Chasing yield feels safe. A high-dividend ETF paying monthly, a covered-call fund with a flashy distribution rate. But investors who have parked capital in income-first vehicles over the past decade have quietly watched the compounding machine of the Nasdaq-100 leave them behind. Invesco QQQ Trust (NYSEARCA:QQQ | QQQ Price Prediction) makes the case that for investors with time on their side, QQQ’s return record makes a concrete case for prioritizing growth over income.

What QQQ Actually Is (and Isn’t)

QQQ tracks the Nasdaq-100 Index, holding roughly 100 of the largest non-financial companies listed on the Nasdaq. No banks, no insurance companies, no yield-heavy utilities. What you get instead is a concentrated bet on the businesses that have driven most of the equity market’s returns over the past generation: semiconductor makers, cloud platforms, consumer internet giants, and biotech leaders.

At just net expense ratio is 18 basis points, QQQ is one of the most cost-efficient ways to access mega-cap technology. The portfolio is deliberately concentrated — Information Technology alone makes up nearly 49% of the portfolio, with Communication Services adding another 16% — reflecting a deliberate tilt toward the sectors that have driven most of the equity market’s gains over the past generation.

Apple anchors the fund at 8.8% of the fund, followed by Microsoft at 7.5% and Nvidia at 5.9% — three companies whose combined market leadership in hardware, cloud, and AI infrastructure reflects the Nasdaq-100’s tilt toward platform-scale businesses. The roughly 0.5% dividend yield makes clear that QQQ is built for capital appreciation, not income.

The Return Engine: Compounding Business Growth

QQQ generates returns because the companies inside it grow their earnings, expand their margins, and reinvest cash into new revenue streams. That reinvestment is the compounding engine, and it is why the fund’s long-term return record looks the way it does.

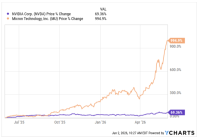

QQQ’s long-term return record reflects the compounding power of its underlying businesses. The fund has returned 454% over the past decade and 90% over the past five years, driven by earnings growth and margin expansion across its largest holdings. That stands in sharp contrast to the current 10-year Treasury yield of 4.2%, which locks in a nominal return that barely keeps pace with inflation, while QQQ’s underlying businesses have historically compounded at multiples of that rate.

Does the Strategy Deliver in Practice?

Over long periods, yes, but with real turbulence along the way. The VIX currently sits at 25, up 18% over the past month, reflecting genuine market unease. QQQ is down about 3% year-to-date as of mid-March. Reddit sentiment around the fund has been consistently bearish in recent weeks, with one widely circulated discussion on r/investing centered on concentration risk from a potential SpaceX IPO forcing passive Nasdaq-100 funds to absorb a massive new position. These are real short-term concerns.

But QQQ’s return record was built through periods exactly like this one. The VIX hit 52 in April 2025 during a sharp market stress event, and the fund recovered strongly from that same period. Volatility is the price of admission for the returns QQQ has historically delivered.

The Tradeoffs Worth Understanding

Concentration is the most significant structural risk. Nearly half the fund sits in a single sector, and the top ten holdings represent an outsized share of total performance. When tech sentiment turns, QQQ feels it more acutely than a broad market index. Investors who need steady income cannot rely on QQQ’s minimal dividend to fund living expenses.

The rate environment adds another layer. The Fed has cut rates by 75 basis points since last year, which generally supports growth stock valuations by reducing the discount rate applied to future earnings. Any reversal would pressure QQQ’s highest-multiple holdings disproportionately.

QQQ has historically appealed to growth-oriented investors with a multi-year time horizon who can tolerate sector-concentrated volatility. The fund’s minimal dividend makes it a poor fit for income-focused strategies.