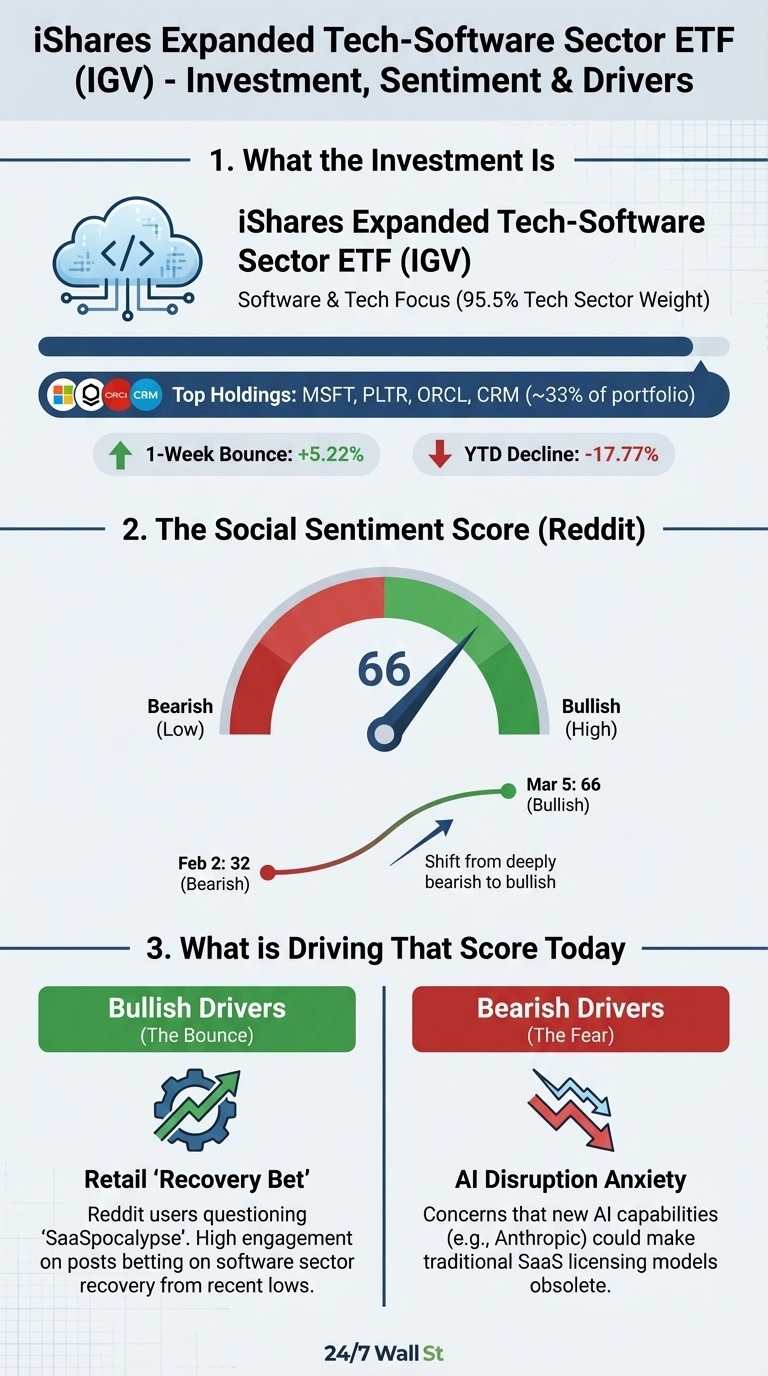

One of the more volatile tech funds, the iShares Expanded Tech-Software Sector ETF (NYSEARCA:IGV) has bounced 5.13% over the past week, reversing after a collapse that left the fund down 18% year-to-date from a December 31 starting price of $105.69. Retail sentiment on Reddit has followed, flipping from deeply bearish in early February to a score of 66 as of March 5. The question investors are wrestling with: can the underlying SaaS business models of IGV’s top holdings sustain revenue and margins in an AI-disrupted environment, or is the re-rating still incomplete?

The selloff had a clear trigger as Anthropic’s new AI automation capabilities accelerated an already-nervous market in early February, with IGV falling across multiple sessions as traders questioned whether AI agents were making traditional SaaS licensing models obsolete.

Reddit’s “SaaSpocalypse” Debate Hits a Turning Point

During the trough, r/stocks lit up with a post that captured the retail mood precisely. As one commenter wrote, “the market is pricing in a full collapse of the SaaS model, but most of these companies still have multi-year contracts and sticky enterprise customers”: a post on r/stocks titled “Investors are placing massive bets on a software sector recovery”.

Investors are placing massive bets on a software sector recovery

by u/[OP] in stocks

That post drew 124 upvotes and 58 comments, the highest engagement in the entire dataset. By February 23, tone had shifted toward contrarian buying, with r/TheRaceTo10Million posting:

Updated thoughts on buying IGV ETF or single SaaS stocks? Is the SaaSpocalypse overblown and irrational? Buy the blood now?

by u/[OP] in TheRaceTo10Million

One commenter on the r/TheRaceTo10Million post wrote: “the market is pricing in a full collapse of the SaaS model, but most of these companies still have multi-year contracts and sticky enterprise customers.”

The post got 13 upvotes and 19 comments, signaling early contrarian positioning before the recovery materialized.

Three reasons the bearish case hasn’t fully resolved:

- AI agents are increasingly embedded directly into enterprise workflows, eroding the value of standalone SaaS subscriptions that make up the bulk of IGV’s holdings

- Goldman Sachs characterized the selloff as “indiscriminate repricing” but only recommended four names with specific structural advantages, not a broad sector recovery

- IGV’s one-year return of -9% lags the Invesco QQQ Trust’s +20.25% over the same period, reflecting a genuine re-rating of the sector’s fundamental earnings outlook

Where IGV Goes From Here

Dan Niles of Niles Investment Management noted that “narrative follows price,” warning that recent price gains may be rationalizing themselves rather than reflecting a genuine fundamental shift. He identified database, security, and high-production-cost gaming software as the sub-sectors best positioned post-shakeout, noting that the sub-sector divergence suggests the broad fund may not capture the recovery as efficiently as targeted positions in those specific categories. IGV’s top four holdings, Microsoft, Palantir, Salesforce, and Oracle, represent roughly 33% of the portfolio, so the fund’s fate is heavily tied to whether those names, including Microsoft (NASDAQ:MSFT | MSFT Price Prediction), Palantir (NYSE:PLTR), Salesforce (NYSE:CRM), and Oracle (NYSE:ORCL), can defend their earnings quality and competitive moats heading into the next earnings cycle.

Contact [email protected] for any questions or corrections.