The two largest names in enterprise software have been bruised, and the smart money is using the discount to add exposure. Oracle (NYSE:ORCL | ORCL Price Prediction) trades near $190 against a Wall Street consensus target of $242.10, while Microsoft (NASDAQ:MSFT) sits around $405 versus a target of $561.56. Both gaps run well into double digits.

Both companies are core AI infrastructure operators whose underlying earnings have accelerated through the drawdown. Microsoft has posted four consecutive EPS beats. Oracle just delivered its first quarter in over 15 years of 20%+ growth in both organic revenue and non-GAAP EPS. Yet the S&P 500 is up 8% year to date while these two have lagged badly.

Oracle: Capex Panic Is Drowning Out A $553 Billion Backlog

Oracle has been punished for its balance sheet rather than its growth. Capital expenditures reached $48.25 billion in the latest quarter, free cash flow swung to negative $24.7 billion, and non-current debt expanded to $124.7 billion from $85.3 billion. Management has telegraphed up to $50 billion in additional debt and equity financing for data centers. That overshadowed a strong Q3 FY2026 earnings report: EPS of $1.79, revenue of $17.19 billion, and IaaS revenue up 84% YoY.

Analysts are looking past the CapEx anxiety. Remaining performance obligations exploded to $553 billion, up 325% YoY, representing multi-year contracted revenue from AI customers including Meta and NVIDIA. Management raised FY2027 revenue guidance to $90 billion and projects OCI revenue scaling to $144 billion by FY2030. Wedbush’s Dan Ives raised his target to $275, arguing Wall Street is fixated on capex optics while ignoring contracted demand.

The ratings split is decisively bullish: 7 Strong Buy, 28 Buy, 8 Hold, and 1 Sell. The 52-week range shows the rout, with a high of $343.01 against a low of $134.57. Seeking Alpha called a bottom with 36% potential upside to consensus, citing $30 billion in secured funding and $29 billion in customer-prepaid contracts.

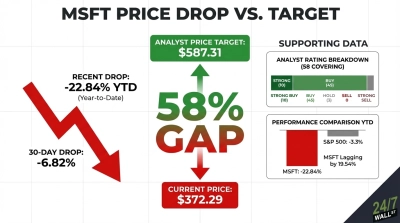

Microsoft: A Capex Hangover Obscuring The $37 Billion AI Engine

Microsoft’s selloff is more textbook. Shares are down 15% year to date against that 8% gain for the S&P 500. Investors balked at $30.88 billion in Q3 FY2026 capex (up 84% YoY), OpenAI-related investment losses rising to $3.1 billion in Q1 FY26, and concerns that circular cloud contracts with OpenAI and Anthropic are flattering results.

The bull case rests on scale and visibility. Q3 FY2026 EPS hit $4.27 against a $4.07 consensus, the fourth straight beat. Azure grew 40% YoY. The AI business reached $37 billion annualized run rate, up 123% YoY. Commercial remaining performance obligations nearly doubled to $627 billion. The restructured OpenAI partnership locked in $250 billion of incremental Azure commitments and extended Microsoft’s IP rights through 2032.

Wall Street remains overwhelmingly positive. Of 54 analysts, 51 are bullish and zero are bearish, broken down as 9 Strong Buy, 42 Buy, and 3 Hold. The consensus target sits at $561.56, well above the current $401.42 quote, implying upside in the high double digits. Trailing P/E of 25 and forward P/E of 21 look reasonable for a company growing earnings 23% at a 46% operating margin. Wealth Enhancement Trust Services initiated a 56,211-share position worth $27.19 million, ranking it as their fourth-largest holding.

Where I Land: 2 Different Risk-Reward Profiles

Microsoft fits a quality-compounding-at-a-discount profile here. The capex worry is real, but four straight beats, a $627 billion RPO, and 51 of 54 analysts bullish say the AI spend is producing actual returns. The bear case holds if the circular-revenue critique proves right and Azure growth decelerates below 30%. I’d buy Oracle here if you can stomach the balance sheet.

Oracle suits investors who can stomach the balance sheet. The $553 billion RPO is one of the most striking forward indicators in megacap tech, and customer prepayments are quietly de-risking the capex story. The bear case holds if rates stay elevated or if one or two major AI customers stumble, because contract concentration is real.

Analyst targets are one data point, never a guarantee. Between these two, I lean Microsoft for risk-adjusted return given its fortress balance sheet. Oracle offers higher absolute upside with materially more execution risk. Owning both makes sense if AI infrastructure is your thesis, and the institutional buying patterns suggest plenty of professional investors already agree.

Contact [email protected] for any questions or corrections.