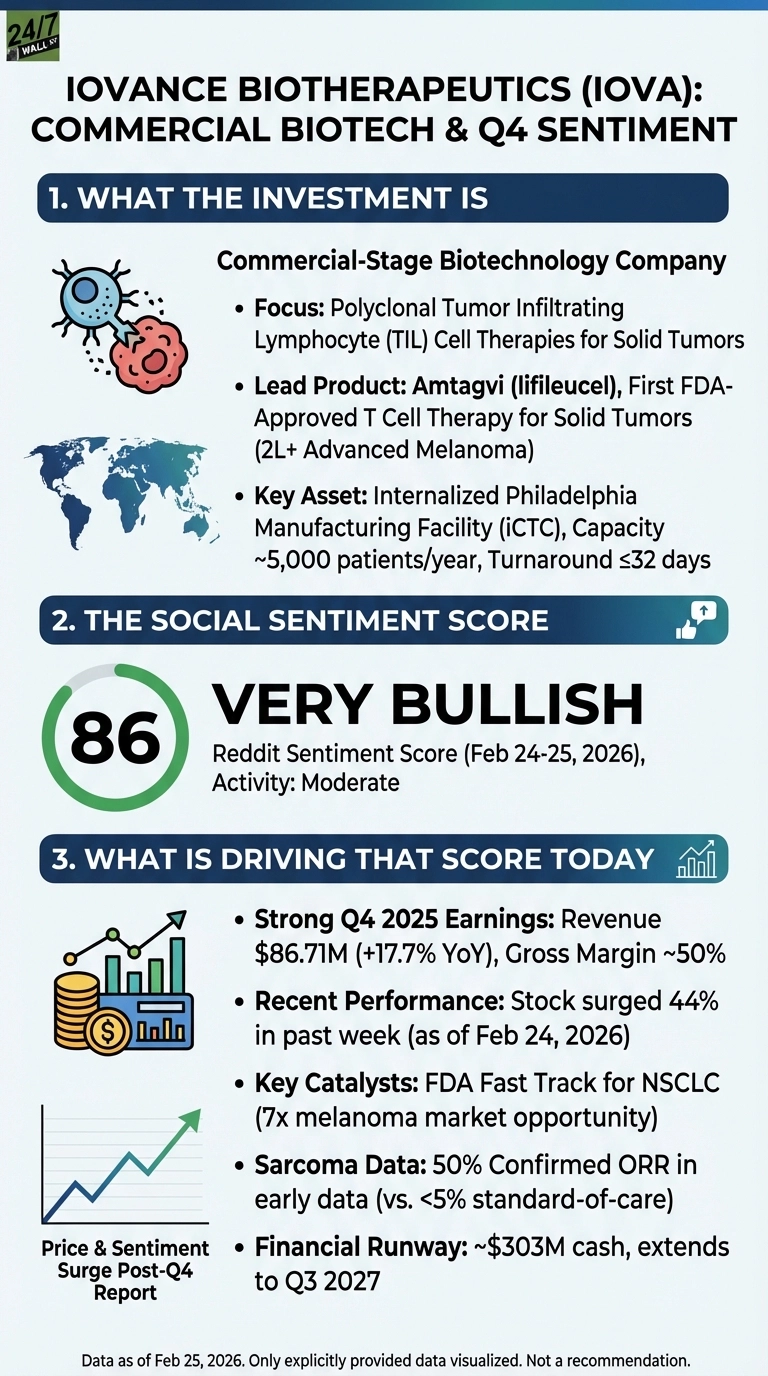

A relative unknown, if you don’t watch the biotherapeutics industry, Iovance Biotherapeutics (NASDAQ:IOVA | IOVA Price Prediction) surged 43% in the past week after reporting Q4 2025 earnings on February 24, pushing Reddit sentiment to 86 out of 100. For a stock that bottomed near $1.64 in May 2025, the turnaround is data-backed. Iovance is no longer a pipeline story. It is a commercial company with a manufacturing moat.

As far as the company’s recent numbers, Q4 revenue hit $86.71 million, up 17.7% year-over-year and roughly 30% sequentially, driven by Amtagvi, the first FDA-approved T-cell therapy for solid tumors. Gross margin reached 50% in Q4, up from 38.2% a year earlier. The per-share loss narrowed to -$0.18 from -$0.26. Full-year 2025 revenue totaled $263.5 million, a 60.6% increase within the company’s guidance range.

The Philadelphia Facility Is the Real Story

The iCTC manufacturing center in Philadelphia is really what is setting Iovance apart from other cell therapy companies that still farm out production. All lifileucel manufacturing runs through that single internalized facility, with capacity for up to 5,000 patients per year and a turnaround time of 32 days or less. COO Igor Bilinsky described it as capable of providing “uninterrupted supply and fully support anticipated global demand today and scale up for the future even during future annual maintenance periods.” That structural cost advantage is already flowing through the margin line.

Reddit Is Paying Attention

IOVA Strong 25Q4 Earnings Call

by u/supp0rtlife in wallstreetbets

One Reddit user expressed conviction in the stock, writing: “They just had a stellar Q4 earnings. CEO said there was potential for a 10-12B market cap ($60). Several catalysts still in the bag due in 26/27. Back to back to back Quarter improvement for their FDA approved product. Not selling a single share until at least $35.” This reflects one user’s personal position and is not a recommendation.

Three catalysts are driving retail interest:

- Amtagvi received FDA Fast Track Designation for non-small cell lung cancer, a market roughly seven times larger than the current melanoma opportunity

- Early sarcoma data showed a 50% confirmed response rate in the first six evaluable patients, against a standard-of-care response rate below 5%

- Cash of approximately $303 million extends the runway into Q3 2027

As of February 25, 2026, Iovance has not yet issued formal 2026 revenue guidance, though CEO Frederick Vogt said the company expects “remarkable revenue growth in 2026” and that guidance will come soon. The analyst consensus 12-month price target sits at $10.00, compared to the current price of $3.06, with 9 of 13 analysts rated Buy or Strong Buy. NSCLC trial enrollment completion and the soft tissue sarcoma Phase 2 launch in Q2 2026 are the near-term catalysts that will determine whether momentum holds.

Contact [email protected] for any questions or corrections.