Tech dinasour Microsoft (NASDAQ:MSFT | MSFT Price Prediction) remains a compelling long-term holding. The stock is down 12.9% year-to-date as of mid-April 2026, sitting at $420.26 against a 52-week high of $552.24. That gap reflects a significant discount from recent highs. Here’s why I’m loading up on it.

The Revenue Backlog Nobody Is Talking About Enough

The commercial remaining performance obligation stands out as a key metric. In Q2 FY2026, that figure hit $625 billion, a 110% surge year-over-year. That is contracted, committed future revenue already on the books. One quarter earlier, it stood at $392 billion, up 51% year-over-year. The acceleration from 51% growth to 110% growth tells me enterprise customers are locking in for years.

A large piece of that is structural: OpenAI is contracted to purchase an incremental $250 billion of Azure services, and Microsoft holds a roughly 27% stake in OpenAI valued at approximately $135 billion, with IP rights extended through 2032. The IP rights extension through 2032 and contracted Azure purchases provide long-term revenue visibility.

Azure Growth Is Not Slowing Down

Azure grew 33% in Q3 FY2025, then 39% in Q4 FY2025, then 40% in Q1 FY2026, then 39% again in Q2 FY2026. For the full fiscal year 2025, Azure surpassed $75 billion in annual revenue, up 34%. Forward guidance for Q3 FY2026 calls for 37% to 38% growth.

CEO Satya Nadella said: “We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises.”

Microsoft Cloud revenue crossed $51.5 billion in a single quarter for the first time in Q2 FY2026, up 26% year-over-year. The trajectory reflects sustained acceleration, with Microsoft Cloud revenue crossing $51.5 billion in a single quarter for the first time.

The Earnings Machine Keeps Beating

Microsoft has beaten EPS estimates in every quarter tracked closely. The beats are not marginal: 7.59% in Q3 FY2025, 7.99% in Q4 FY2025, 12.78% in Q1 FY2026, and 7.57% in Q2 FY2026. Q2 FY2026 net income came in at $38.46 billion, up 59.52% year-over-year, and operating cash flow reached $35.76 billion, up 60.41%.

The company returned $12.7 billion to shareholders in Q2 FY2026 alone, a 32% increase year-over-year. At a trailing P/E of 26x and a forward P/E of 20x, The valuation represents a reasonable multiple for a business generating $136 billion in annual operating cash flow and compounding it faster each year.

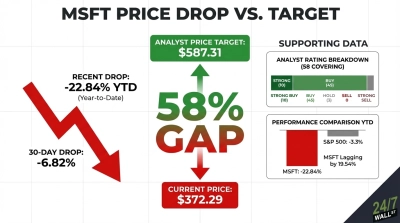

The analyst community agrees: 55 analysts rate it a buy or strong buy, with zero sell ratings, and a consensus price target of $580.87.

What Could Go Wrong, and Key Risks to Monitor

The real risk is that the $29.88 billion in quarterly capital expenditures, up 89% year-over-year, does not generate projected returns, and AI infrastructure spending becomes a drag rather than a driver. But the contracted backlog of $625 billion, consistent Azure acceleration, and five straight quarters of earnings beats suggest spending is already converting to revenue.

The five-year base case projects a total return of 78.11% at a 12.24% annualized rate, and even the bear case shows 30.06% upside over five years.

A business with $625 billion in contracted revenue, Azure growing near 40%, and a profit margin of 39% does not stay at a 12.9% year-to-date discount for long. The valuation discount may attract investors seeking long-term exposure to the AI infrastructure buildout.

Contact [email protected] for any questions or corrections.