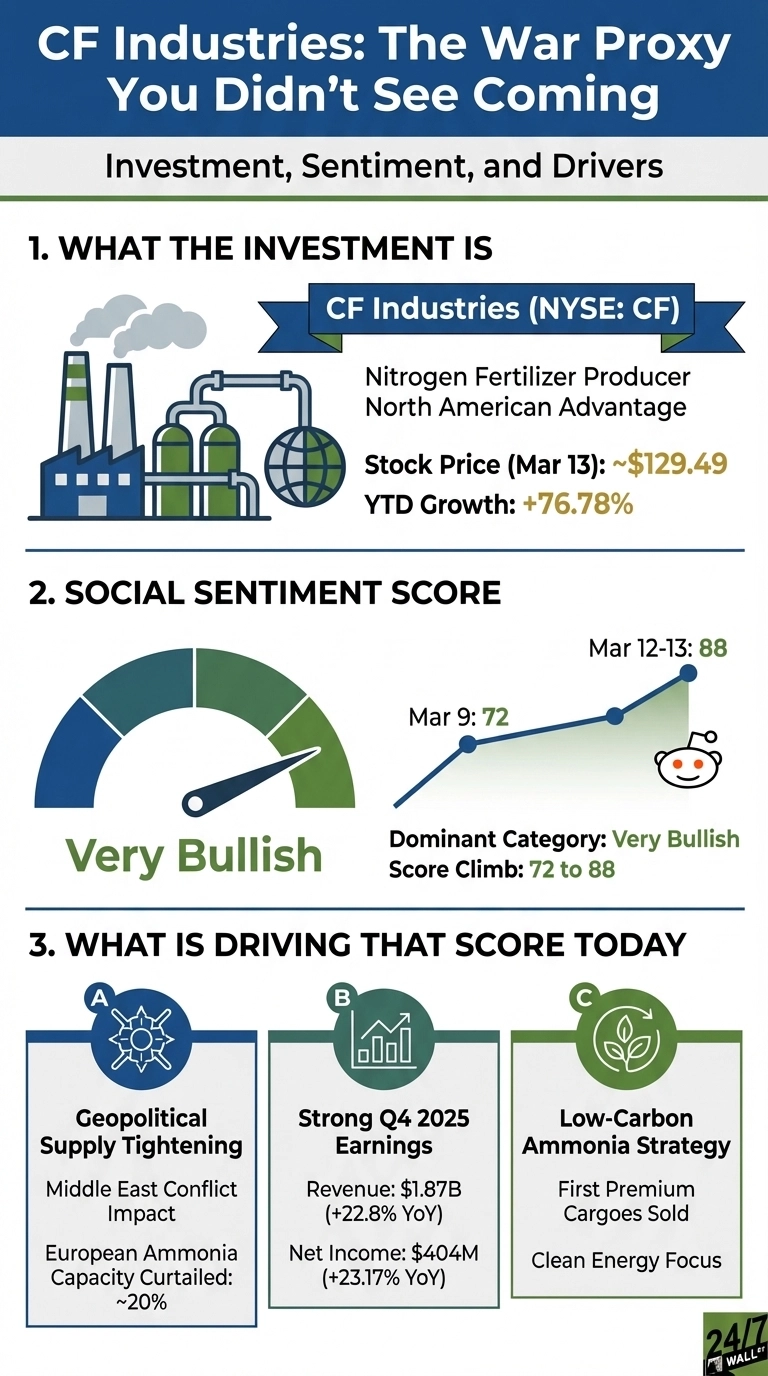

The world’s largest producer of ammonia, CF Industries (NYSE:CF | CF Price Prediction) shares hit an all-time high this week, up 67.6% year-to-date as escalating Middle East conflict tightened global nitrogen supply and sent fertilizer prices surging. CF is trading around $129.60 on Friday after pulling back from a $136 close on March 12. The thesis is straightforward right now, even amid international disarray, as Iran and the Strait of Hormuz handle a meaningful share of global fertilizer flows, and CF is one of the few large-scale North American producers positioned to fill that gap at a structural cost advantage.

Reddit Found CF Before the Headlines Did

Retail sentiment climbed from 72 on March 9 to a sustained 88 by March 12, with r/wallstreetbets driving most of the volume. The geopolitical angle surfaced first in r/stocks, where the post “Not just oil….but also fertiliser…one third passes through the Hormuz” drew early attention to the supply disruption.

Not just oil….but also fertiliser…one third passes through the Hormuz

by u/stocks_poster in stocks

In “$CF 100k++ gainz in one day, thank you Value Investors for the fertilizers heads up”, the poster wrote: “Saw the fertilizer Hormuz thread in r/stocks last week and loaded up on CF calls — paid off big today.” That post reached 192 upvotes and 65 comments by Friday morning. The bullish case rests on three pillars:

- Roughly 20% of European ammonia capacity and 25% of urea capacity are currently curtailed, removing a major supply source from global markets

- CF posted full-year revenue of $7.08 billion, up 19.1% year-over-year, with Q4 gross margin expanding to 38.5% from 34.6% versus the prior year

- North American natural gas costs remain far below European feedstock prices, giving CF a durable margin advantage as long as that spread holds

Solid Earnings, Fragile Geopolitical Premium

The good news for investors closely watching the stock is that this rally is not purely speculative, as CF beat Q4 EPS estimates by $0.11 to $2.59 versus the $2.48 consensus, and full-year adjusted EBITDA grew to $2.89 billion from $2.28 billion in 2024. Barclays raised its price target to $120, citing favorable nitrogen market forecasts, though the stock has already blown past that level. Prediction markets assign only a 19.5% probability to the Iran conflict resolving by March 31, suggesting the supply-disruption narrative has room to persist in the near term.

CF’s Blue Ammonia Bet Changes the Long-Term Story

Even if the geopolitical tailwind fades, CF is building a second act. The Blue Point joint venture with JERA and Mitsui targets low-carbon ammonia production in Louisiana, and the Yazoo City carbon capture project with ExxonMobil (NYSE:XOM) is targeting a 2028 startup. CF already sold its first certified low-carbon ammonia cargoes at premium prices in Q3 2025. Analysts will be watching whether the clean ammonia platform can support a higher valuation floor once the geopolitical premium fades.