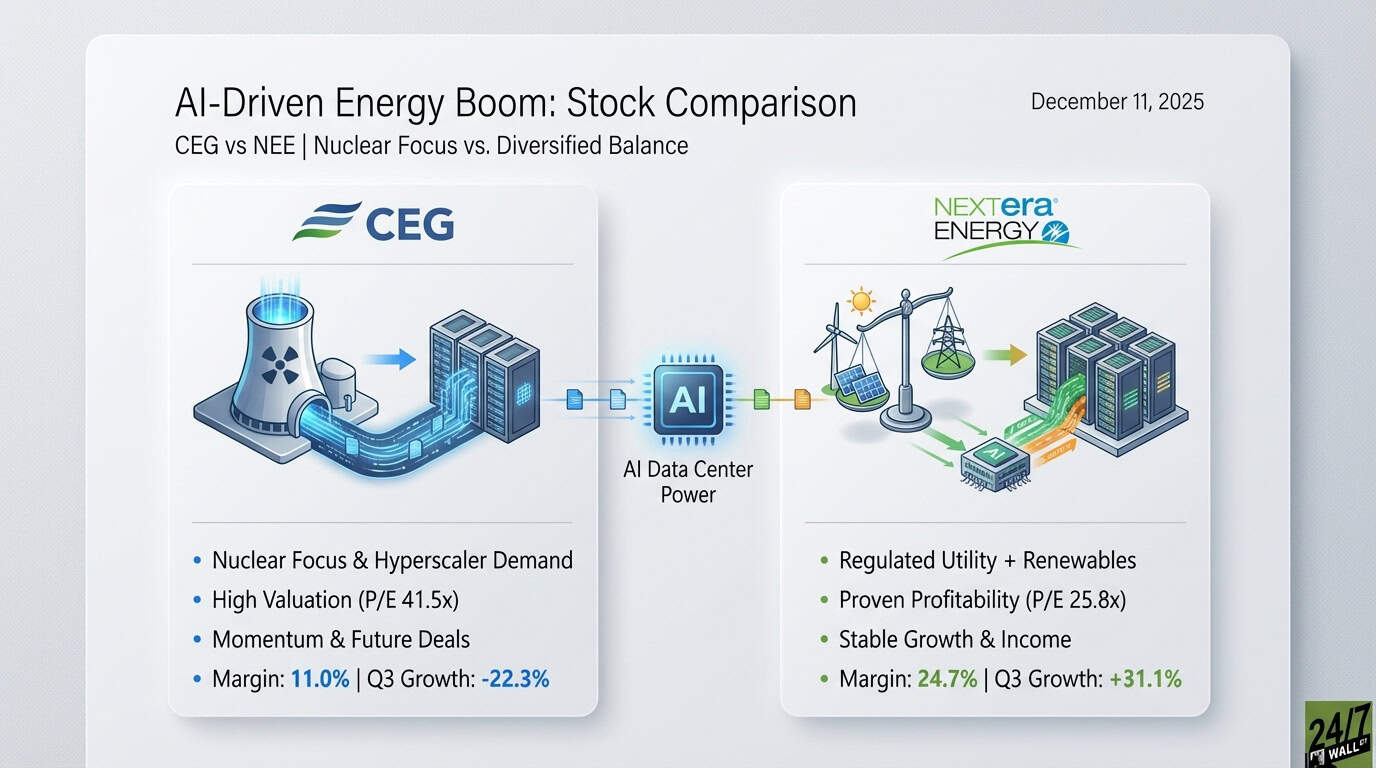

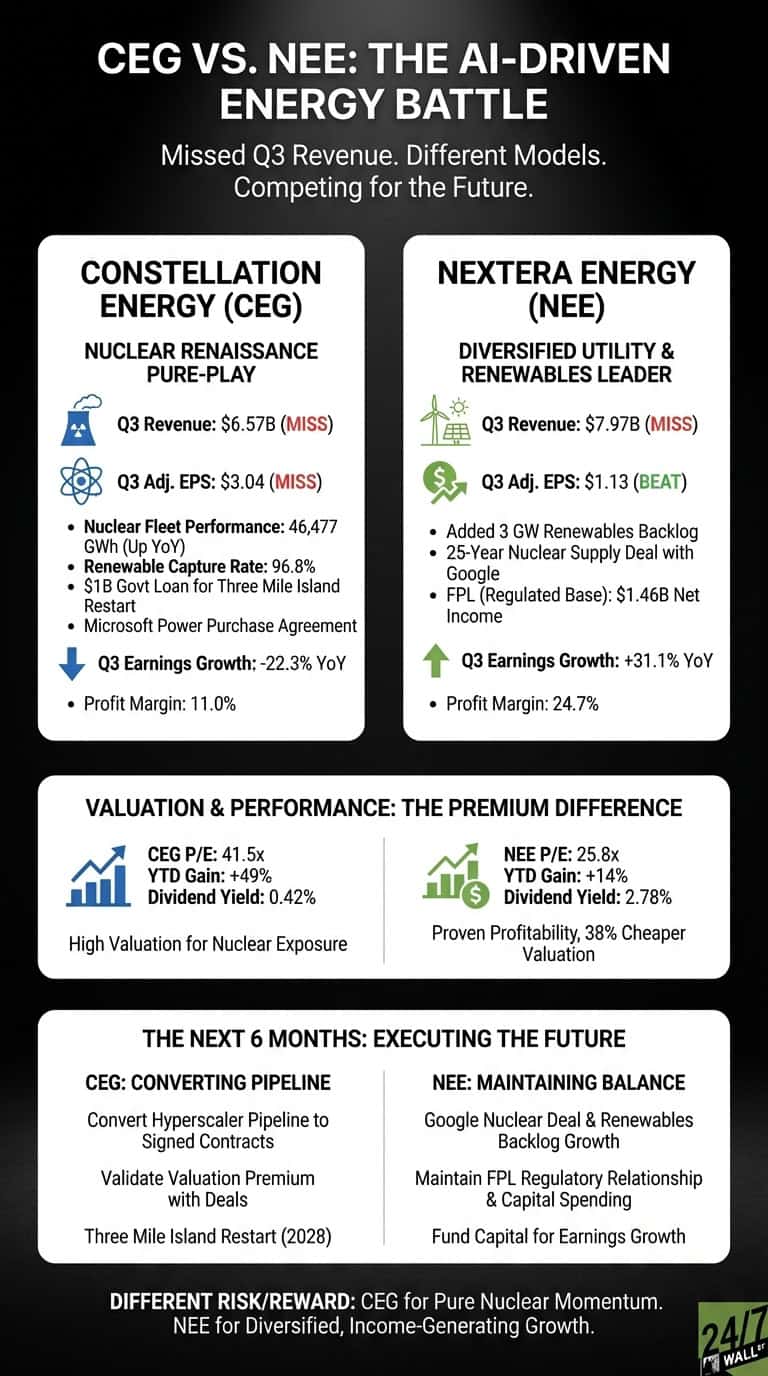

Constellation Energy (Nasdaq: CEG | CEG Price Prediction) and NextEra Energy (NYSE: NEE) both missed Q3 2025 revenue expectations, but the stories reveal fundamentally different business models competing for the AI-driven energy boom.

Nuclear Focus vs. Diversified Balance

Constellation posted $6.57 billion in revenue and $3.04 per share in adjusted earnings, both below Wall Street targets. CEO Joe Dominguez called it “outstanding performance” from the nuclear fleet, which generated 46,477 gigawatt-hours in Q3, up from 45,510 a year earlier. Renewable capture rates improved to 96.8%. The company secured a $1 billion government loan to restart the Three Mile Island reactor, backed by a Microsoft power purchase agreement.

NextEra delivered $7.97 billion in revenue but beat on earnings at $1.13 per share versus the $1.05 estimate. The company added 3 gigawatts to its renewables backlog and announced a 25-year nuclear supply deal with Google to power Iowa data centers. Florida Power & Light contributed $1.46 billion in net income, providing the stable regulated base that funds NextEra Energy Resources’ renewable expansion. Management maintained 2025 earnings guidance of $3.45 to $3.70 per share and projected roughly 10% annual dividend growth through 2026.

| Business Driver | CEG | NEE |

| Core Growth Engine | Nuclear fleet performance | FPL regulated base + renewables |

| Q3 Earnings Growth | -22.3% YoY | +31.1% YoY |

| Profit Margin | 11.0% | 24.7% |

| Dividend Yield | 0.42% | 2.78% |

Premium Valuation Meets Proven Profitability

Constellation trades at 41.5x trailing earnings compared to NextEra’s 25.8x multiple, a 61% premium reflecting investor enthusiasm for nuclear exposure to hyperscaler demand. The stock climbed 49% year-to-date through early December versus NextEra’s 14% gain. That rally occurred despite a 22% earnings decline in Q3, while NextEra grew earnings 31%.

NextEra operates with nearly double Constellation’s profit margin at 24.7% and generates more predictable cash flow through its regulated Florida utility. The company serves 12 million customers with steady rate base growth, then deploys that capital into renewable projects with long-term contracts. Constellation concentrates risk and reward in merchant nuclear generation, where output depends on fleet reliability and power prices.

What the Next Six Months Will Reveal

Watch whether Constellation can convert its hyperscaler pipeline into signed contracts at economics that justify the valuation premium. Dominguez said the team “has never been more active with serious and knowledgeable customers,” but deals take time. The Three Mile Island restart won’t deliver power until 2028.

For NextEra, the Google nuclear deal and continued renewables backlog growth matter more than quarterly revenue misses. Track whether FPL can maintain its regulatory relationship in Florida while funding the capital spending that drives earnings growth.

Different Risk/Reward Profiles

Constellation offers pure exposure to the nuclear renaissance at a 41x multiple. The stock has momentum and a clear thesis.

NextEra provides a combination of regulated utility stability and renewable growth at a 38% cheaper valuation. The 2.78% dividend yield provides income while the Google deal and renewables backlog develop. NextEra’s 24.7% profit margins and 31% recent earnings growth demonstrate different execution characteristics. The company can participate in nuclear opportunities without depending entirely on that narrative. For investors seeking energy transition exposure across multiple technologies and customer segments, NextEra offers a more diversified approach.

Contact [email protected] for any questions or corrections.