Phillips 66 (NYSE:PSX) has been one of the energy sector’s standout performers, with shares up 5.60% over the past week, 21.21% over the past month and 41.02% year-to-date. The stock recently touched a 52-week high of $185.37, with shares currently trading around $184.12. The Street consensus target sits at $162.33, but Raymond James is making a bolder call, raising its price target to $205 while maintaining an Outperform rating. That target stands well above consensus and implies meaningful upside from current levels. Can PSX realistically reach $205 by end of 2026?

Raymond James’s $205 PSX Prediction

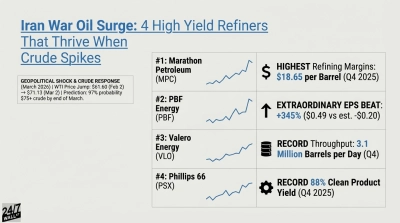

Raymond James raised its target from $175 to $205, anchoring the thesis in geopolitical tailwinds reshaping refining economics. WTI crude surged from $65.87 on Feb. 27 to $91.85 by March 13 as Middle East tensions escalated. Raymond James acknowledges that short-term refiners may struggle to fully capture “spiky” near-term margins, but argues that forward strip margins suggest considerably higher earnings potential in Q2 and beyond, with medium-term upside likely to dominate market focus as elevated refining margins persist well after the conflict subsides.

Key Drivers of PSX Stock Performance

- Refining margin expansion: Worldwide realized refining margins nearly doubled, reaching $12.48 per barrel in Q4 2025 versus $6.08 per barrel in Q4 2024. Phillips 66 management is bullish on 2026, with commercial leadership noting that “if you look toward the start of spring turnarounds, we believe the refining system will have trouble keeping up with demand” , a structural setup supporting sustained margin compounding.

- WRB acquisition and heavy crude leverage: Acquiring the remaining 50% of WRB Refining increased Phillips 66’s exposure to Canadian heavy crude differentials by 40%. Management notes that each dollar of crude differential widening is worth $140 million in yearly earnings , a sensitivity that amplifies returns as heavy crude dips remain favorable.

- Shareholder return engine: Phillips 66 has distributed $14.3 billion to shareholders since July 2022, with a current annual dividend of $4.75 per share and a 2.69% dividend yield. CFO Kevin Mitchell’s cash flow framework targets approximately $1.5 billion in annual debt reduction over the next two years, alongside growing buybacks.

What Will It Take for PSX to Reach $205?

With 400,744,000 shares outstanding, a $205 price target implies a market capitalization in the range of $82 billion. Reaching that level requires three conditions: sustained elevated refining margins through mid-2026 as Middle East supply risks persist, continued execution on the cost reduction roadmap targeting $5.50 per barrel in controllable costs by 2027, and a strong Q1 2026 earnings report on April 29, 2026 that validates the margin windfall thesis.

The primary risk is a rapid geopolitical de-escalation that collapses crude prices and compresses refining spreads before Phillips 66 can fully capture the margin upside. With record refining yields, a strengthened midstream platform, and a management team that delivered “our best year ever for safety performance” alongside a doubling of refining margins in Q4, Raymond James’s $205 target reflects a credible multi-quarter earnings trajectory worth watching.