The AI revolution has a power problem. Training GPT-4 required as much electricity as 10,000 U.S. homes use in a year. Multiply that by thousands of models being trained simultaneously, plus billions of daily queries. The result? A data center energy boom reshaping power generation. Facilities drawing 100+ megawatts each, with some hyperscale campuses approaching 1 gigawatt (the equivalent of small cities).

The winners won’t just be chip makers and cloud providers. Companies supplying reliable, scalable power infrastructure are seeing explosive demand. We ranked the top three plays based on revenue scale, profitability metrics, AI data center exposure, and growth trajectories.

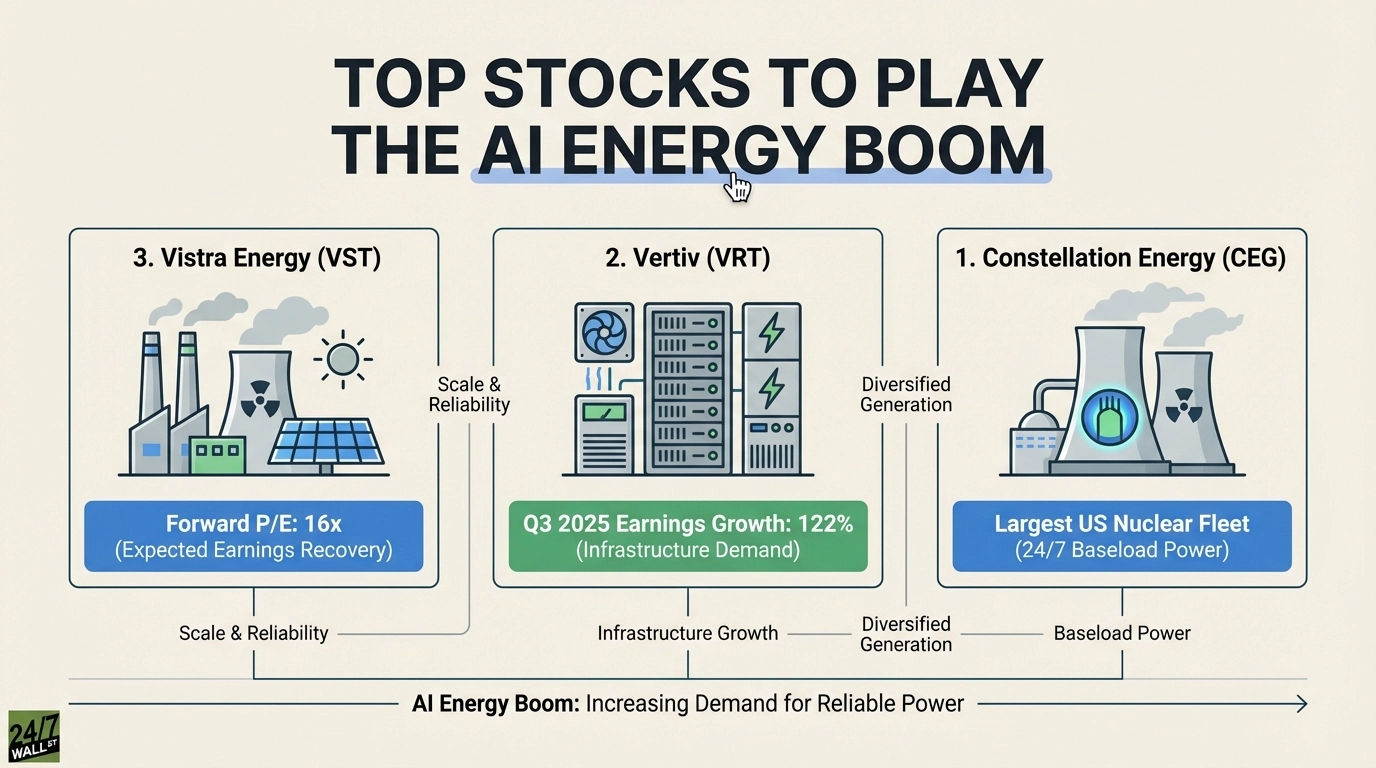

3. Vistra Energy: The Diversified Power Play

Vistra Energy (NYSE:VST | VST Price Prediction) brings $54.2 billion in market cap and a diversified generation portfolio spanning natural gas, nuclear, and renewable assets. Q3 2025 revenue hit $4.97 billion with 21% operating margin, demonstrating efficient operations critical for competing on cost with data centers.

Five-year price performance: up 695% since 2021. But recent volatility shows the stock down 19% over the past six months and down 4% year-to-date, suggesting investors question whether the AI energy thesis can sustain premium valuations.

Vistra’s 58x trailing P/E looks stretched until you see the forward P/E of 16x. Earnings are expected to jump 49% this year, which helps drive that compression. The company generated $5.21 billion in EBITDA over the trailing twelve months with $3.99 billion in operating cash flow.

The challenge? Recent quarterly earnings dropped 66.7% year-over-year, and revenue fell 20.9%. These declines reflect cyclical pressures in power markets, but forward-looking metrics suggest the AI demand wave will reverse these trends. With 92.6% institutional ownership and a consensus price target of $230 (implying 35%+ upside), sophisticated capital is backing the thesis. Execution risk remains highest here given recent earnings headwinds. However, buying Vistra after recent weakness could turn into a long-term opportunity if AI power demand continues in Texas.

2. Vertiv: The Infrastructure Pure Play

Vertiv (NYSE:VRT) supplies cooling systems, power distribution, and monitoring equipment for data centers. When hyperscalers build new AI facilities, Vertiv gets the call.

The numbers validate the positioning. Q3 2025 revenue hit $2.68 billion, up 29% year-over-year. Net income jumped to $398.5 million, representing 122% earnings growth. Operating margins of 20.5% demonstrate pricing power in a supply-constrained market. Return on equity of 38.9% shows exceptional capital efficiency.

Vertiv has beaten analyst estimates in all four quarters of 2025, with an average surprise of 34.7%. Q1 2025 showed the most dramatic beat at 77.8%, indicating accelerating demand momentum analysts underestimated. The stock is up 76% over the past year and 3% year-to-date, showing continued momentum while peers have pulled back.

Valuation is aggressive at 68x trailing earnings, but the forward P/E of 33x reflects expectations for continued growth. With a PEG ratio of 0.9, the growth-adjusted valuation appears reasonable given recent 122% earnings expansion. The five-year return of 809% demonstrates this isn’t a new story, but recent acceleration suggests the AI boom is entering a new phase. Vertiv’s $69.4 billion market cap validates this as a major player, not a speculative bet. If you’re looking for smaller plays in Vertiv’s specialties, consider a stock like Modine Manufacturing (NYSE: MOD). It’s about 1/10th the size of Vertiv, but benefits from many of the same trends.

1. Constellation Energy: The Nuclear Baseload Leader

Constellation Energy (Nasdaq:CEG) operates the largest nuclear fleet in the United States. AI data centers need 24/7 baseload power, not intermittent renewable generation. Nuclear delivers carbon-free electricity at scale with capacity factors above 90%. When Microsoft (NASDAQ:MSFT) and other hyperscalers talk about powering AI with clean energy, nuclear power is their top choice.

Constellation’s $89 billion market cap makes it the largest pure-play nuclear operator globally. Q3 2025 revenue reached $7.18 billion with $930 million in net income. Operating margins of 11% in the past twelve months are lower than Vertiv’s, but the scale is dramatically larger. EBITDA of $5.95 billion over the trailing twelve months and operating cash flow of $2.41 billion provide substantial financial firepower.

The company’s earnings trajectory shows the nuclear renaissance in action. Annual EPS swung from losses in 2022 to $11.90 in 2024, before moderating to $6.02 through the first three quarters of 2025. That 2024 peak represented a 137% increase from 2023, driven by power purchase agreements with data center operators paying premium prices for reliable, clean baseload power.

Recent stock performance has been volatile, up 5% over the past year and down 21.2% year-to-date. But the five-year return of 540% demonstrates the long-term thesis. The company’s 33x P/E is the most reasonable of the three stocks, reflecting both earnings power and market confidence in sustained demand. With no sell-side ratings among analysts, the consensus remains bullish on nuclear’s role in powering AI infrastructure.

The Verdict: Scale and Reliability Win

Constellation takes the top spot because AI data centers can’t tolerate power interruptions. Nuclear provides the baseload reliability that natural gas and renewables can’t match at this scale. Vertiv offers the highest growth rates but faces execution risk as it scales production. Vistra provides diversification and could be a worthwhile alternative if you’re looking for a stock with higher upside than Constellation.

Contact [email protected] for any questions or corrections.