenue, not just beat lowered estimates. The company’s 10-year stock decline of 46% reflects investor skepticism that management can reverse market share losses in core categories.

Key Considerations for Evaluating These Consumer Staples

PepsiCo offers a 3.86% yield backed by 50 consecutive years of dividend increases and positive earnings of $5.26 per share. The company has demonstrated EPS growth of 48% over four years and maintains a return on equity of 37.2%. Kraft Heinz provides a higher 6.63% yield, though the dividend has been frozen since 2019 and current TTM EPS is negative $3.71. The $1.60 annual dividend is not covered by earnings. Evaluating these stocks involves different risk-reward profiles based on dividend sustainability, growth trajectories, and turnaround execution risk. PepsiCo’s larger scale, diversified portfolio, and consistent profitability contrast with Kraft Heinz’s distressed valuation, higher yield, and need to prove revenue growth capability beyond cost management.

Contact [email protected] for any questions or corrections.