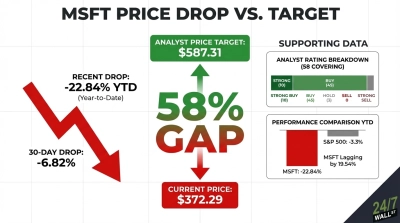

Microsoft (NASDAQ:MSFT | MSFT Price Prediction) investors have endured a punishing start to 2026. The stock is down roughly 25% in the first quarter, on track for its steepest quarterly decline since the fourth quarter of 2008 — nearly two decades ago — when shares plunged 27% amid the global financial crisis.

Among the so-called Magnificent Seven tech giants, Microsoft has been the clear laggard while the group as a whole has fallen about 14%. Yet as the sell-off deepens, a contrarian question emerges: Has the market overreacted, leaving one of the world’s most dominant software and cloud franchises trading at levels too attractive to pass up?

The Capex Surge and Growth Jitters

The pressure stems from two overlapping anxieties gripping the broader tech sector. First, Microsoft is pouring record sums into artificial-intelligence infrastructure just as Wall Street grows impatient for visible payoffs in revenue acceleration. Second, fears are mounting that nimble AI startups could bypass traditional software providers altogether, eroding pricing power and margins in Microsoft’s core businesses.

Microsoft’s capital expenditures — including leases — are forecast to hit $146 billion in fiscal 2026, which ends in June. That represents a 66% jump from the $88 billion spent in fiscal 2025, with analysts expecting the figure to climb further to $170 billion in 2027 and $191 billion in 2028. The spending is aimed squarely at expanding Azure’s AI capacity and supporting tools like Copilot across the productivity suite.

Yet the most recent quarterly results showed a modest deceleration in Azure’s growth rate, the first such pause in years. Copilot, despite heavy promotion, has yet to gain broad traction among the hundreds of millions of Microsoft 365 users. The company has responded by reshuffling its AI leadership, a clear signal that executives recognize the need for faster progress. Investors, already wary of the capital intensity, are asking whether this heavy spending will translate into the kind of durable revenue lift that justified Microsoft’s premium valuation in prior years.

Adding to the unease is the possibility that enterprises could shift spending directly to pure-play AI providers such as OpenAI or Anthropic. “There is this concern that rather than paying Microsoft, we’ll see more customers go directly to AI vendors,” one portfolio manager told Bloomberg, “which could disrupt the core business or at least pressure pricing and margins.”

Valuation at a Generational Low

The sell-off has compressed Microsoft’s valuation to levels not seen in a decade. Shares now trade below 20 times expected earnings over the next 12 months — the lowest multiple since June 2016. For the first time since 2015, the stock has briefly traded at a discount to the S&P 500. That’s a striking shift for a company long viewed as a growth compounder.

Only a month ago, in late February, the multiple hovered near 25 times — already considered a decade low at the time. The additional 25% drop since then has pushed the valuation into even more compelling territory for long-term investors who believe Microsoft’s entrenched position in enterprise software and cloud computing remains intact.

To be sure, the company still carries a forward multiple slightly above the broader market. But the gap has narrowed dramatically, and the discount to historical norms is hard to ignore given Microsoft’s scale, cash flow, and competitive moat.

Can AI Deliver the Payoff?

Microsoft’s long-term case still rests on its ability to weave AI into every layer of its ecosystem. Copilot is embedded across Word, Excel, Teams, and Azure, giving the company a distribution advantage few rivals can match. Enterprise customers already rely on Microsoft for mission-critical workloads; adding AI capabilities could drive meaningful upsell revenue if adoption accelerates.

Yet near-term hurdles remain. Supply constraints in data centers, power availability, and equipment lead times have limited Azure’s ability to meet demand, a dynamic that has persisted into 2026. Competition from Google Cloud, Amazon Web Services, and standalone AI offerings continues to intensify. User surveys show initial enthusiasm for Copilot often fades once alternatives are tested, and retention rates have lagged expectations.

Still, Microsoft’s balance sheet remains fortress-like, and its history of disciplined execution suggests it can navigate these challenges. The current market reaction appears driven more by sentiment than by any fundamental breakdown in the business model.

Key Takeaway

Microsoft’s worst quarterly performance in nearly 20 years has created a rare valuation reset. While AI-related capex pressures and adoption hiccups justify some caution, the stock’s forward multiple has fallen to its lowest level in a decade — well below historical averages and even briefly below the S&P 500.

For investors with a multi-year horizon who believe Microsoft can convert its massive infrastructure bet into sustained Azure and Copilot growth, the shares now offer an attractive entry point. The near-term risks are real, but the long-term opportunity may be too compelling to ignore.

Contact [email protected] for any questions or corrections.