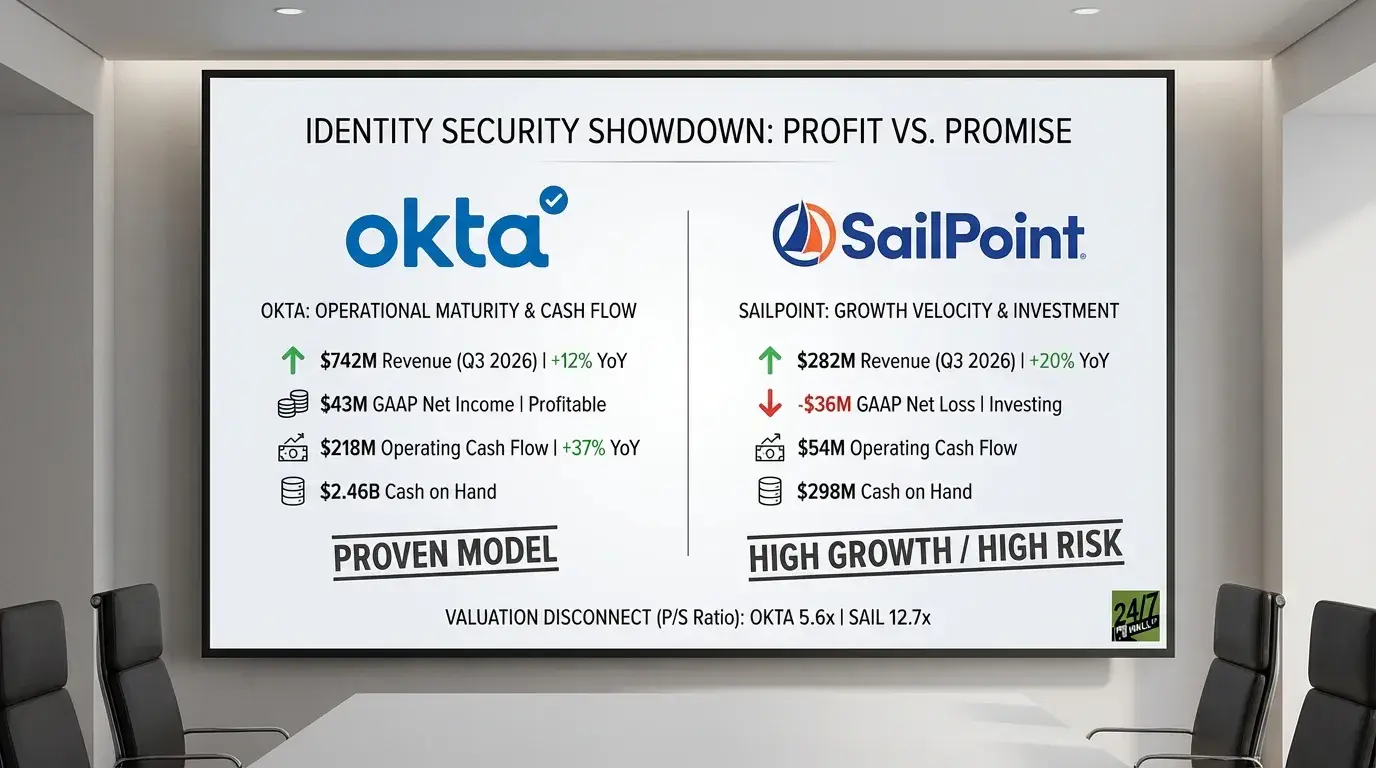

Okta (NASDAQ: OKTA | OKTA Price Prediction) and SailPoint Technologies (NYSE: SAIL) both beat Q3 2026 earnings expectations, but their financial trajectories diverge sharply. Okta delivered $742 million in revenue with $43 million in GAAP net income. SailPoint posted $282 million in revenue while losing $36 million.

Profitability vs. Growth Velocity

Okta’s quarter showed operational maturity. Revenue climbed 12% year over year, but operating cash flow surged 37% to $218 million. Free cash flow reached $211 million. The company turned a $16 million loss into $23 million in operating income. CEO Todd McKinnon highlighted “continued strength with large customers” and adoption of Okta Identity Governance and Auth0 for AI Agents. Large enterprise deals carry higher margins and stickier retention.

SailPoint grew faster at 20% revenue growth and 38% SaaS ARR expansion. The company crossed $1 billion in total ARR, a milestone CEO Mark McClain called proof of “the strength of SailPoint’s strategy and the durability of our business.” But SailPoint’s GAAP operating loss widened to $42 million from $24 million a year earlier. The company reports a 20% adjusted operating margin, but that requires adding back $98 million in stock compensation and other expenses. Okta doesn’t need those adjustments to show profit.

| Metric | Okta | SailPoint |

| Revenue Growth | 12% | 20% |

| GAAP Net Income | $43M | -$36M |

| Operating Cash Flow | $218M | $54M |

| Cash on Hand | $2.46B | $298M |

Scale and Cash Generation Diverge Sharply

Okta operates at nearly three times SailPoint’s revenue scale and generates four times the operating cash flow. That gap matters when both companies need to fund AI product development and compete for the same enterprise identity security budgets. Okta’s $2.46 billion cash position provides room to invest aggressively or weather margin pressure. SailPoint’s $298 million in cash leaves less margin for error, especially with a price-to-sales ratio of 12.7x compared to Okta’s 5.6x.

The valuation disconnect reflects market expectations. SailPoint trades at 119x forward earnings despite current losses, while Okta sits at 24x forward earnings with actual profit. Analysts favor SailPoint slightly more, with 86% buy ratings versus Okta’s 64%. The market believes SailPoint’s growth rate justifies the premium, but only if the company can convert revenue into cash flow without destroying margins further.

What Determines the Winner From Here

Okta’s next test is whether large customer wins can offset slower overall growth. The company guided Q4 revenue to $748-750 million, implying roughly 11% growth. If Identity Governance and AI-focused products gain traction, Okta could reaccelerate without sacrificing profitability. SailPoint needs to prove it can scale SaaS ARR past $1 billion while narrowing losses. The company’s Q4 guidance calls for $290-294 million in revenue and $58.5-59.5 million in adjusted operating income, but GAAP profitability remains elusive.

Why I Favor Okta’s Proven Model Over SailPoint’s Promise

I lean toward Okta because cash flow and profitability matter more than growth rate when both companies face the same competitive pressures. Okta’s 156% earnings growth over the past year shows operating leverage kicking in. SailPoint’s faster revenue growth is real, but the company is burning through capital to achieve it. Okta offers lower execution risk today. SailPoint might deliver higher returns if it hits profitability ahead of schedule, but that remains a forecast rather than a fact. I’d rather own the company generating $211 million in free cash flow than the one still losing money on a GAAP basis.

Contact [email protected] for any questions or corrections.