Last quarter, Microsoft (NASDAQ:MSFT | MSFT Price Prediction) delivered a strong earnings beat, but one number overshadowed everything else: $29.88 billion in capital expenditures (CapEx) for Q2 FY2026, the quarter ended Dec. 31, 2025. That figure, reported in Microsoft’s 8-K filed Jan. 28, 2026, represents a 89% increase year-over-year from $15.80 billion — a near-doubling in a single quarter that has investors questioning the pace and payoff of the company’s AI infrastructure buildout.

To put the scale in context, Microsoft’s last four quarters of CapEx total $83.09 billion, already surpassing the widely cited $80 billion AI infrastructure commitment. This spending represents a structural shift: pre-AI era capex consistently ran at 25-27% of operating cash flow, while the most recent full fiscal year saw that ratio climb to 47.4%. The consequence is visible in free cash flow, which fell 9.3% year-over-year to $5.88 billion even as operating cash flow surged 60% to $35.76 billion. The CapEx machine is consuming the gains.

Spending vs. Results

The broader quarterly results were objectively strong. Revenue reached $81.27 billion, up 17% year-over-year, with Azure growing 39% and Microsoft Cloud crossing $51.5 billion, up 26%. Non-GAAP EPS of $4.14 beat the $3.91 consensus estimate. The commercial remaining performance obligation — a measure of contracted future revenue — surged 110% to $625 billion, signaling that enterprise demand for AI-linked services is real and accelerating.

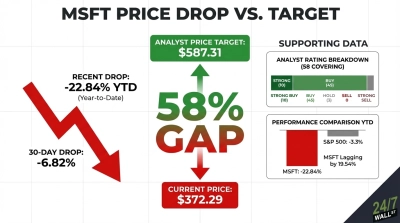

The market’s reaction, however, told a different story. Shares closed at $452.04 at the time of filing, rose briefly to $463.50 within an hour, then reversed sharply — falling to $430.29 the next day and $393.67 within a week. As of this morning, Microsoft trades at $385.83, representing a 14.6% decline since the filing against a 1.6% decline in SPY over the same period. The stock is also trading well below its 200-day moving average of $486.88.

The investor concern is straightforward: CapEx of this magnitude needs to translate into revenue and margin expansion to justify the spend. CEO Satya Nadella offered confidence, stating “We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises.” But the company’s own filing flagged the core risk: “Significant investments may not achieve expected returns.”

Analyst conviction remains high — 57 of 58 analysts carry a Buy or Strong Buy rating with a consensus target of $596 — but prediction markets assign only a 7% probability of Microsoft closing above $405 by month-end. The next major checkpoint will be Q3 FY2026 earnings, expected in April, where investors will be watching whether Azure growth acceleration and RPO conversion begin to visibly offset the capex drag on free cash flow.

Contact [email protected] for any questions or corrections.