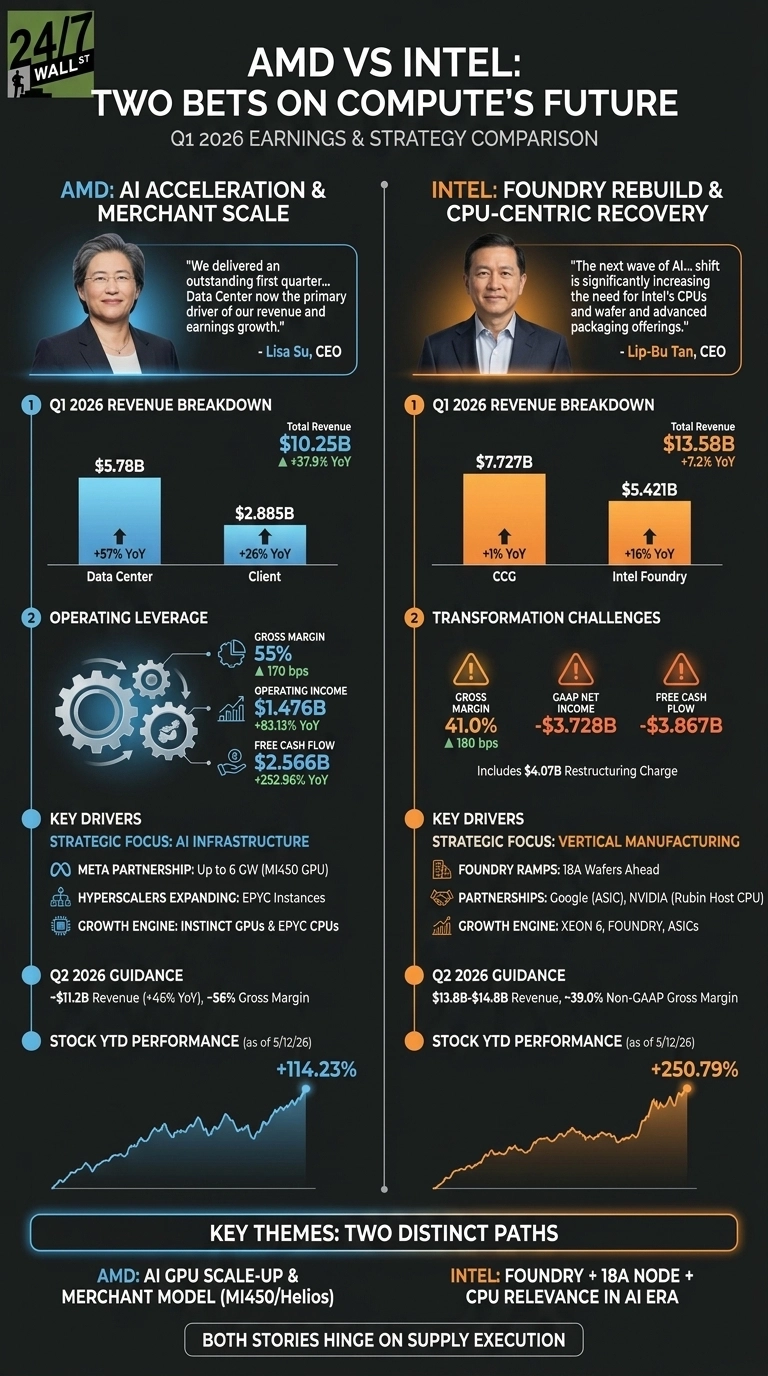

AMD (NASDAQ:AMD | AMD Price Prediction) and Intel (NASDAQ:INTC) both reported Q1 fiscal 2026 results within two weeks of each other, and the contrast is striking. AMD posted $10.25 billion in revenue powered by AI accelerators, while Intel delivered $13.58 billion alongside a sprawling foundry rebuild. Two chipmakers, two very different bets on where compute is heading.

Data Center Carries AMD. Foundry Surprises at Intel.

AMD’s Data Center segment hit $5.78 billion, up 57% YoY, with Lisa Su calling it a “structural shift in our business”. EPYC server CPUs grew more than 50%, and Instinct GPU shipments accelerated. Free cash flow more than tripled to $2.566 billion. That is the kind of operating leverage investors rarely see from a company this size.

Intel told a messier story. Revenue rose 7.18% YoY, but a $4.07 billion restructuring charge tied largely to Mobileye drove a GAAP net loss of $3.728 billion. Underneath, Intel Foundry climbed 16% YoY and DCAI grew 22%. Lip-Bu Tan called it the “sixth consecutive quarter of revenue above our expectations”. Progress is real, even if the headline loss looks ugly.

| Driver | AMD | Intel |

| Growth engine | Instinct GPUs, EPYC | Xeon 6, Foundry, ASICs |

| Gross margin | 55% | 41.0% |

| Marquee partner | Meta (6 GW) | NVIDIA Rubin host CPU |

Merchant AI Scale vs. Vertical Manufacturing Bet

AMD is doubling down as a merchant chip vendor. The 6 GW Meta deployment uses a custom MI450-based GPU and Helios rack-scale architecture, with shipments starting in the second half. Add OpenAI, AWS, Google Cloud, Azure, and Tencent expanding 5th Gen EPYC instances, and you get why Su now expects server CPU TAM to grow at greater than 35% annually, reaching over $120 billion by 2030.

Intel is going the other direction. Tan wants Intel to own the silicon and the fab. “18A wafers are now running ahead of internal projections,” he told analysts, and Intel joined the TeraFab project with SpaceX, xAI, and Tesla.

The custom ASIC business is already at a run rate north of a billion dollars, per CFO David Zinsner. That is encouraging, though Intel’s $3.867 billion negative free cash flow shows how much capital the foundry path consumes.

Supply Is the Next Test

Both CEOs said demand exceeds supply. Su guided Q2 to approximately $11.2 billion, implying 46% YoY growth, with server CPU revenue expected to grow more than 70% YoY.

Intel guided to $13.8 billion to $14.8 billion. I will watch whether AMD can land MI450 volume in the second half without margin slippage, and whether Intel 18A yields hold as Panther Lake volumes ramp six to seven times sequentially. Both stories hinge on execution.

Why I Lean Toward AMD on Quality, But Keep Intel on the Watchlist

For my own money, AMD’s quarter looks cleaner. A 55% gross margin, 95% net income growth, and named hyperscaler commitments give me visibility I can underwrite. The stock is up 114.23% year to date, so I am not chasing it here.

Intel offers turnaround optionality for investors evaluating the foundry pivot. Shares have climbed 250.79% year to date as the foundry narrative gained credibility, but the GAAP losses and CHIPS Act overhang keep me cautious. Intel’s case depends largely on whether 14A wins customers in 2027.

Contact [email protected] for any questions or corrections.