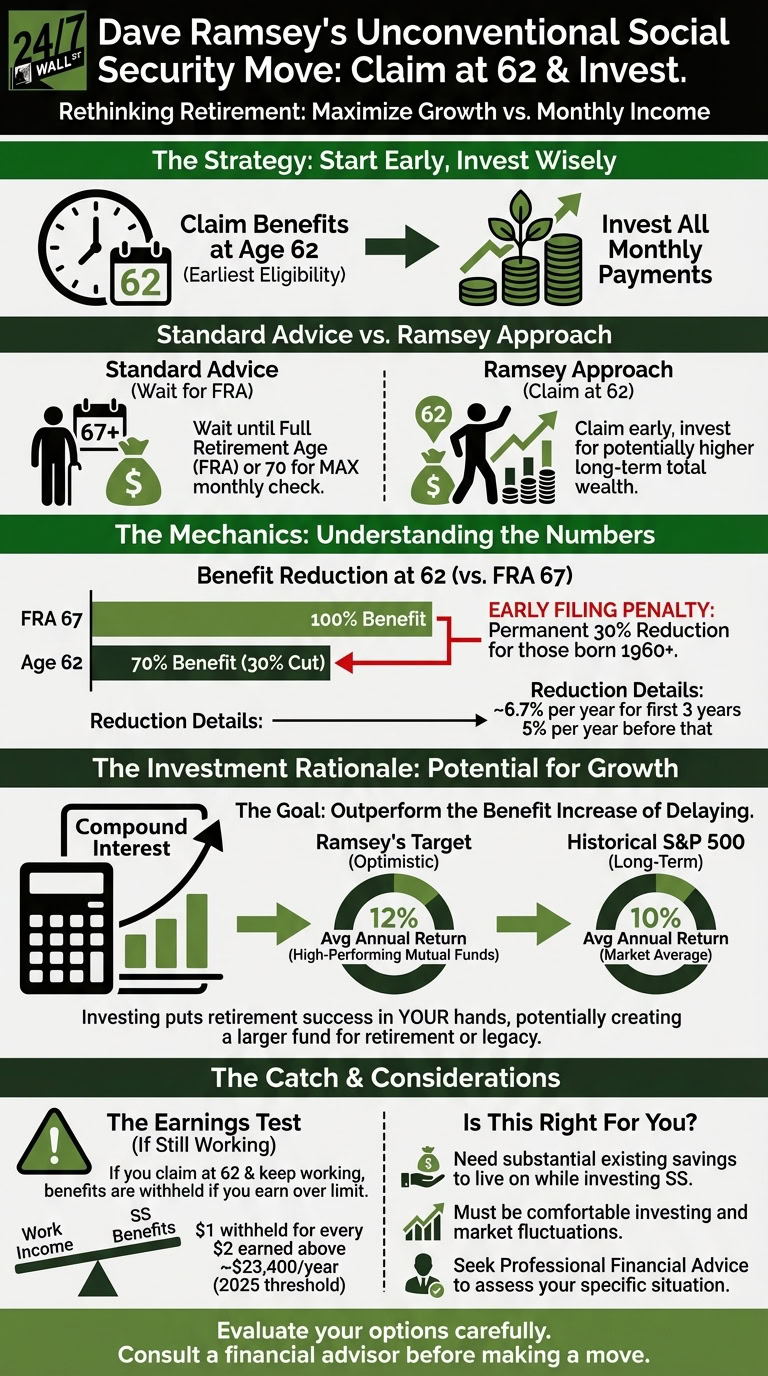

Dave Ramsey wants Baby Boomers to make an unconventional move when it comes to Social Security. His advice: claim benefits at 62 and invest every check. That is a sharp departure from conventional wisdom, which tells retirees to delay claiming as long as possible to lock in the largest monthly payment. Ramsey’s position cuts against that guidance and invites real debate.

The strategy carries genuine risks, but it also has real merit for retirees who have the financial cushion to pull it off. The key question is whether you are confident you can invest the money productively rather than spend it on living expenses.

Why Ramsey recommends starting Social Security at 62

Ramsey recommends claiming Social Security at the earliest eligible age, even though it sits well before a worker’s full retirement age (FRA) and triggers a permanent reduction in monthly benefits. Anyone born in 1960 or later has an FRA of 67, so filing at 62 means claiming five years early and accepting a 30% cut to the monthly check.

Ramsey’s counter to that reduction is straightforward: put every dollar into a high-performing mutual fund. His view is that a well-invested portfolio can grow faster than the additional income gained by waiting. He has also made a longevity argument on his show and blog, saying that “your retirement payments die when you die, so you might as well take the money and make the most of it while you can.” If a retiree passes away earlier than average, collecting for five extra years can mean more total lifetime income even at the reduced rate.

There is also a program-solvency dimension that has grown more urgent. The 2026 Social Security Trustees Report, released June 9, 2026, projects the OASI Trust Fund will be depleted in the fourth quarter of 2032, one quarter earlier than last year’s report projected. If Congress does not act before then, the program would be able to pay only about 78% of scheduled benefits from ongoing payroll tax revenue. For retirees who place any weight on that risk, locking in payments now and investing them has an added appeal.

The math behind Ramsey’s argument

Ramsey’s case has genuine mathematical support. Filing early shrinks monthly benefits by 5/9 of 1% for each of the first 36 months before FRA, and by 5/12 of 1% for each additional month beyond that. Practically, that works out to roughly a 6.7% reduction per year for the first three years and about 5% per year for years four and five, producing that combined 30% hit for a claim at 62.

The flip side is that an early filer collects checks for five years before a delayed claimer receives a single dollar. On a standard $2,000 monthly benefit at FRA, claiming at 62 yields roughly $1,400 a month, while waiting until 70 (which earns an 8% annual credit above FRA) pushes the monthly check to around $2,480. That gap of more than $13,000 per year is the prize for waiting, but only if the retiree lives long enough to recoup the years of missed payments. The break-even point typically falls between ages 80 and 82.

Ramsey argues that investing the early checks can close or exceed that gap. He cites expected returns of 10% to 12% annually from diversified mutual funds. The 12% figure is optimistic for a retiree who needs a relatively conservative allocation, but a 10% average annual return is historically defensible for a long-term equity investor given the S&P 500’s track record. The core logic is that compounding over a 15-plus-year horizon can turn those smaller early checks into a larger pool of capital than a delayed, guaranteed benefit would have provided.

Taking ownership of those funds also shifts control of your retirement outcome away from a government program and toward assets you manage directly. For retirees who worry about benefit cuts or means-testing down the road, that autonomy has real value.

The important catches to understand

Ramsey’s strategy works only if every Social Security check goes into investments rather than toward monthly bills. Retirees who claim at 62 and need that money for groceries and rent are simply locking in a smaller lifetime benefit. To execute the plan as intended, you need to be fully retired and have enough in savings to cover living expenses independently. That is a higher bar than many 62-year-olds can clear: Fidelity data shows the average 401(k) balance for workers aged 60 to 64 is about $246,500, and median balances run considerably lower.

A second obstacle applies to anyone still working. The Social Security earnings test withholds $1 in benefits for every $2 earned above the annual limit, which stands at $24,480 in 2026 (up from $23,400 in 2025). That translates to a monthly threshold of $2,040. Benefits withheld under this rule are not lost permanently. Social Security recalculates your payment upward at FRA to credit those months. In the meantime, though, the checks you planned to invest may not arrive, which breaks the strategy’s logic.

There is also a tax dimension worth noting. If your provisional income exceeds $34,000 as a single filer (or $44,000 for a married couple filing jointly), up to 85% of your Social Security benefits become subject to federal income tax. Routing investment income on top of early benefits can push you past those thresholds and effectively shrink your real return.

For those who can genuinely invest the funds and live on other savings in the meantime, Ramsey’s approach deserves serious consideration. A financial advisor can help you model the numbers for your specific situation, including the impact on survivor benefits for a spouse, before you file.

Editor’s note: This article has been updated to reflect the 2026 Social Security earnings test threshold of $24,480 (up from $23,400 in 2025) per official SSA data, the 2026 Trustees Report projection that the OASI Trust Fund will be depleted in Q4 2032 with 78% of benefits payable at that time, and additional context on the roughly $13,000 annual income gap between claiming at 62 versus 70, the average 401(k) balance of about $246,500 for workers aged 60 to 64, and the provisional income thresholds above which Social Security benefits become taxable.

Contact [email protected] for any questions or corrections.