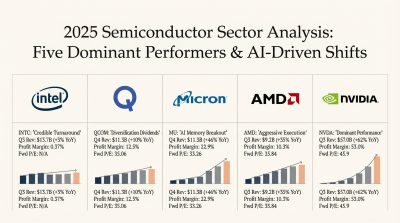

Intel (NASDAQ:INTC | INTC Price Prediction) and AMD (NASDAQ:AMD) both reported Q1 2026 earnings in the past month, and the results tell two very different stories about how x86 chipmakers are riding the AI buildout.

Intel is mid-turnaround under new CEO Lip-Bu Tan, leaning on foundry ambitions and CPU partnerships. AMD is already cashing checks on AI accelerators, with Data Center now its profit engine.

Restructuring Pain at Intel, Pure Acceleration at AMD

Intel posted revenue of $13.6 billion, up 7.2% YoY, with Data Center and AI jumping 22% YoY to $5.052 billion. The headline ugly was a $3.728 billion GAAP net loss tied to a $4.07 billion Mobileye goodwill impairment.

Lip-Bu Tan framed it as deliberate, saying the quarter marked a “sixth consecutive quarter of revenue above our expectations.” Non-GAAP gross margin came in at 41%, up 1.8 percentage points, which is progress but still a long way from competitive.

AMD looked like a different species. Revenue hit $10.253 billion, growing 37.9% YoY, with Data Center surging 57% to $5.775 billion. Non-GAAP EPS of $1.37 beat the $1.29 estimate, and free cash flow exploded 252.96% to $2.566 billion. Lisa Su called it “an outstanding first quarter, driven by accelerating demand for AI infrastructure.”

Vertical Integration vs. Merchant Accelerator

| Lens | Intel | AMD |

| Core Bet | Foundry plus Xeon CPUs for inference | Instinct GPUs and EPYC for hyperscalers |

| Marquee Win | Xeon 6 as host CPU for NVIDIA DGX Rubin NVL8 | Meta 6 GW Instinct deployment with custom MI450 |

| Non-GAAP Gross Margin | 41.0% | 55% |

| Key Vulnerability | Foundry losses, capex intensity | TSMC dependency, HBM supply |

Intel is spending heavily, with capex of $4.963 billion against negative free cash flow. The Intel 18A ramp in Arizona and the Terafab project alongside SpaceX, xAI, and Tesla are real, but Foundry profitability remains the open question.

AMD is buying its capacity from TSMC and converting it straight into operating leverage, with operating income up 83.13% YoY.

The Next Test Is Whether Intel Can Convert Hype Into Foundry Orders

Intel guided Q2 revenue to $13.8 billion to $14.8 billion with non-GAAP EPS of just $0.20. AMD guided Q2 to roughly $11.2 billion, implying about 46% YoY growth. I will be watching whether MI450 ships on schedule for Meta and whether Intel 14A secures an external anchor customer before any further pause risk.

Insider activity is telling too: Intel directors are retaining vested equity, while AMD’s Lisa Su sold heavily on May 13 at prices between $433 and $457.

Why I Lean AMD Today, but Keep Intel on the Watchlist

On the fundamentals, AMD looks like the cleaner long-term story today. The forward P/E of 67 is rich, yet the combination of accelerating Data Center growth, 55% gross margins, and signed multi-gigawatt deals with Meta and OpenAI provide visibility that Intel currently lacks.

For turnaround-oriented investors with patience for messy quarters, Intel’s PEG ratio of 0.5 and the Lip-Bu Tan reset offer real optionality, especially if Foundry crosses into profitability. A named 14A external customer would be the key signal that Intel’s strategy is taking hold.

Contact [email protected] for any questions or corrections.