Palo Alto Networks (NASDAQ:PANW | PANW Price Prediction) just earned a Buy initiation from Benchmark with a $200 price target, anchored to a compelling profitability thesis: The company is on track to achieve nearly Rule of 60 status in FY2026. For long-term investors watching the cybersecurity sector, this call deserves attention.

So far this year, the stock is down 10.33%, and over the past year, shares have slipped 6.11%. But PANW has rallied over the past month, gaining 7.12%.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| PANW | Palo Alto Networks | Benchmark | Initiation | N/A | Buy | N/A | $200 |

The Analyst’s Case

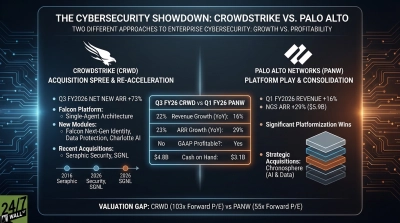

Benchmark frames Palo Alto Networks as an AI-driven cybersecurity leader delivering integrated platform solutions for superior protection, faster response, and lower costs. The firm identifies it as a core sector holding meeting key SaaS investment criteria: technology leadership, high AI defensibility, a $360 billion-plus total addressable market, consistent beat-and-raise performance, and strong profitable growth targeting nearly Rule of 60 in FY2026.

The Rule of 60 benchmark combines revenue growth rate and free cash flow margin. Palo Alto is guiding for FY2026 revenue growth of 22-23% year-over-year alongside an adjusted free cash flow margin of 37%, putting the combined sum within striking distance of that threshold. Management is also targeting 40%+ adjusted free cash flow margin by FY2028, signaling the profitability trajectory is still building.

Company Snapshot

Palo Alto Networks generated $2.594 billion in revenue in Q2 FY2026, beating the $2.583 billion consensus estimate. Non-GAAP EPS came in at $1.03, surpassing the 93 cent-estimate by 10%. Next-Generation Security ARR reached $6.30 billion, up 33% year-over-year, and full-year NGS ARR guidance calls for $8.52–$8.62 billion, representing 53%–54% growth.

CEO Nikesh Arora described the dynamic plainly on the earnings call: “We saw continued strength in platformizations, a trend that is accelerating due to AI – customers are keen to both modernize and normalize their cybersecurity stack, aligning them to our approach.”

Why the Move Matters Now

Palo Alto stock has pulled this year and trades below its 200-day moving average of $188.30, well off its 52-week high of $223.61. That reset gives Benchmark’s $200 target meaningful relevance. The broader analyst community agrees: 44 analysts rate the stock Buy or Strong Buy against just 2 Sell ratings, with a consensus price target of $206.97. CEO Arora reinforced conviction with a $10 million personal share purchase in late March, the first major insider buy since 2019.

What Investors Should Watch

Benchmark’s initiation highlights a company with durable platform economics, accelerating NGS adoption, and a credible path toward elite SaaS profitability metrics. The valuation remains elevated at a forward P/E of 42x, so investors should weigh the premium against the growth runway. The pending Chronosphere acquisition at $3.35 billion and the CyberArk deal add integration risk, but also expand the addressable platform. For retirement-focused investors, Palo Alto represents a high-quality cybersecurity franchise with a credible path toward elite SaaS profitability metrics.