NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) has delivered a 23,000% return over the past decade has become the benchmark every tech investor measures against. The company created the infrastructure that made modern AI possible. Now the question: which company pulls off the next NVIDIA-like run?

We analyzed 15 AI-adjacent stocks across semiconductors, software, and quantum computing to find the five with the clearest path to impressive future returns thanks to massive growth in the decade ahead. Here’s what separated the contenders from the pretenders.

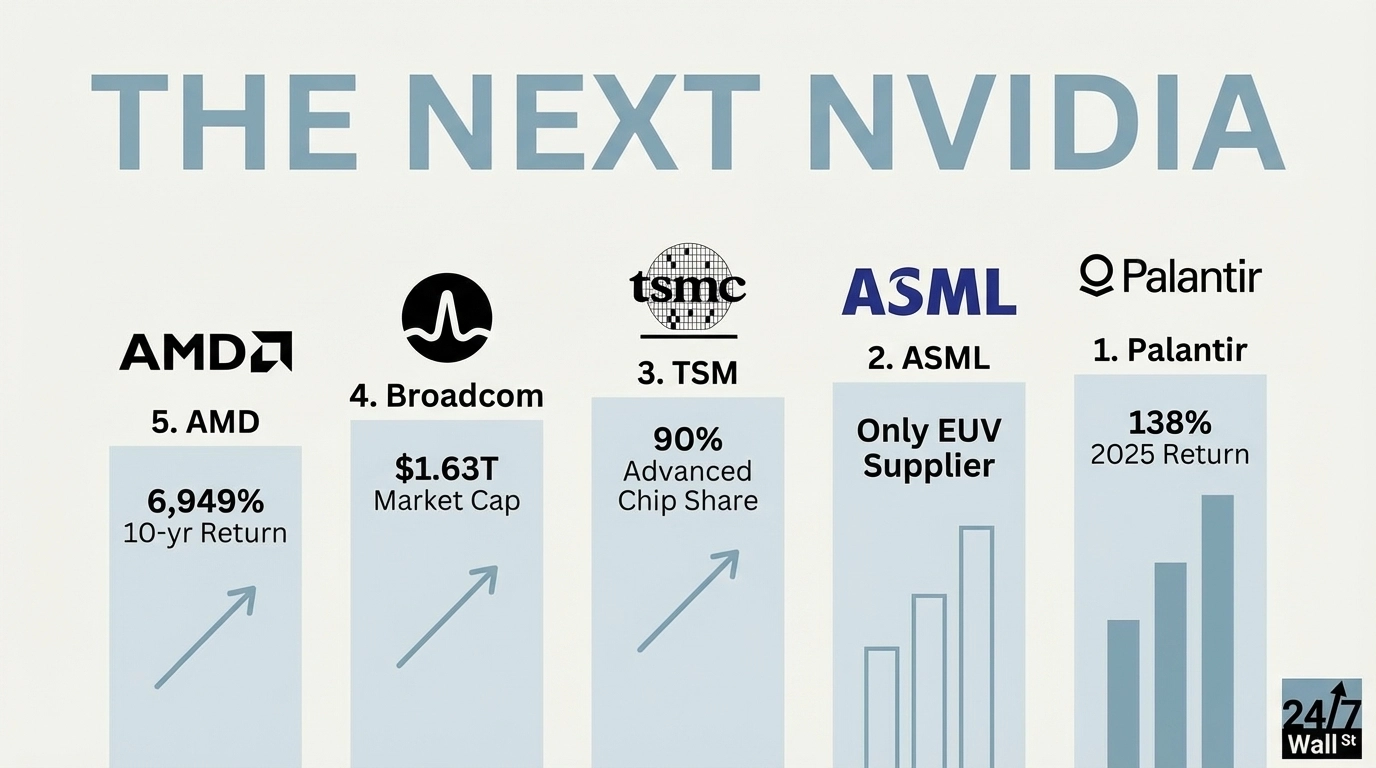

5. Advanced Micro Devices: The Direct Challenger With Proven Chops

Advanced Micro Devices (NASDAQ:AMD) delivered a 6,949% return over the past decade. MI300 AI accelerators have gained traction against NVIDIA’s H100 chips, particularly among hyperscalers diversifying their AI infrastructure. The next battle will pit AMD’s MI400 series against NVIDIA’s Blackwell series.

AMD generated $32.0 billion in trailing revenue with 36% year-over-year growth. The company’s 100x P/E prices in continued market share gains, but AMD needs to prove it can sustain momentum beyond initial MI300 wins. Operating margins of 14% lag far behind NVIDIA’s efficiency, and gross margins of 52% leave limited room for price competition.

The thesis hinges on whether AMD can capture 20% of the AI accelerator market by 2027. If it does, current valuations look reasonable. If NVIDIA maintains its 80% share with Broadcom in second place, AMD becomes an expensive also-ran.

4. Broadcom: The Established Giant Still Growing Fast

Broadcom (NASDAQ:AVGO) already achieved what most “next NVIDIA” candidates aspire to: a $1.63 trillion market cap built on actual profits. The company generated $63.9 billion in trailing revenue with a 36% profit margin.

What makes Broadcom compelling is its custom AI chip business. While NVIDIA sells standardized accelerators, Broadcom designs bespoke silicon for Alphabet (NASDAQ:GOOGL), Meta Platforms (NASDAQ:META), and other hyperscalers who want optimized solutions for specific workloads. This creates stickier customer relationships and higher switching costs.

Earnings nearly tripled year-over-year despite its massive scale. With 46 Buy ratings and zero Sell ratings from analysts, Wall Street sees continued execution. The 73x P/E is expensive, but the company’s 0.97 PEG ratio suggests the valuation matches the growth trajectory. Broadcom won’t deliver 200x returns from here, but it might pull off 3x to 5x over five years with far less risk.

3. Taiwan Semiconductor: The Foundry Monopoly Powering Everything

Taiwan Semiconductor Manufacturing (NYSE:TSM) manufactures roughly 90% of the world’s most advanced chips. Every NVIDIA H100, every Apple (NASDAQ:AAPL) M-series processor, every AMD MI300 gets made in TSM’s fabs. The company generated $119 billion in trailing revenue with 30% year-over-year growth and a 51% operating margin.

TSM’s 1,711% return over the past decade proves the picks-and-shovels approach works. The company doesn’t need to pick winners in the AI chip wars because it manufactures for all of them. Recent momentum tells the story: shares are up 55% across the past year.

Geographic risk around Taiwan creates periodic buying opportunities when tensions flare. But TSM’s monopoly position in advanced node manufacturing makes it nearly irreplaceable. The 33x P/E is reasonable for a company this critical to the AI supply chain. Wall Street expects profits to grow another 50% by the end of next year.

2. ASML: The Ultimate Semiconductor Kingmaker

ASML Holding (NASDAQ:ASML) holds the most unassailable moat in semiconductors: it’s the only company on Earth that can manufacture extreme ultraviolet lithography machines. Every advanced AI chip requires ASML’s technology. No ASML machines, no cutting-edge semiconductors.

The company delivered a 1,386% return over the past decade and just posted 19% gains since the beginning of the year. That recent momentum suggests accelerating AI chip demand across the industry. ASML generated $37.5 billion in trailing revenue with a 33% operating margin and 45x P/E.

What makes ASML special is its position one layer deeper than TSM. While foundries compete on price and capacity, ASML has zero competition in EUV lithography. The company’s machines cost $200 million each, and customers wait years for delivery. This creates a revenue stream that’s both predictable and nearly impossible to disrupt.

1. Palantir: The Software Play With NVIDIA-Like Momentum

Palantir Technologies (NYSE:PLTR) delivered a 138% return in 2025, outpacing NVIDIA’s 37% gain over the same period. The company reached a $414.8 billion market cap by proving that AI software monetization can scale as fast as hardware.

Palantir generated $3.9 billion in trailing revenue with 63% year-over-year growth and a 33% operating margin. The Artificial Intelligence Platform is winning enterprise contracts at an accelerating pace, particularly in government and defense where switching costs are enormous.

Yes, the 395x P/E is absurd. Yes, the 106x price-to-sales multiple prices in perfection. But NVIDIA traded at extremes during its growth phase as well. Palantir’s quarterly earnings more than doubled year-over-year, demonstrating the kind of acceleration that justifies premium valuations. With 80% gross margins, the company has room to maintain profitability while scaling.

The risk is obvious: any stumble gets punished severely at these multiples. But if you’re hunting for the stocks that could become massive winners across the next decade if AI becomes the largest technology trend of all time, you need to accept that the winners trade at valuations that make traditional investors uncomfortable. Palantir’s combination of accelerating growth, expanding margins, and defensible moat in AI software makes it the most compelling “next NVIDIA” candidate.

The Verdict on Chasing Lightning Twice

Finding the next NVIDIA requires accepting uncomfortable truths about valuation and risk. The companies trading at reasonable multiples probably won’t deliver explosive returns. The ones with massive potential trade at prices that assume flawless execution for years.

Palantir tops this list because it has the clearest path to matching NVIDIA’s growth trajectory. The company is capturing enterprise AI spending at scale, expanding margins while growing revenue, and building sticky customer relationships that create decade-long moats. ASML and TSM offer lower-risk exposure to the entire AI ecosystem. Broadcom provides established profitability with continued growth. AMD gives you a direct play on taking share from NVIDIA.

Contact [email protected] for any questions or corrections.