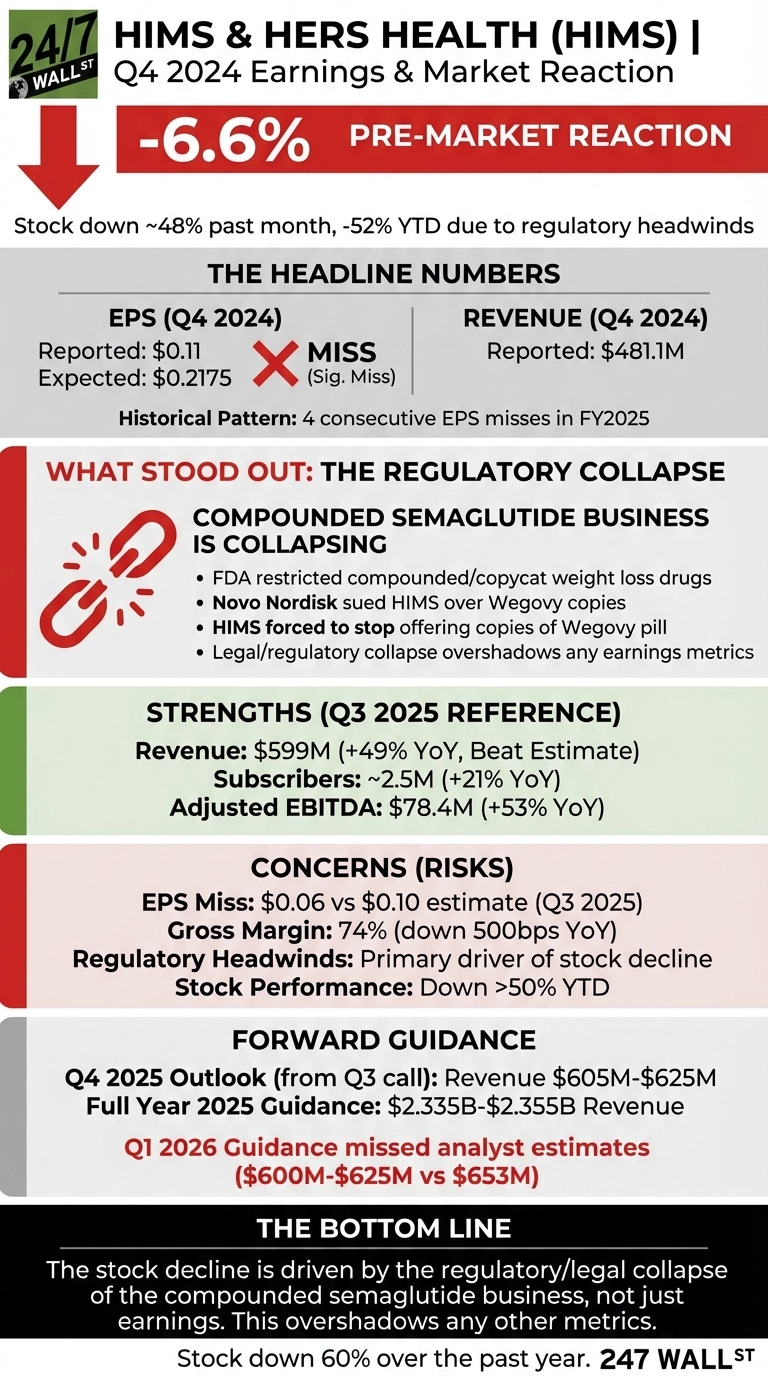

Shares of Hims & Hers Health (NYSE:HIMS) are trading lower this morning after yesterday’s earnings, and the reason is straightforward: guidance. Yesterday we were watching whether management could offer a credible forward path after months of regulatory damage. The answer disappointed.

Guidance Gap Overshadows the Beat

Shares fell in after-hours trading Monday and were down approximately 6.6% in pre-market trading, sitting near $14.18 ahead of the open. The earnings print itself was not the problem. Q4 revenue came in at $617.8 million, up 28% year over year. EPS of $0.08 beat the $0.05 consensus estimate. Full-year 2025 revenue reached $2.35 billion, up 59% year over year, and subscribers exceeded 2.5 million.

The problem was Q1 2026. Management guided first-quarter revenue of $600 million to $625 million, missing analyst estimates of $653 million. The company flagged a $65 million headwind from changes in how personalized weight-loss products are shipped, a direct consequence of the regulatory crackdown on compounded semaglutide that has dominated the HIMS story for weeks. Full-year 2026 guidance of $2.7 billion to $2.9 billion was roughly in line with the $2.74 billion consensus, but the soft Q1 print set a cautious tone at the open.

Regulatory Overhang Remains the Real Story

As we covered in recent weeks, the regulatory collapse of the compounded semaglutide business has been the defining force on this stock. The FDA resolved the semaglutide shortage and moved to restrict copycat compounded versions, Novo Nordisk filed a patent infringement suit after Hims launched and then pulled a $49 compounded Wegovy pill, and a securities fraud investigation was initiated by outside law firms. That sequence sent HIMS down nearly 48% over the past month and more than 52% year to date heading into Monday’s print.

On the earnings call, CEO Andrew Dudum struck a defiant tone, emphasizing that the majority of revenue and profitability is driven by offerings outside of weight loss. Analysts noted that while international expansion would widen the long-term opportunity, the more important component for the stock is how Hims progresses with its weight-loss business.

What to Watch From Here

The Q1 guidance miss confirms what the market has feared: the semaglutide transition is creating a real near-term revenue air pocket, not just a perception problem. Watch whether the Hers brand’s momentum, now accounting for nearly 40% of U.S. revenue, and the Eucalyptus acquisition can provide enough diversification to offset that pressure. Analyst price target revisions after this morning’s open will be the next signal worth tracking.