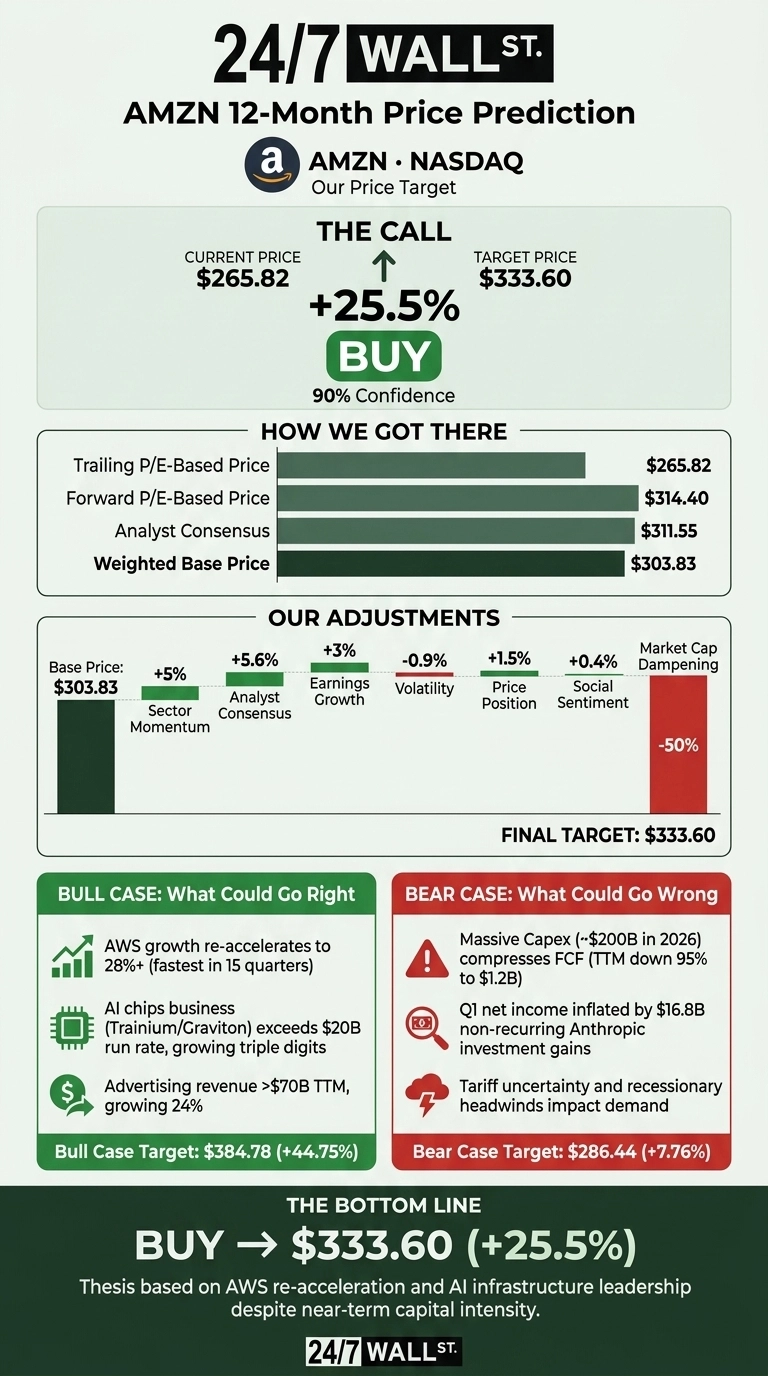

Our Amazon (NASDAQ:AMZN | AMZN Price Prediction) view is straightforward: the cloud and AI infrastructure story is accelerating, the model still has room to re-rate, and the recent pullback has reset valuation for long-term investors. The 24/7 Wall St. price target points to $333.60 over the next 12 months, an upside of 25.5% from $265.82. Our recommendation is buy with high confidence at 90%.

| Metric | Value |

|---|---|

| Current Price | $265.82 |

| 24/7 Wall St. Price Target | $333.60 |

| Upside | 25.5% |

| Recommendation | BUY |

| Confidence Level | 90% |

AWS Re-acceleration Reset the Story

Amazon is up 15.16% year to date and 27.41% over the last 12 months, though shares have cooled 2.83% in the past week off the $278.56 52-week high.

The catalyst was Q1 2026, filed April 29, 2026: EPS of $2.78 vs. a $1.73 consensus, a fifth consecutive beat. Revenue hit $181.52 billion, up 16.6%, while AWS posted $37.59 billion at 28% growth, the fastest pace in 15 quarters at a 37.7% operating margin.

CEO Andy Jassy framed the moment plainly on the call: “We’re in the middle of some of the biggest inflections of our lifetime, we’re well positioned to lead.”

The Case for $384+

The bull setup is the AI infrastructure flywheel. OpenAI has committed 2 GW of Trainium capacity beginning 2027, Anthropic is securing up to 5 GW, and Trainium2 is fully subscribed at 1.4M chips. The chips business is already at a $20 billion run rate growing triple digits.

Advertising crossed $70 billion TTM at 24% growth, and Rufus is contributing $12B in incremental annualized sales. Our bull case carries AMZN to $384.78 over 12 months, a 44.75% return. The Wall Street consensus of $311.55 from 62 buy and 5 hold ratings (zero sells) anchors the optimism.

What Could Go Wrong

The risks are real. Capex is exploding to $200B in 2026, and TTM free cash flow has compressed to $1.2B. Q1 net income was inflated by $16.80B in non-recurring Anthropic gains, a point Reddit’s r/investing has flagged repeatedly. Long-term debt has climbed to $119.1B, and management explicitly flagged tariff and recessionary headwinds in Q2 guidance.

Bears would counter, fairly, that the FCF compression reflects deliberate investment in the AI infrastructure moat. Our bear case settles at $286.44, still a 7.76% positive return. Insider activity has tilted toward net selling, and Polymarket’s May 2026 market still clusters around $256 (45.5%) and $280 (43.5%), suggesting near-term crowd skepticism about a fast move higher.

The Bottom Line

The 24/7 Wall St. price target of $333.60 with 25.5% upside and 90% confidence reflects a simple thesis: AWS reaccelerating to 28% growth on a base of nearly $150B annualized changes the earnings trajectory.

The setup looks constructive if AWS holds the high-20s growth rate through 2026 and operating margin stays above 13%. The thesis weakens if capex blows past $220B without commensurate AWS bookings or if tariffs hit retail unit growth.

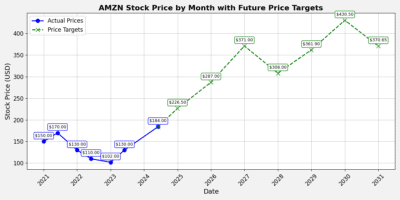

Amazon Price Prediction 2026-2030

Looking further ahead, here is where our model projects AMZN could trade as the AI infrastructure cycle matures.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $333.60 |

| 2027 | $357.05 |

| 2028 | $422.50 |

| 2029 | $471.41 |

| 2030 | $518.05 |

These projections assume Amazon continues monetizing Trainium capacity, AWS margins stabilize above 35%, and capex peaks in 2026-2027. Significant upside or downside could result from the pace of AI demand, regulatory action, or a sharper consumer downturn.

Contact [email protected] for any questions or corrections.