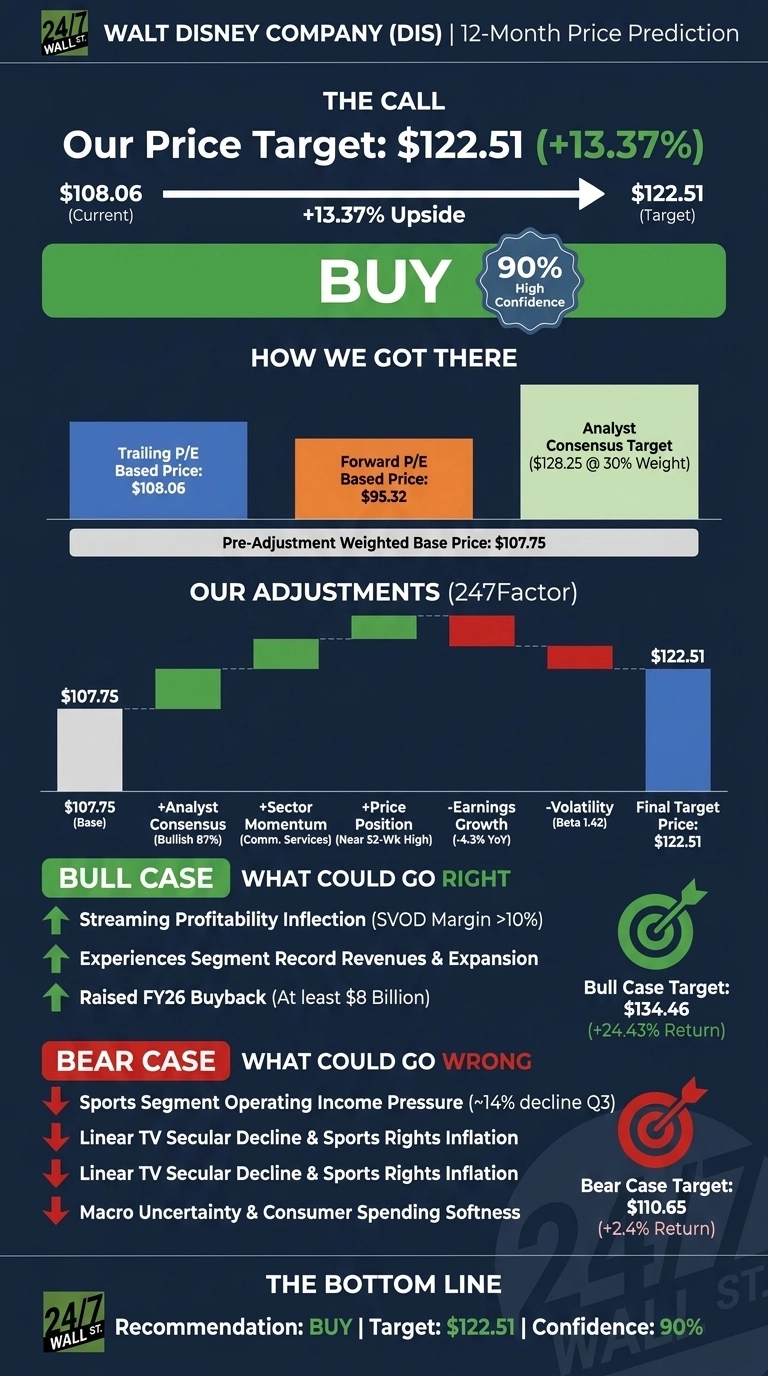

Our 24/7 Wall St. price target for Disney (NYSE:DIS | DIS Price Prediction) is $122.51 over the next 12 months, implying 13.37% upside from the current price of $108.06. We rate Disney a buy with high confidence (90%) following a strong fiscal Q2 earnings report, an inflection in streaming margins, and management’s raised buyback. The setup is constructive: shares trade 4% below the 52-week high, sentiment is firming, and FY26 EPS guidance points to double-digit growth.

| Metric | Value |

|---|---|

| Current Price | $108.06 |

| 24/7 Wall St. Price Target | $122.51 |

| Upside | 13.37% |

| Recommendation | BUY |

| Confidence | 90% |

A Quarter That Reframed the Story

Disney has rallied 6.67% in the past week and 12.24% in the past month, though shares remain down 5.02% year to date.

The catalyst was fiscal Q2 2026: adjusted EPS of $1.57 topped consensus by 4.98%, and revenue of $25.16 billion rose 6.55% year over year. Operating income jumped 31.29% to $4.60 billion. Entertainment SVOD posted its first double-digit operating margin (10.6%), with operating income up 88% to $582 million. Experiences delivered record fiscal Q2 revenue of $9.48 billion with domestic per-capita spending up 5%.

The Case for $134 and Higher

Bulls focus on three levers. First, streaming: SVOD margin expanded from 8.4% in Q1 2026 to 10.6% in Q2 2026, with 196 million Disney+/Hulu subscribers providing scale.

Second, Experiences keeps compounding, with international parks up 11% and capital-light expansions in Abu Dhabi and Japan extending the runway.

Third, capital return: management raised the FY26 buyback to at least $8 billion. Wall Street’s consensus target of $128.25 reflects 7 Strong Buy and 20 Buy ratings. Our bull-case scenario points to $134.46 within 12 months, a 24.43% total return.

Barclays analyst Kannan Venkateshwar raised the firm’s price target on Disney to $135 from $130 and keeps an Overweight rating on the shares following the earnings report. Further, Guggenheim analyst Michael Morris raised the firm’s price target on Disney to $120 from $115 and keeps a Buy rating on the shares and JPMorgan raised the firm’s price target on Disney to $139 from $138 and keeps an Overweight rating on the shares.

What Could Go Wrong

Net income fell 24.73% year over year in Q2, and Q1 free cash flow swung to -$2.278 billion. Bulls would counter that the cash flow hit reflects deferred California wildfire tax payments, with management reaffirming $19 billion in full-year operating cash flow. Sports remains pressured, with Q3 operating income guided down 14% on higher programming costs, and the NFL deal is $0.03 dilutive to FY26 EPS. Linear TV decline, macro softness, and tariff risk round out the watch list. Our bear case lands at $110.65, essentially flat.

Our Take

The price target of $122.51 backs a buy at 90% confidence. The streaming margin inflection is the factor that tips the scale. The bull thesis strengthens if SVOD margins hold above 10% and Experiences sustains mid-single-digit operating income growth into H2. The thesis weakens if Sports rights inflation widens and consumer spending at parks visibly softens.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $122.51 |

| 2027 | $137.04 |

| 2028 | $149.42 |

| 2029 | $164.16 |

| 2030 | $164.97 |

These projections assume Disney sustains streaming profitability and Experiences momentum. Material upside or downside could come from ESPN DTC scaling and the cadence of sports rights cost inflation.

Contact [email protected] for any questions or corrections.