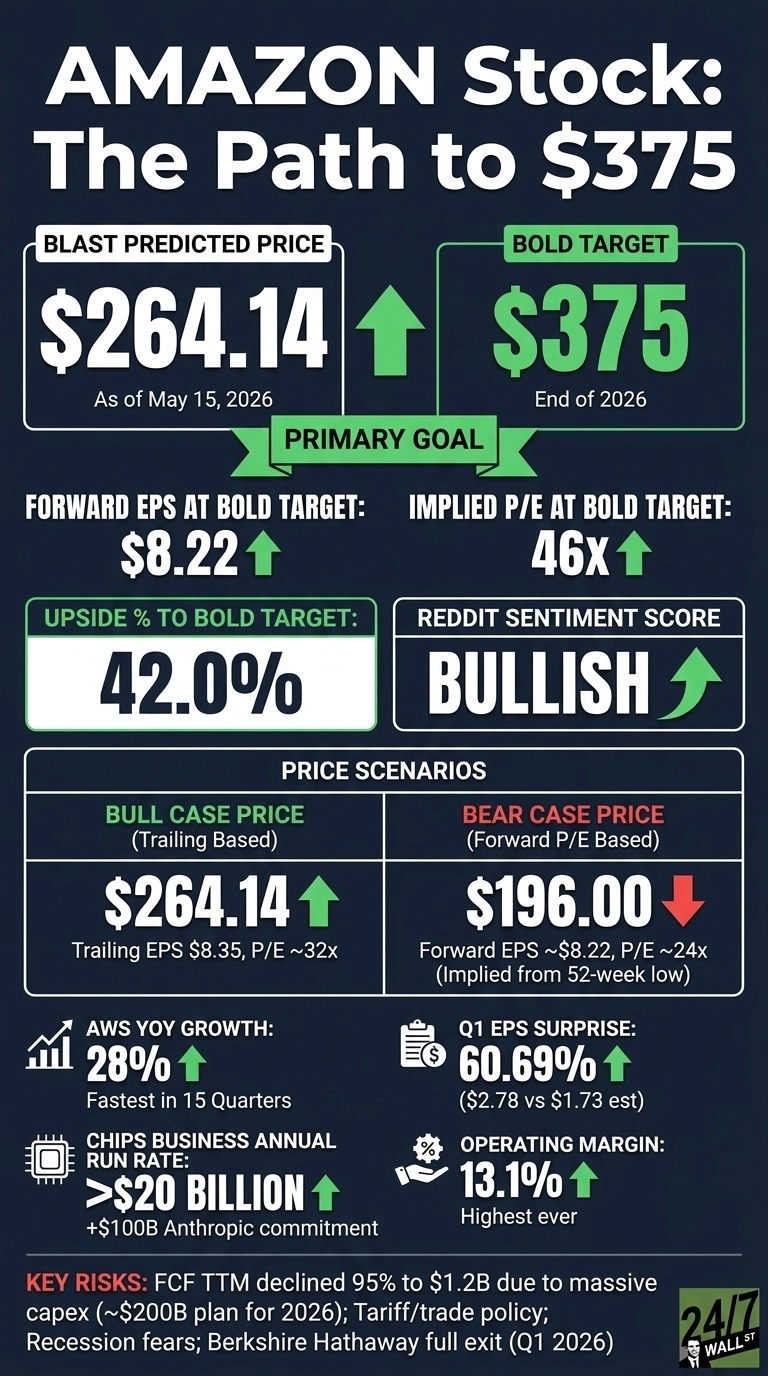

Amazon (NASDAQ:AMZN | AMZN Price Prediction) just delivered a quarter that should make every bear reconsider. AWS grew 28% year over year, the fastest pace in 15 quarters, the chips business crossed a $20 billion annual run rate, and EPS came in at $2.78 versus a $1.73 estimate.

Yet shares closed at $264.14 on May 15, well below where fundamentals suggest they should be. Can Amazon reach $375 a share in 2026?

Why Amazon Shares Are Stuck Despite Record AWS Growth

Despite Q1 results that CFO Brian Olsavsky framed around a 13.1% operating margin, the highest ever, shares have given back recent gains. Momentum has cooled. The MACD histogram flipped negative on May 11 and deepened to -2.0243 by May 15, while RSI dropped from 81.1 on May 6 to 58.6 in nine sessions.

Two overhangs explain it. First, Berkshire Hathaway fully exited its Amazon position in Q1 2026, a headline that traveled. Second, free cash flow has collapsed under a $200 billion 2026 capex plan, with $43.2 billion spent in Q1 alone. With a beta of 1.468, AMZN amplifies every macro wobble.

Wall Street Sees Modest Upside. I Think They Are Too Conservative

The consensus target sits at $311.55, with 14 Strong Buys, 48 Buys, 5 Holds, and zero Sells among 67 analysts. That is bullish, but the price target feels stale. Quarterly EPS growth ran at 74.8% year over year and revenue at 16.6%. Yet consensus implies less than 18% upside from here.

The Street appears anchored to old growth assumptions before AWS reaccelerated and before the chips business hit a $50 billion implied standalone run rate. With $364 billion in AWS backlog and Trainium nearly fully subscribed through Trainium3, the operating leverage story has years left.

The Path to $375 Per Share

Reaching $375 from today’s price of $264.14 requires a gain of 42%. With forward EPS of roughly $8.22 (derived from the 32 forward P/E), a price of $375 implies a forward P/E of 46x. The consensus target of $311.55 implies roughly 38x, meaning the bold target requires about 7.7x of additional multiple expansion. Can Amazon earn that? Yes, if three things keep working:

- AWS AI revenue is running at over $15 billion with triple-digit growth

- Anthropic committed over $100 billion beyond the backlog

- Trainium is positioned to save AWS tens of billions in CapEx annually

CEO Andy Jassy framed it directly: “We’re in the middle of some of the biggest inflections of our lifetime, we’re well positioned to lead, and I’m very optimistic about what’s ahead for our customers and Amazon.” The single biggest risk is a capex-driven free cash flow squeeze that forces the market to value Amazon on FCF rather than earnings power.

Where Amazon Trades Today vs Its Earnings Power

At $264.14, AMZN trades at roughly 32x forward earnings, with trailing EPS of $8.35 producing a similar 32x trailing multiple. Valuation is reasonable given EPS growth of 74.8% YoY and ROE of 24.3%. Shares sit between the 52-week low of $196 and high of $278.56, closer to the top end. The stock has compounded meaningfully over the past decade, and the current setup pairs that long-run engine with a once-in-a-cycle AI infrastructure buildout.

Is $375 Realistic? My Verdict

Reaching $375 means a 42% gain and a forward P/E of 46x. That is a stretch, but it is achievable. Three things need to go right: AWS holds the 28% growth pace into the back half of 2026, the chips business converts $225 billion in Trainium commitments into reported revenue, and Q2 lands inside the $194 to $199 billion sales guide.

A tariff shock or sharp rate tightening would derail the multiple expansion story quickly. We’ve outlined the blueprint for how Amazon could reach $375 in 2026.

Contact [email protected] for any questions or corrections.