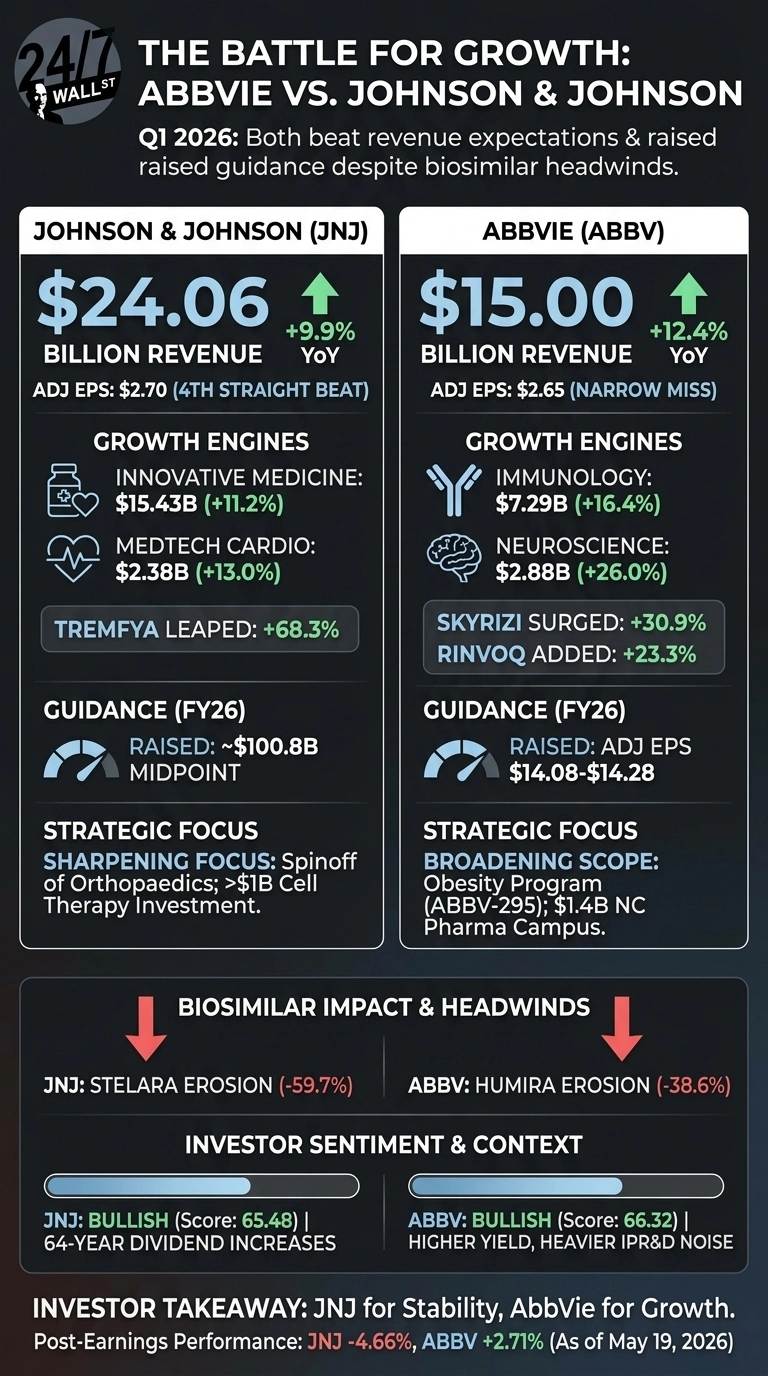

Johnson & Johnson (NYSE:JNJ | JNJ Price Prediction) and AbbVie (NYSE:ABBV) both posted Q1 2026 results that beat revenue expectations and prompted raised full-year guidance. JNJ leaned on a diversified pharma plus MedTech engine. AbbVie leaned almost entirely on immunology. Both face biosimilar headwinds, yet each chose a different way to outgrow them.

TREMFYA and Cardiovascular Carry JNJ. Skyrizi Carries AbbVie.

JNJ delivered revenue of $24.06 billion (+9.9% YoY) and adjusted EPS of $2.70, a fourth straight beat. Innovative Medicine led with 11.2% growth, powered by DARZALEX at $3.96 billion (+22.5%) and TREMFYA leaping 68.3% as it absorbs STELARA patients.

MedTech Cardiovascular climbed 13%, with Shockwave up 18.5%. CEO Joaquin Duato called the quarter “a strong start to 2026”, and the company raised its FY26 revenue outlook to a midpoint of $100.8 billion.

AbbVie reported $15 billion in revenue (+12.4%), but adjusted EPS of $2.65 narrowly missed consensus after a $744 million IPR&D charge clipped earnings by $0.41. Skyrizi reached $4.48 billion (+30.9%) and Rinvoq added $2.12 billion (+23.3%), more than offsetting Humira’s 38.6% decline. CEO Robert Michael said the firm is “off to an excellent start in 2026”.

A Diversified Giant Meets a Concentrated Specialist

The strategic split is meaningful. JNJ is sharpening focus by spinning off DePuy Synthes Orthopaedics and pouring over $1 billion into Pennsylvania cell therapy manufacturing.

AbbVie is going the opposite way, broadening into obesity through ABBV-295, a non-incretin candidate showing weight reduction in Phase 1, while committing $1.4 billion to a North Carolina campus.

| Lens | JNJ | AbbVie |

| Core Bet | Oncology, immunology, cardio devices | Skyrizi and Rinvoq immunology |

| Biosimilar Drag | STELARA -59.7% | Humira -38.6% |

| Dividend Story | 64 straight annual hikes | Higher yield, heavier IPR&D noise |

JNJ’s $330 million in litigation charges and 55.4% drop in free cash flow are real overhangs. AbbVie’s 32.9% GAAP tax rate and trenibotE Complete Response Letter add their own friction.

The Next Test Is Pipeline Conversion

I am watching whether TREMFYA can sustain that 68% growth trajectory while DARZALEX FASPRO combinations roll out in multiple myeloma. The December 8, 2026 Enterprise Business Review will reveal how the post-separation JNJ will be framed.

For AbbVie, the Skyrizi subQ Crohn’s filing and the ABBV-295 obesity readouts are the catalysts that matter. JNJ shares are down 4.66% since filing, while ABBV is up 2.71%, suggesting investors are giving the immunology growth story a slight edge for now.

Why I Lean Toward JNJ for Stability, AbbVie for Growth

If I want defensive ballast, JNJ wins for me. Diversification, a $551 billion balance sheet, and that 64-year dividend record are hard to replicate. The trade-off is slower top-line growth and unresolved talc litigation.

If I want torque, AbbVie is the more interesting bet. Skyrizi and Rinvoq are still scaling, and the obesity optionality is real, even if accounting noise from IPR&D charges keeps GAAP earnings messy. Reddit and news sentiment land bullish on both, with composite scores of 65.48 for JNJ and 66.32 for AbbVie. I would split exposure rather than choose, treating JNJ as the anchor and AbbVie as the growth lever.

Contact [email protected] for any questions or corrections.