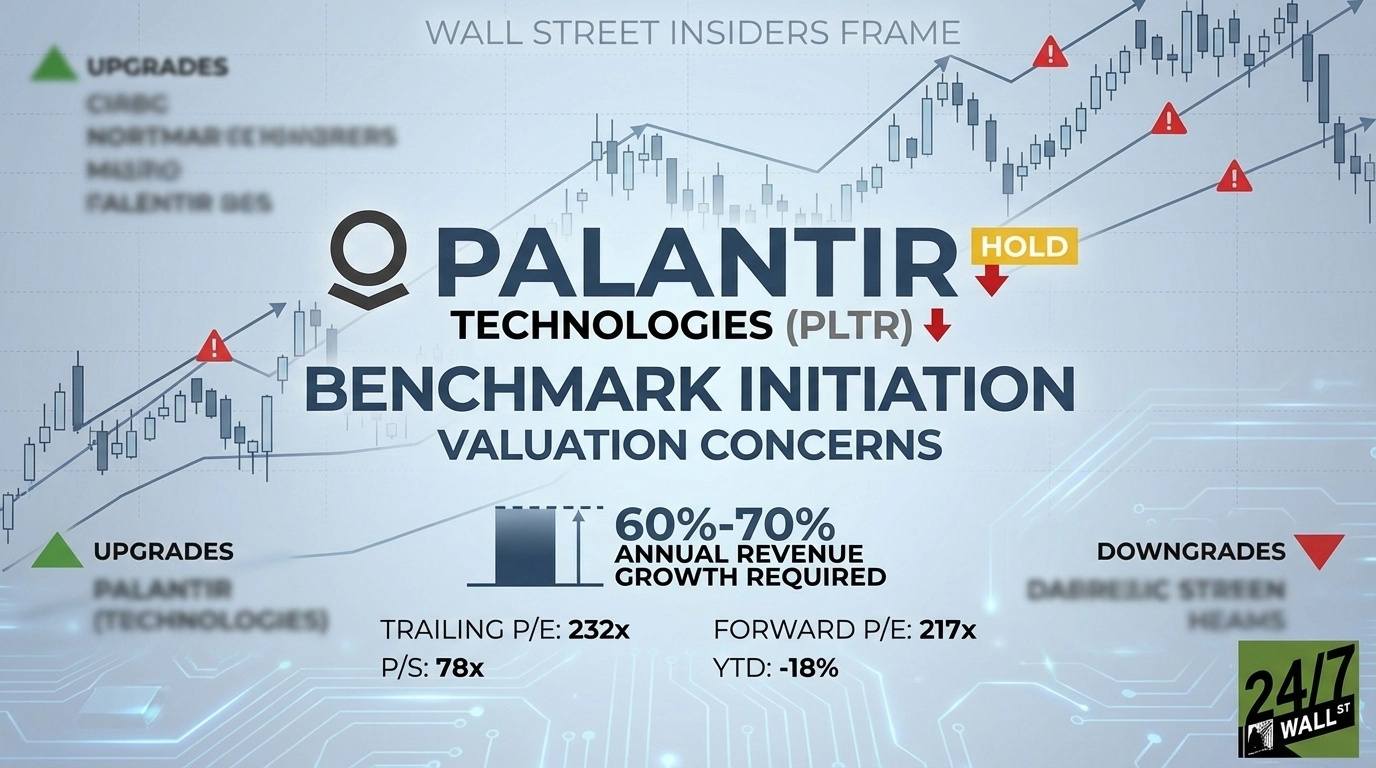

Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction) received a Hold initiation from Benchmark analyst Yi Fu Lee. The core concern: at current prices, the stock requires sustained 60% to 70% annual revenue growth to avoid potential downside. That is an extraordinarily high bar to maintain, and Benchmark is not convinced the company can clear it indefinitely.

| Ticker | Company | Firm | Action | New Rating |

|---|---|---|---|---|

| PLTR | Palantir Technologies | Benchmark | Initiation | Hold |

The Analyst’s Case

Benchmark’s Yi Fu Lee acknowledges Palantir’s AI-powered automation platform, which delivers real-time decision support to government and commercial customers, and recognizes the company’s strong fundamentals and leadership under CEO Alex Karp. The problem is valuation. The current price appears to price in near- to mid-term growth at the high end of guidance, leaving little room for any growth deceleration. Benchmark is essentially signaling that the risk-reward is too uncertain to recommend buying at current levels.

Company Snapshot

Palantir operates three core platforms: Gotham for government clients, Foundry for commercial clients, and AIP, its Artificial Intelligence Platform. The company posted Q4 2025 revenue of $1.406 billion, up 70% year-over-year, beating estimates by 6%. U.S. commercial revenue surged 137% year-over-year to $507 million, while U.S. government revenue grew 66% to $570 million. The company carries a Rule of 40 score of 127% and a market cap of $334.795 billion..

Why the Move Matters Now

Palantir’s own guidance for FY 2026 calls for revenue of $7.19 billion at the midpoint, representing 61% year-over-year growth. That figure lands squarely inside the 60% to 70% range Benchmark says is required just to justify current prices. In other words, management’s best-case scenario barely clears the valuation hurdle. The stock trades at a trailing P/E of 232x and a forward P/E of 217x, with a price-to-sales ratio of 78x. These multiples leave almost no margin for error. The stock is already down 18% year-to-date through March 31, even as the underlying business continues to execute at a high level. Despite blowout Q4 results, shares fell 12% the day after earnings were reported, a telling signal about how much growth is already baked into the price.

What It Means for Your Portfolio

Palantir’s operational performance is genuinely impressive. Adjusted EPS came in at $0.25 versus an $0.18 estimate, free cash flow reached $791.4 million in Q4, up 73%, and customer count grew 34% year-over-year to 954. The bull case is real. Benchmark’s Hold initiation is a reminder that valuation matters as much as execution, even exceptional businesses can be poor investments when priced for perfection. For long-term investors, the real question is whether it can sustain 60% to 70% growth for long enough to grow into a valuation that already prices in near-perfection.