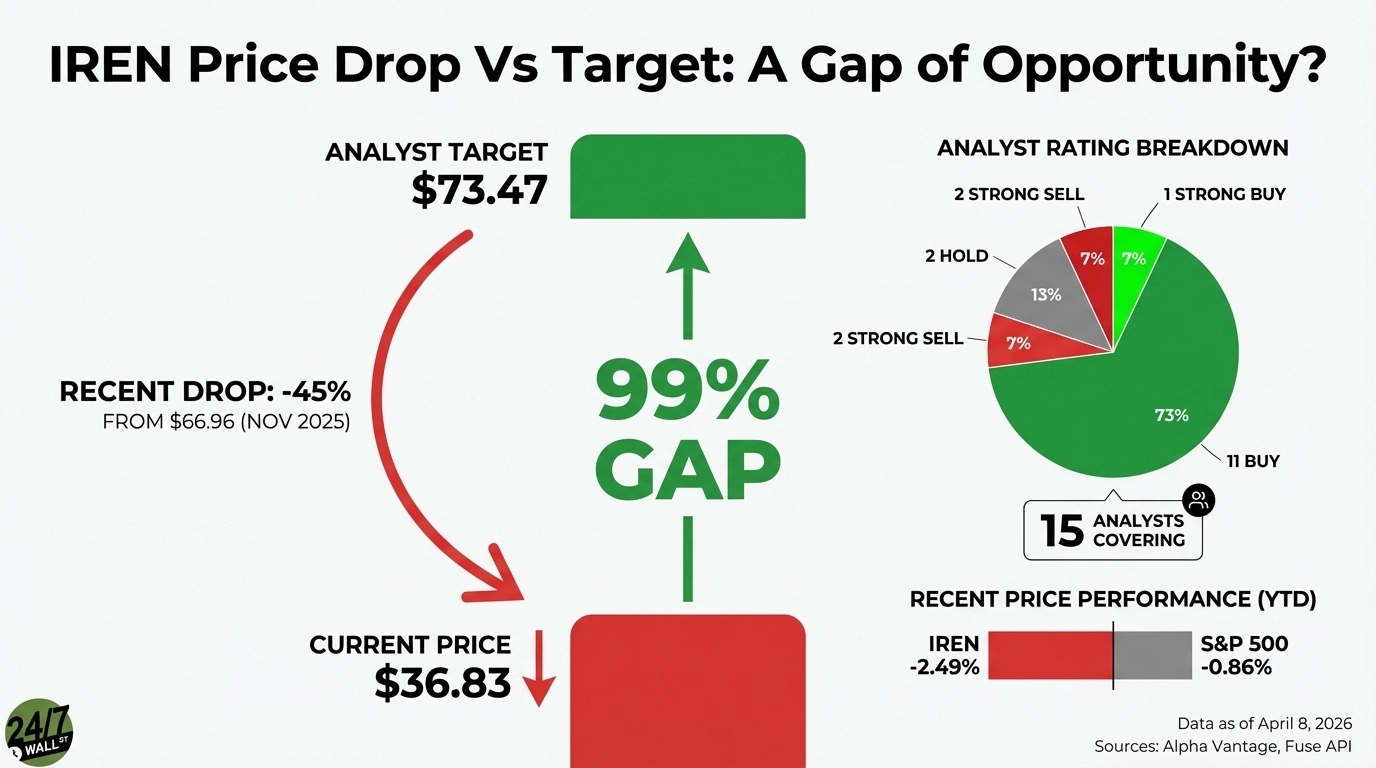

IREN Ltd (NASDAQ:IREN) currently trades at $36.83, while the Wall Street consensus price target sits at $73.47, implying roughly 99% upside from current levels. This level of implied upside stands out and suggests the market may not yet be fully pricing in the company’s earnings power as that contracted revenue begins to materialize.

IREN is a vertically integrated data center company pivoting from Bitcoin mining to AI cloud infrastructure. The company has secured more than 4.5GW of power capacity across North America and landed a $9.7 billion contract with Microsoft for phased GPU deployments at its Childress, Texas campus. The stock traded as high as $76.87 heading into late 2025 before collapsing.

A Revenue Miss During a Critical Transition

IREN’s most recent quarter delivered a revenue miss. Q2 FY26 revenue came in at $184.7 million against a consensus estimate of $226.9 million, an 18.6% miss. Shares fell roughly 12% in the session following results. The revenue shortfall stemmed from deliberate capacity reallocation. CFO Anthony Lewis explained that total revenue was down 23% on the prior quarter primarily on account of lower Bitcoin mining revenue, driven by a reduction in Bitcoin mined as a result of the AI transition, which lowered operating hashrate against the backdrop of an increasing global hashrate, together with lower average Bitcoin prices over the period. IREN chose to shrink its most profitable current business to build its future one.

A net loss of $155.4 million amplified the damage, though most was non-cash. A $219.2 million one-time debt conversion inducement expense and a $31.8 million mining hardware impairment inflated the headline loss. Adjusted EBITDA held at $75.3 million with a 41% margin, better than the 38% margin posted the prior quarter. The operating business remained intact, but headline numbers were ugly enough to do real damage.

Analysts See a $3.4 Billion Revenue Engine That’s Just Getting Started

The bull thesis rests on contracted revenue not yet flowing through the income statement. Chief Commercial Officer Kent Draper confirmed that current annualized run-rate revenue under contract stands at $2.3 billion, comprising roughly $1.9 billion from the Microsoft contract and approximately $0.4 billion from Prince George in British Columbia. The company’s stated target is $3.4 billion in ARR by end of calendar year 2026. Against trailing revenue of $757 million, the gap between current earnings and contracted revenue is the entire investment thesis.

The financing structure is much better than critics acknowledge. IREN secured a $3.6 billion delayed draw term loan from Goldman Sachs and JPMorgan at less than 6% interest, covering 95% of GPU-related capital expenditure for the Microsoft contract. CEO Daniel Roberts stated: “We essentially got the GPUs for next to nothing.” The company also holds approximately $2.8 billion in cash as of January 2026, providing meaningful runway before the revenue ramp materializes.

Analysts are watching GPU deployment velocity at Childress and the Prince George expansion as primary near-term catalysts. Draper noted that customers are seeking longer contract tenures and continuing to provide prepayments, signaling confidence in IREN as a long-term counterparty.. He also highlighted the economics: “Every incremental 200 megawatts can deliver either $300 million-ish through a colo or multiples of that in the billions under a cloud contract.” That revenue-per-megawatt differential explains why analysts maintain their targets.

Trading at Half the Analyst Target

IREN trades at $36.83, against a consensus target of $73.47. The implied upside is approximately 99%. Of the 15 analysts covering IREN, 11 rate it a Buy (including 1 Strong Buy), 2 rate it a Hold, and 2 rate it a Strong Sell. The two Strong Sell ratings reflect concerns around Bitcoin exposure, customer concentration, and execution risk on a buildout at this scale, but overall, this is a heavily bullish read from analysts. The 11 Buy ratings reflect confidence that the contracted revenue pipeline is real and financing is in place to deliver it.

Year to date, IREN is down 2.49% while the S&P 500 is down roughly 0.86% over the same period. The stock’s 52-week range of $5.24 to $76.87 illustrates extraordinary volatility and the stock’s beta of 4.31 means that IREN amplifies every market move in both directions.

The trailing P/E of 25x looks reasonable in isolation, but the forward P/E of 63x reflects how much the bull case depends on future revenue materializing on schedule. A market cap of approximately $11.9 billion prices in significant execution. If the $3.4 billion ARR target is achieved, current valuation looks cheap. If it slips, the multiple has nowhere to hide.

The Bull Case Depends on Revenue Ramp Execution

The bull case strengthens if Microsoft contract revenue begins to show up meaningfully over the next few quarters and British Columbia GPU deployments stay on track. The $2.3 billion in contracted ARR is already in place, financing has been secured, and data centers are actively being built. If execution follows through, the current price starts to look disconnected from the company’s near-term earnings power.

The bear case centers on execution and concentration risk. A sharp drop in Bitcoin prices would pressure the legacy business, while any delays in the AI cloud ramp could push out the timeline for meaningful revenue. The Microsoft contract represents roughly $1.9 billion of the $3.4 billion ARR target, so any issues with that relationship would have an outsized impact. At the same time, the $3.7 billion in convertible notes adds financial leverage that leaves less room for mistakes.

The setup is compelling because the revenue pipeline is real and financing is largely in place, which suggests the gap to analyst targets reflects a legitimate opportunity rather than a pure value trap. That said, this is a high-risk, high-variance story. The next two quarters should make it much clearer whether the revenue ramp is materializing or if execution risk is starting to show up.