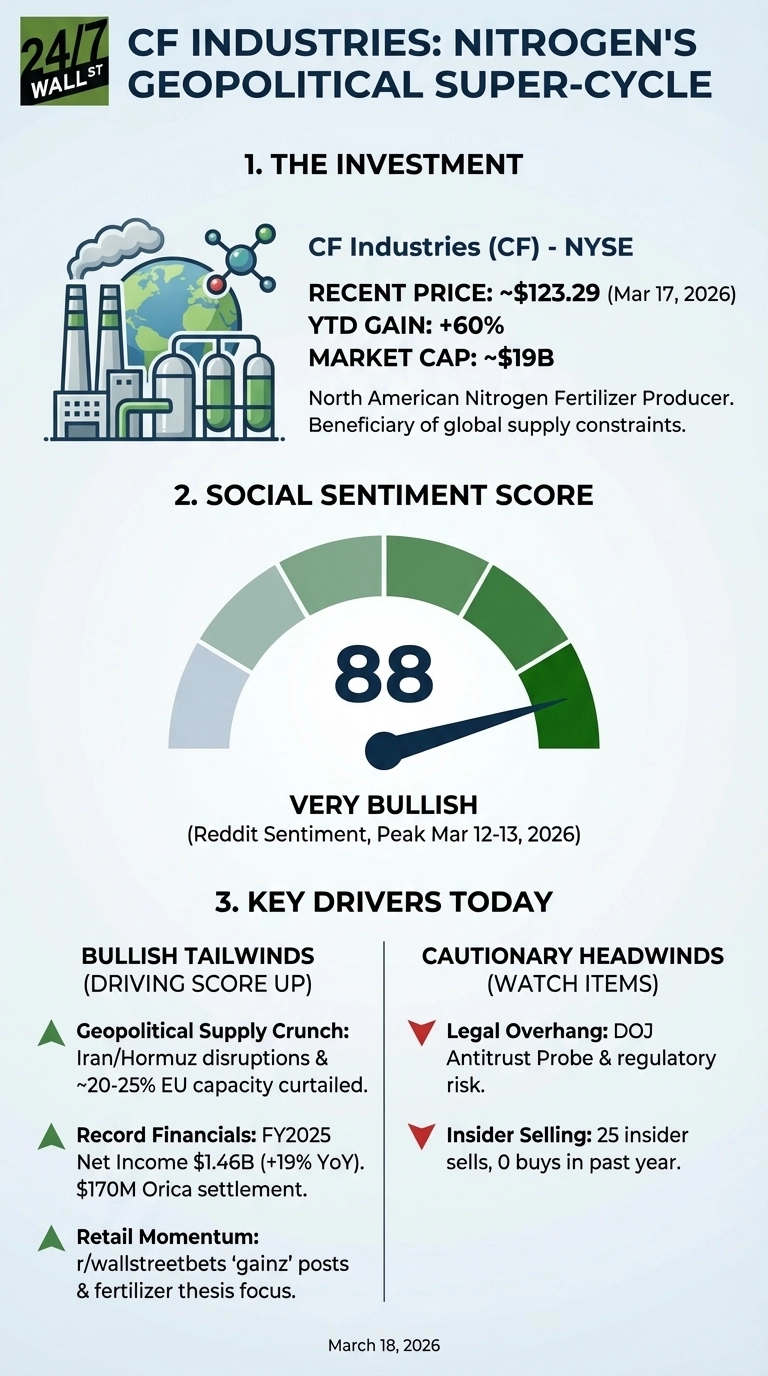

A leading global manufacturer of hydrogen and nitrogen products, CF Industries (NYSE:CF | CF Price Prediction) has surged 59% year-to-date amid Iran-linked supply disruptions, which have tightened global nitrogen markets, with shares reaching $123.29 as of March 17. But the rally drawing retail investors is also drawing federal regulators, raising a question Reddit has not fully priced in: is CF sitting on a geopolitical windfall, or walking into a legal trap?

The fundamentals are hard to argue with as CF reported Q4 2025 revenue of $1.87 billion, beating estimates by 7%, with gross margin expanding to 40.9% from 34.4% a year earlier. Other good news included full-year net income of $1.455 billion, up 19%. Additionally, a $169.5 million cash settlement from Orica, announced March 16, added a near-term cash tailwind. Then came the headwind: a DOJ antitrust probe that put a legal overhang on what had been a clean supply-disruption story.

Reddit Found the Hormuz Trade Early

Sentiment on CF climbed from 72 on March 9 to 88 by March 12-13, driven by two waves. The geopolitical angle broke first in r/stocks, where a post titled “Not just oil….but also fertiliser…one third passes through the Hormuz” framed CF as a direct beneficiary of Middle East supply chain disruption, arguing that CF Industries stands to benefit as one-third of global fertiliser supply passes through the Strait of Hormuz and any disruption removes a major competing supply source from world markets.

Not just oil….but also fertiliser…one third passes through the Hormuz

by u/[post_author] in stocks

Days later, r/wallstreetbets lit up with gains posts.

$CF 100k++ gainz in one day, thank you Value Investors for the fertilizers heads up

by u/wallstreetbets_poster in wallstreetbets

That post reached 212 upvotes and 70 comments by March 13. The structural case behind the enthusiasm:

- ~20% of European ammonia capacity and ~25% of European urea capacity are currently curtailed, removing a major competing supply source from global markets

- CF’s 97% FY 2025 capacity utilization sits 10% above North American peers, giving it maximum leverage on tight pricing

- Russian nitrogen exports run approximately 15% below pre-war levels, and Chinese urea exports remain restricted under strict quotas

The Legal Overhang Institutional Investors Are Watching

The bull case collides with a pattern institutions have noticed, as insiders tracking the stock have logged 25 sales and zero buys over the past year, including director and former CEO Anthony Will selling 57,364 shares worth $6.27 million on March 9 and W. Will selling 81,651 shares at $126.56 on March 13. Barclays, AustralianSuper, and the Public Sector Pension Investment Board all trimmed or cut positions in February and March. The analyst consensus is “Hold” with a price target near $101, well below where shares trade today.

Mosaic (NYSE:MOS), focused on phosphate and potash rather than nitrogen, is idling lower-margin Brazilian facilities amid weak U.S. phosphate demand. CF’s nitrogen focus and North American gas cost advantage put it in a structurally different position. The key watch item is how the DOJ probe develops: formal price-fixing charges could unwind the geopolitical premium faster than the supply disruption that built it.