I’ve been watching the memory semiconductor cycle for years now, and I can’t stop thinking about a comment from a market analyst this week. On a recent TV segment, the analyst argued the selloff in memory and semiconductor names has been completely overdone, and the data backs that up hard.

“DRAM contracts this month, quarter over quarter were up 90 to 95%. We still have massive demand. And you look at companies supplying memory, for example, they’re sold out for the next two years.”

That’s a supply-demand imbalance with receipts.

The Numbers Behind the Claim

Micron Technology (NASDAQ:MU | MU Price Prediction) is the clearest U.S.-listed window into this dynamic. In fiscal Q1 2026, DRAM revenue hit a record $10.8 billion, up 69% year-over-year and up 20% sequentially, with CFO Mark Murphy noting that “prices increased 20%, driven by tight industry DRAM supply, pricing execution, and favorable mix.”

CEO Sanjay Mehrotra was direct: “The gap between the demand and supply for all of DRAM, including HBM, is really the highest that we have ever seen.” He added that “We have completed agreements on price and volume for our entire calendar 2026 HBM supply.” The order books aren’t just full — they reportedly stretch into 2027.

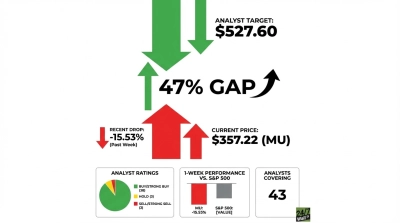

For Q2 FY2026, Micron guided to revenue of $18.70 billion with non-GAAP EPS of $8.42 and non-GAAP gross margins of 68% — all projected records. The stock is up 28.94% year-to-date even after pulling back -10.82% over the past month. That recent dip is exactly what the analyst flagged as overdone.

The Equipment Suppliers Confirm It

The “sold out for two years” thesis shows up clearly in the equipment layer. Applied Materials (NASDAQ:AMAT) reported record DRAM revenue in Q1 FY2026, with DRAM rising to 34% of Semiconductor Systems sales from 27% year-over-year. CEO Gary Dickerson projected semiconductor equipment business growth over 20% in calendar 2026.

Lam Research (NASDAQ:LRCX) posted Q2 FY2026 revenue of $5.34 billion, up 22.1% year-over-year, with CEO Tim Archer pointing to “multi-year outperformance” as the operating framework. Deferred revenue of $2.68 billion as of Q4 2025 signals customers locking in equipment capacity well in advance.

Then there’s NVIDIA (NASDAQ:NVDA), the demand engine at the center of all of it. Data Center revenue hit $62.31 billion in Q4 FY2026, up 75% year-over-year, with Jensen Huang describing “the agentic AI inflection point” as the macro driver. Every GPU cluster NVIDIA ships needs high-bandwidth memory. That’s Micron’s product. That’s the Korean memory names the analyst referenced. The demand is real, contracted, and not going away.

The analyst’s core argument holds up: Micron itself can only meet 50% to two-thirds of demand from several key customers. When a company with record margins and record revenue still can’t fill its order book, the selloff in its stock is a window.