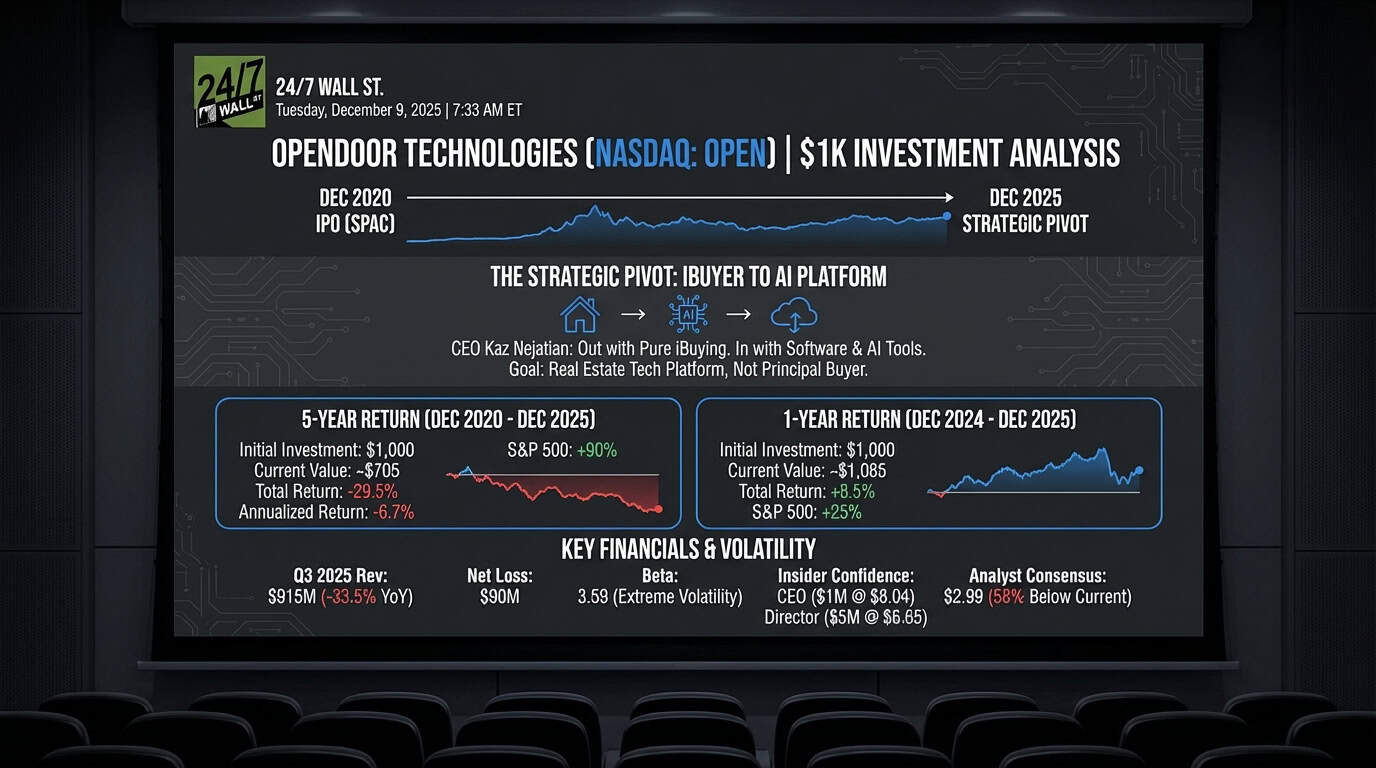

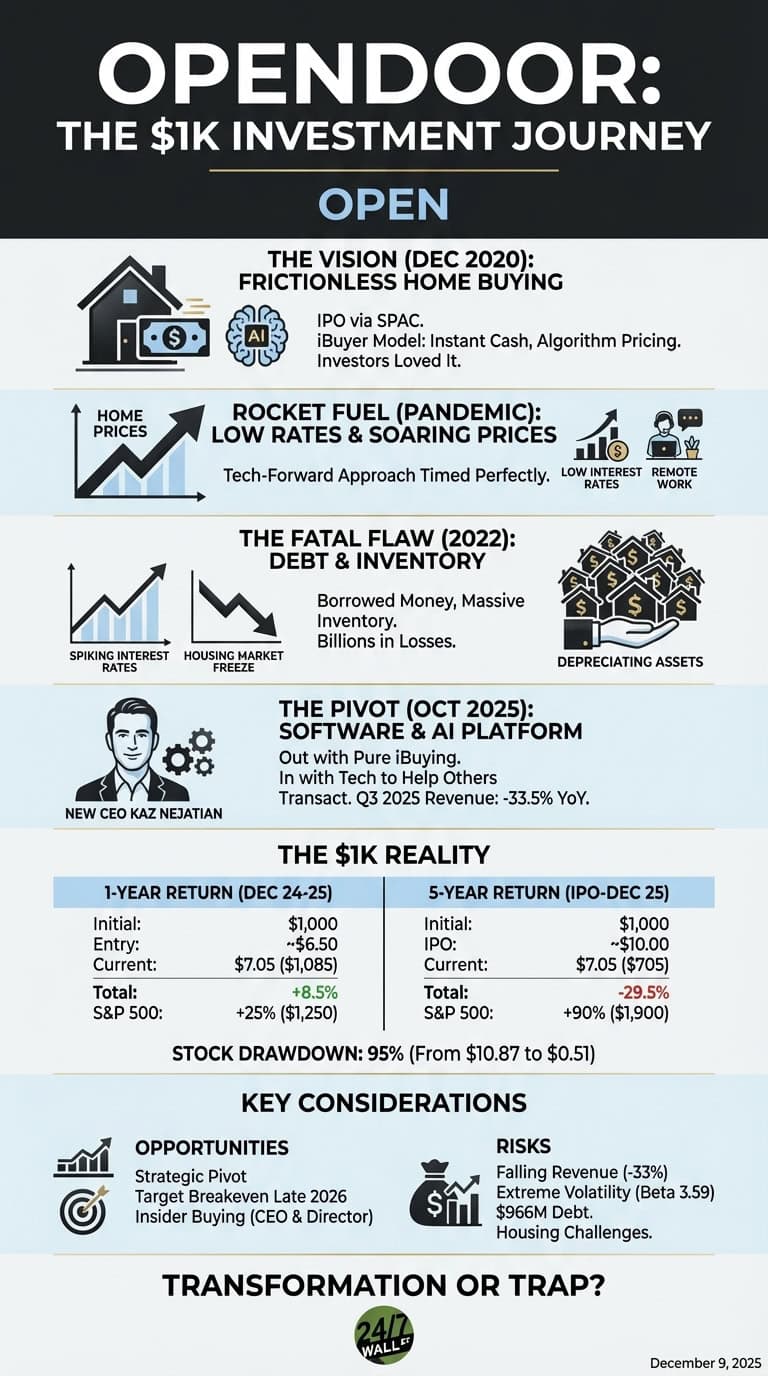

Opendoor Technologies (NASDAQ: OPEN) went public via SPAC merger in December 2020 with a bold vision: use technology to eliminate friction from home buying and selling. The iBuyer model promised homeowners instant cash sales while buyers browsed algorithmically priced homes online. Investors initially loved it.

The pandemic housing boom was rocket fuel. Low rates and remote work sent home prices soaring, and Opendoor’s tech-forward approach seemed perfectly timed. But the model had a fatal flaw: buying massive inventory with borrowed money, then reselling quickly at a profit. When interest rates spiked in 2022 and the housing market froze, Opendoor got caught holding billions in depreciating assets. Losses ballooned to over $1 billion annually.

In October 2025, new CEO Kaz Nejatian immediately pivoted strategy. Out with pure iBuying, in with software and AI tools. The goal: become a technology platform helping others transact real estate, not just a principal buyer. Revenue in Q3 2025 dropped 33.5% year over year to $915 million, with a net loss of $90 million that quarter.

From $1,000 to What?

Because Opendoor only went public in late 2020, we can’t calculate 10-year returns. Here’s what your $1,000 would look like at different entry points:

1-Year Return (Dec 2024 to Dec 2025)

- Initial Investment: $1,000

- Estimated Entry Price: ~$6.50

- Current Value (at $7.05): ~$1,085

- Total Return: +8.5%

- S&P 500 (same period): ~$1,250 (+25%)

5-Year Return (Dec 2020 IPO to Dec 2025)

- Initial Investment: $1,000

- Estimated IPO Price (adjusted): ~$10.00

- Current Value (at $7.05): ~$705

- Total Return: -29.5%

- Annualized Return: -6.7%

- S&P 500 (same period): ~$1,900 (+90%)

Early investors who bought at IPO have lost nearly 30%, while the S&P 500 nearly doubled. Even recent buyers have underperformed dramatically. The stock hit $10.87 in its 52-week high before collapsing to $0.51, a 95% drawdown.

Rising rates killed the iBuyer model’s economics. Opendoor’s beta of 3.59 means it’s nearly four times more volatile than the market, and that volatility has mostly pointed down. The company has never turned a profit, burning through over $1 billion in cumulative losses.

Key Considerations for Investors

The company’s strategic pivot presents both opportunities and risks. Opendoor has $962 million in cash but also $966 million in debt, targeting breakeven by late 2026. The new platform model could transform margins if successfully scaled. Analysts have set a consensus target of $2.99, 58% below current levels. However, insider activity shows confidence: CEO Nejatian purchased $1 million worth at $8.04 in November, and Director Eric Wu deployed $5 million at $6.65 in September.

Challenges remain significant. Revenue fell 33% year over year, and the company has missed earnings expectations in recent quarters. The stock’s beta of 3.59 indicates extreme volatility, nearly four times the market average. The housing market remains challenged, and inventory levels are low, limiting near-term growth potential.

Contact [email protected] for any questions or corrections.