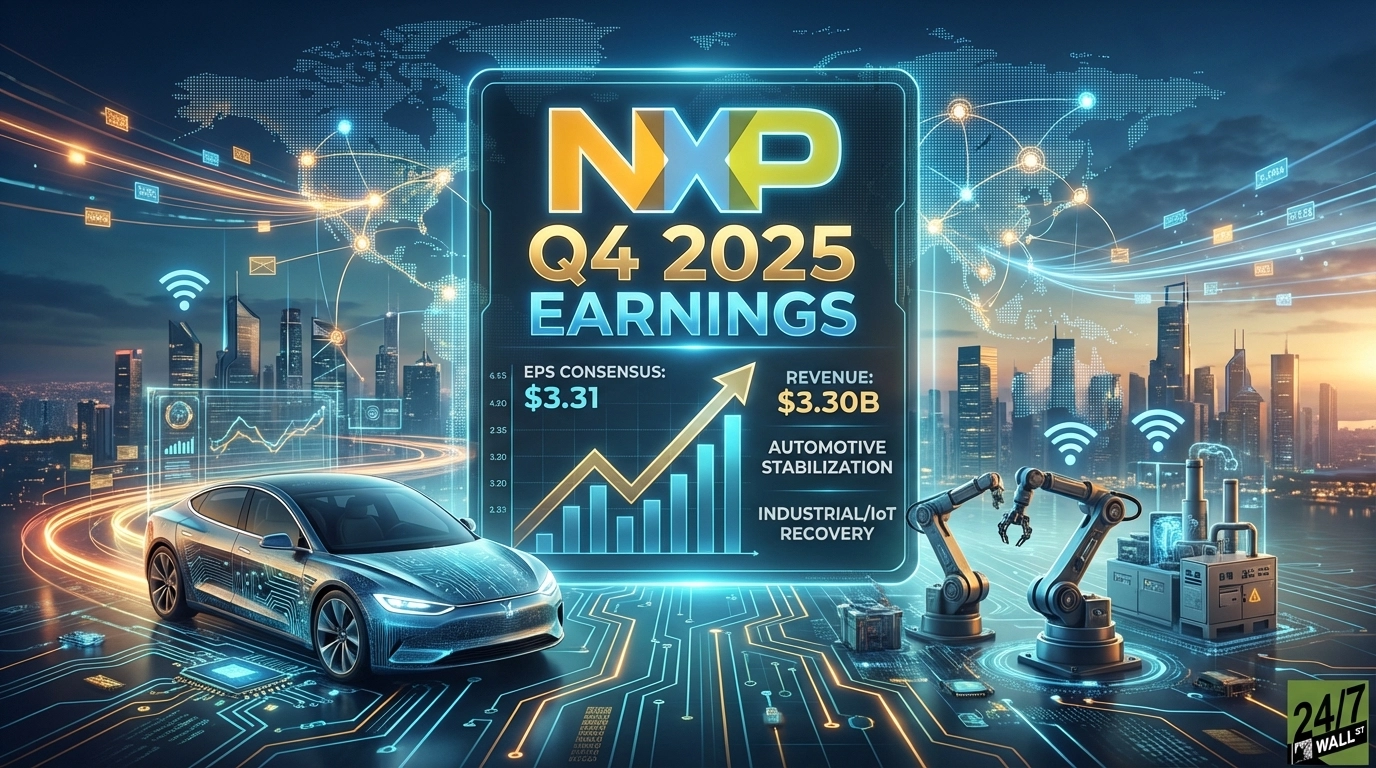

NXP Semiconductors (NASDAQ: NXPI) | NXPI Price Prediction reports Q4 2025 earnings today after market close at 4:10 PM ET. Wall Street expects earnings of $3.31 per share on revenue of $3.30 billion, representing 4.1% year-over-year EPS growth and 6.1% revenue growth. Shares have gained more than 25% since their six-month low on Nov. 20, 2025.

The Numbers That Matter

Wall Street Expects:

- EPS consensus: $3.31

- Revenue consensus: $3.30 billion

- Automotive segment: Continued stabilization after 6% sequential growth in Q3

- Industrial/IoT segment: Recovery expected after 6% sequential improvement in Q3

The Beat Threshold:

A meaningful beat requires EPS of at least $3.36 (1.5% above consensus) paired with revenue of $3.35 billion or higher. The company’s average surprise over the past eight quarters is 1.2%.

Historical Context:

NXP has beaten or met earnings estimates in 10 of the past 11 quarters, with only Q3 2025 showing a minor miss of $0.01. The stock’s average post-earnings move is approximately 5%, though shares jumped 8.4% following Q4 2024’s $0.04 beat.

What Happened Last Quarter

3 Key Takeaways from Q3 2025:

- Revenue of $3.17 billion declined 2.4% year-over-year but improved 8.5% sequentially, signaling potential stabilization

- Operating margin compressed to 28.1% from 30.5% in Q3 2024, though gross margin held steady at 56.3%

- Automotive segment grew to $1.84 billion while Industrial/IoT reached $579 million, both up 6% quarter-over-quarter

Management’s Promise:

Last quarter, management guided Q4 revenue to $3.20-3.40 billion, implying potential sequential growth. The company highlighted completion of its MEMS sensors business sale for up to $950 million and the $243 million acquisition of Aviva Links to strengthen automotive connectivity capabilities.

The Sector Setup

How Peers Have Performed:

Semiconductor earnings this season present a mixed picture. STMicroelectronics missed Q4 estimates by 16 cents and warned of restructuring costs, while Microchip Technology enters its Feb. 5 report with positive analyst sentiment. The sector shows continued pressure in communications infrastructure offset by automotive and industrial strength.

NXP’s positioning differs from broader semiconductor peers given its automotive exposure, which represents approximately 58% of revenue based on Q3 results. With the global discrete semiconductors market projected to reach $77 billion by 2030 from $43.84 billion in 2025, NXP’s automotive and industrial focus could provide insulation from consumer weakness.

What Could Move the Stock

Bull Case Triggers:

- EPS above $3.36 with Q1 2026 guidance indicating continued sequential revenue growth

- Automotive segment revenue exceeding $1.90 billion would signal accelerating content gains in electric vehicles

- Management commentary on design win momentum for the new S32N7 processor, which reduces vehicle integration costs by up to 20%

Bear Case Triggers:

- Revenue miss below $3.25 billion, particularly weakness in automotive segment

- Operating margin compression beyond 200 basis points year-over-year

- Cautious Q1 2026 guidance suggesting extended inventory corrections

The Wild Cards:

Recent insider selling totaling over $5 million in the past 90 days contrasts with institutional buying from National Pension Service and NY State Common Retirement Fund. The company’s $154 million in share buybacks ($54 million in Q3, $100 million after quarter-end) provides some support, but net interest expense of approximately $100 million per quarter remains a headwind.

What Analysts Are Watching

In the past 30 days, analyst activity has remained stable with 28 of 33 analysts maintaining buy-equivalent ratings. The average price target of $264.82 implies 15% upside from current levels around $230.

The 1 Metric That Matters:

Analysts are focused on automotive revenue growth this quarter. With automotive representing nearly 60% of total revenue, any sign of weakening demand or inventory destocking would significantly impact full-year 2026 expectations. A result above $1.90 billion would demonstrate NXP’s ability to gain share in software-defined vehicle architectures, while a decline below $1.80 billion would raise concerns about the automotive semiconductor cycle.

Looking Ahead

NXP has navigated recent headwinds with operating margins near 28% and maintained R&D spending at 18.6% of revenue, but year-over-year revenue declined 5% in fiscal 2024. This report will test whether the sequential improvement seen in Q3 marks an inflection point or temporary stabilization. With shares trading at 17x forward earnings, below the 29x trailing multiple, investors are pricing in earnings recovery. The key question: Can management demonstrate that automotive and industrial end-markets have truly bottomed?

Contact [email protected] for any questions or corrections.