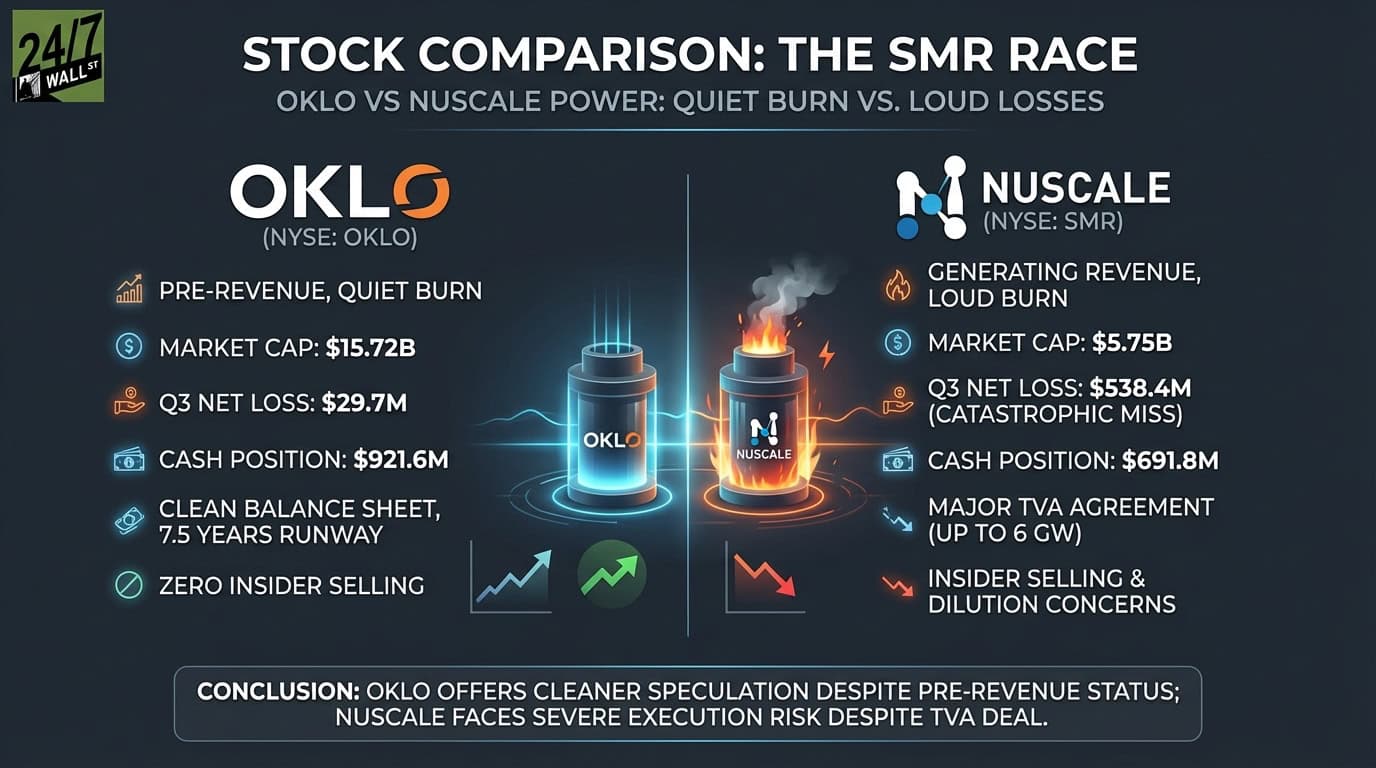

Oklo (NYSE | OKLO Price Prediction: OKLO) and NuScale Power (NYSE: SMR) both operate in the small modular reactor space, but their recent quarterly results reveal two companies at radically different stages. Oklo remains pre-revenue with a $15.72 billion market cap, burning roughly $30 million per quarter. NuScale generates $63.9 million in trailing revenue but shocked investors with a catastrophic Q3 earnings miss.

One Burns Cash in Silence. The Other Burns It Loudly.

Oklo posted a Q3 net loss of $29.7 million, maintaining its pre-revenue development posture. The company holds $921.6 million in cash and short-term investments against just $40.6 million in liabilities, providing approximately 7.5 years of runway at current burn rates. R&D consumed $14.9 million in the quarter, with SG&A adding another $21.4 million. Management has offered no concrete revenue timeline.

NuScale took a different path. On November 6, 2025, the company reported Q3 results that missed estimates by 1,323%. The reported loss of $1.85 per share compared to analyst expectations of negative $0.13. Revenue of $8.24 million came in below the $11.17 million estimate. The massive loss stemmed from a $495 million milestone contribution to ENTRA1 under a partnership agreement. Operating losses hit $538.4 million versus $41 million in the prior year.

NuScale did announce a major win: a TVA agreement for up to 6 gigawatts of SMR capacity, which CEO John Hopkins called “the largest SMR deployment program in U.S. history.” The company also raised $475.2 million through an at-the-market offering, issuing 13.2 million shares. But the combination of dilution, earnings disaster, and one-time charges left investors questioning execution.

| Metric | OKLO | SMR |

| Market Cap | $15.72B | $5.75B |

| Revenue TTM | $0 | $63.9M |

| Q3 Net Loss | $29.7M | $538.4M |

| Cash Position | $921.6M | $691.8M |

Momentum and Insider Signals Tell Different Stories

Technical momentum favors Oklo. The stock’s RSI sits at 49.31, neutral territory after recovering from oversold conditions in late November when RSI bottomed at 35.46. NuScale’s RSI remains weaker at 41.78, struggling to break above 42 despite attempts to recover from a November low of 27.13.

Insider activity raises concerns at NuScale. CFO Robert Hamady exercised 40,000 options at $3.20 and sold all 40,000 shares at $22.17 on December 8, three days after the earnings disaster. Major shareholder Fluor Corp systematically reduced its position in early October, selling 4.7 million shares between $35.86 and $43.62 before the earnings miss became public. Oklo reported zero insider transactions over the past three months.

Why I Lean Toward Oklo Despite the Speculation

If you can stomach extreme volatility, Oklo looks better positioned. The 52-week range of $17.14 to $193.84 reflects pure speculation, but the company avoids the credibility damage NuScale just suffered. Wall Street assigns Oklo a $113.29 price target with 10 buy or strong buy ratings versus seven holds. NuScale’s $36.88 target comes with only six buy ratings and three sell or strong sell ratings.

I would wait for Oklo to demonstrate a path to revenue before committing serious capital, but the cleaner balance sheet and absence of catastrophic earnings misses make it the safer speculation between the two. NuScale’s TVA deal matters, but insider selling and the pattern of missing estimates by vast amounts suggest execution risk remains severe.

Contact [email protected] for any questions or corrections.