Oklo Inc. (NYSE: OKLO) Earnings Live: What You Need to Follow

Live Updates

Controlled cash burn

Q1 cash burn was $12.2M, consistent with full-year forecast of $65–80M. Cash and marketable securities ended at $260.7M.

There’s no sign of capital pressure, and the company is progressing both reactor and isotope licensing within this base.

Why it matters: Oklo may not need to raise capital before 2026 — a rarity for early-stage energy tech firms.

Operational Milestones

-

Aurora-INL Project:

-

Completed site drilling campaign, including seismic and geophysical surveys

-

Finalized environmental and site access agreements with DOE and INL

-

Still targeting late 2027 / early 2028 plant operation start

-

-

Licensing Progress:

-

Submitted licensed operator topical report to NRC

-

Initiated Phase 1 of pre-application readiness for Combined License Application (COLA)

-

-

Fuel & Supply Chain:

-

Fuel secured for first Aurora unit

-

Nearing submission of licensing plan for new Oklo Fuel Foundry

-

Reaffirmed strategic HALEU supply partnership with Centrus

-

-

Radioisotope Expansion via Atomic Alchemy:

-

Demo project expected to deliver first revenue by early-to-mid 2026

-

VIPR® commercial production facility licensing to begin in 2025

-

Over 20 isotopes listed as active commercial targets; customer LOIs already signed

-

First take of Q1 numbers

Financials

-

Revenue: Not disclosed (still pre-commercial)

-

Net Loss: $9.8 million, improved from $(24.0) million in Q1 2024

-

Loss Per Share: $(0.07), vs. est. of $(.10)

-

Cash Burn from Operations: $12.2 million

-

Cash & Marketable Securities: $260.7 million as of March 31, 2025

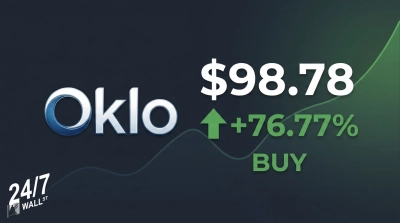

Oklo Stock Up 11% on the day, results coming shortly

Oklo stock soared today while investors await earnings results. The numbers should be in shortly followed by a 5 p.m. Eastern Time conference call.

Will have updates as numbers come in.

Insider trades this past quarter

Since March 2025, Oklo insiders have been active — including open market sales, option exercises, and retained stock events. Co-founder and CEO Jacob DeWitte sold 216,000 shares at $21.80–$26.00 per share. CFO Craig Bealmear also executed a derivative-based sale of 17,413 shares.

Critically, these transactions occurred:

-

Post-SPAC listing, where new liquidity windows opened

-

During periods of continued insider stock retention

-

As part of derivative exercises, which typically trigger planned selling for tax or liquidity reasons

The bigger picture is that Oklo insiders still control 10M+ shares each, with no signs of exit-level divestments. And unlike many early-stage companies, Oklo’s leadership has tied compensation heavily to long-term equity performance and reactor milestone progress.

For long-term investors, the key is not just who’s selling — it’s who’s still holding. In Oklo’s case, insiders remain fully engaged, and selling is routine — not reactive.

Oklo share price soaring before earnings release

Share of Oklo are now up 12% heading into earnings in 1 1/2 hours.

While Oklo’s business is often described as “advanced nuclear,” it’s increasingly clear the company has two separate product lines forming in parallel:

-

Reactor projects (Aurora, 75MW+ commercial rollouts)

-

Radioisotope production (via Atomic Alchemy acquisition)

The reactor segment is capital intensive, license-gated, and tied to long project timelines — but also has massive TAM through power contracts. Meanwhile, the isotope segment offers near-term commercialization, with lower capex and a growing market in medicine, semiconductors, and space.

Tonight’s call needs to clarify:

-

Revenue potential from isotope demo sales in 2025–26

-

Updated buildout timelines for 75MW reactor units

-

How Oklo allocates capital between these parallel paths

If both lines are moving on schedule, Oklo may emerge as the only advanced fission company with revenue before 2027.

Fuel Access and HALEU Scale Is Quietly Becoming a Moat

On Oklo’s most recent call, the company revealed it has not only secured fuel for its first Aurora core, but also formalized a long-term HALEU supply relationship with Centrus—a rare feat in the advanced nuclear space.

“Centrus is already producing HALEU today and continues to scale their production… This ensures a scalable domestic source.”

In a sector where most peers are stuck in theoretical designs or waiting on fuel policy, Oklo’s dual-track on fuel access (initial core + long-term supply) is a major strategic differentiator. If reiterated clearly tonight, it could solidify investor conviction in 2027 deployment feasibility.

What investors want to hear in tonight's call

Oklo’s Q1 isn’t about revenue or profit — it’s about momentum. Investors are looking for concrete signs the company is on track for 2027 deployment and capital-efficient growth. Here’s what the call needs to affirm:

-

Combined License Application (COLA) remains on track for 2025 submission. Any slippage here would undercut the whole roadmap.

-

Fuel procurement remains de-risked. The company previously said it has secured fuel for the first Aurora plant. That must remain true.

-

Customer pipeline >14GW is holding and advancing. Investors want clarity on the pace and stage of Switch, Equinix, and Prometheus LOIs.

-

Atomic Alchemy integration and radioisotope plan are progressing. This provides a non-reactor revenue stream and shortens the value curve.

Pre-Revenue but Not Pre-Expectations

Oklo remains a pre-commercial energy company, but the Street still has firm expectations heading into Q1.

Here’s the current snapshot:

| Metric | Consensus |

|---|---|

| Revenue | $1.5 million |

| EPS | –$0.11 |

| Cash Burn (Q1 est.) | $15–20 million |

The small revenue figure is likely tied to grants or early milestone-based contracts. However, most investors will focus on liquidity levels, operating spend, and updates to deployment and licensing milestones. Analysts expect cash to remain above $250 million, and spending to increase slightly due to Aurora site prep, NRC licensing, and Atomic Alchemy integration. Commentary on Combined License Application timing and early customer contracts (Switch, Prometheus, Equinix) will be more important than EPS noise.

Oklo (NYSE: OKLO) reports first-quarter results this evening with investor focus centered on regulatory progress, early-stage commercial traction, and its growing clean energy pipeline. While the company is still pre-revenue, analysts will be watching for updates tied to its massive data center customer agreements and timelines for its first commercial deployment at Idaho National Lab.

Consensus calls for –$0.11 in EPS and $1.5 million in revenue, with expectations that any top-line results will stem from grant or milestone revenue. What matters more tonight is whether Oklo demonstrates progress across its six strategic fronts: project execution, reactor licensing, fuel access, customer pipeline, strategic partnerships, and cash efficiency.

Investors are especially attuned to timelines around the Combined License Application (COLA) and whether Oklo’s Aurora plant remains on track for deployment by 2027–2028. Commentary on its 75MW modular configuration, fuel security, and the Switch and Equinix customer pipeline will shape the stock’s credibility going into 2H 2025.

Contact [email protected] for any questions or corrections.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall Street