Jim Cramer made an argument on a recent Mad Money segment that deserves more attention: the market has been punishing cybersecurity stocks by lumping them in with traditional software, and that categorization is wrong.

“AI isn’t gobbling them, it’s supporting them because it creates so many new vulnerabilities that hackers can exploit.”

Every new AI deployment, every agentic workflow, every GPU cluster spun up in the cloud is a new attack surface. Demand for cybersecurity doesn’t shrink when AI proliferates. It compounds.

CrowdStrike: Securing the AI Stack

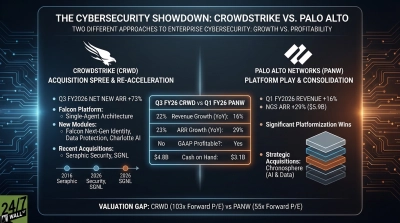

CrowdStrike (NASDAQ:CRWD | CRWD Price Prediction) was up about 6% on the most recent trading day, though the stock is still down about 14% year to date. I’ve been watching CrowdStrike’s ARR trajectory for years now, and the Q4 FY26 numbers are hard to argue with. Ending ARR reached $5.25 billion, up 24% year over year, with record net new ARR of $330.7 million, up 47% year over year. CEO George Kurtz said CrowdStrike is “mission-critical infrastructure — securing AI across every layer from GPU to agent to prompt.” That’s the Cramer thesis expressed in product terms. Falcon Flex ARR hit $1.69 billion, growing over 120% year over year. FY27 revenue guidance is $5.87 billion to $5.93 billion, with non-GAAP EPS of $4.78 to $4.90.

Palo Alto Networks: Platformization Meets AI

Palo Alto Networks (NASDAQ:PANW) rose about 4% on the same session, though it remains down roughly 12% year to date. Cramer argues Palo Alto has nothing to do with traditional software and its business is actually turbocharged by AI. The numbers back that up. Next-Generation Security ARR grew 33% year over year to $6.30 billion in Q2 FY26. CEO Nikesh Arora said “platformizations” are “accelerating due to AI, customers are keen to both modernize and normalize their cybersecurity stack.” Non-GAAP operating margin has held above 30% for three consecutive quarters. Full investor relations detail here.

Palantir: The AI Consultant No One Can Copy

Cramer describes Palantir as “an AI consultant that can’t possibly be duplicated by the AI companies,” and says its stock has been maligned because it became the largest holding in a software index, dragging it down with sector-wide selling. Palantir (NYSE:PLTR) is down about 26% year to date, but the underlying business is accelerating. Q4 2025 revenue grew 70% year over year to $1.41 billion, with U.S. commercial revenue up 137% year over year to $507 million. The Rule of 40 score hit 127%. Prediction markets currently show a 75% probability that PLTR closes higher today, and 47% odds it closes above $136 by end of April.

All three names remain well below recent highs, and macro volatility can extend the pain. Cramer’s observation that stocks “get sold and sold and sold until they’re oversold, and then they bounce for reasons that are not readily accessible” captures the dynamic here. If you believe AI proliferation structurally expands the attack surface, these are businesses whose fundamentals are moving in one direction while their prices have moved in the other. That gap tends to close eventually.

Now, does this mean their stocks won’t drop 8% next time Anthropic does a press release? Unlikely. But I’m not treating those events as a sign to sell. Rather, as always, I’m focused on them as entry points into stocks I want to own for the long-term.

Contact [email protected] for any questions or corrections.