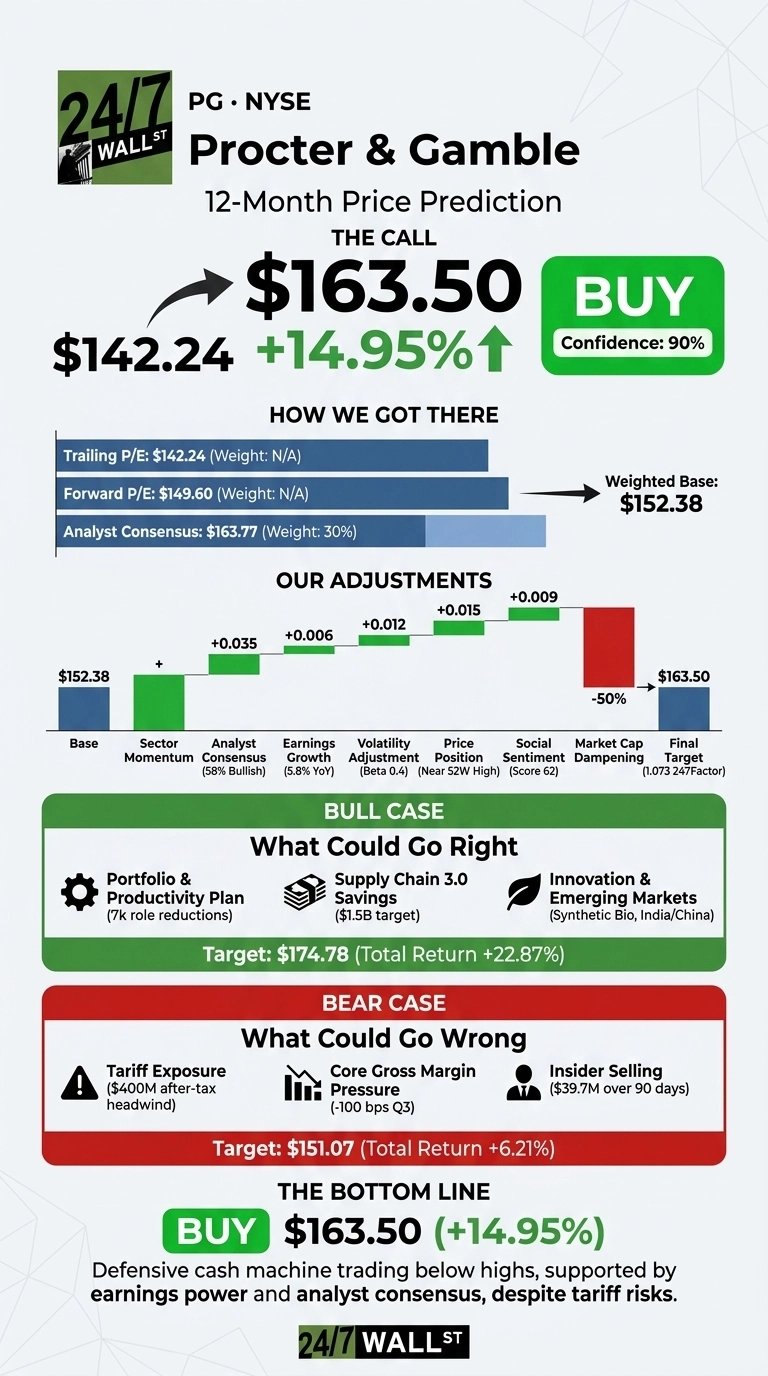

Our 24/7 Wall St. price target for Procter & Gamble (NYSE:PG | PG Price Prediction) is $163.50, implying a 14.95% upside from today’s price. Procter & Gamble trades at $142.24 as of May 13, 2026, with a $330.7 billion market cap and a beta of 0.4.

Our recommendation is buy, with 90% confidence. PG is a defensive cash machine trading well below recent highs, supported by analyst consensus and stable earnings power.

| Metric | Value |

|---|---|

| Current Price | $142.24 |

| 24/7 Wall St. Price Target | $163.50 |

| Upside | 14.95% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Defensive Name That Sold Off Into Earnings Strength

PG is down 7.84% over 12 months, off 3.83% in the past week, and barely positive year to date at +0.69%. Shares sit roughly 14% below the 52-week high of $166.21 and well above the 52-week low of $135.63.

Fundamentals don’t justify the weakness. Q3 FY2026, filed April 24, 2026, delivered Core EPS of $1.59 against a $1.55 consensus, with revenue of $21.23 billion, up 7.4% YoY. Beauty grew 7% organic, and every segment posted growth. CEO Shailesh Jejurikar said the quarter showed “a solid acceleration in top-line results… broad-based growth across product categories and regions.” That marks five consecutive earnings beats.

The Case for $175+

The bull case is credible. Our model’s bull scenario points to $174.78 by May 2027, a 22.87% total return. Drivers include the Portfolio, Supply Chain and Productivity Plan targeting up to 7,000 non-manufacturing role reductions by end of FY2027, plus a Supply Chain 3.0 program aimed at $1.5 billion in cost-of-goods-sold savings. Innovation in synthetic biology, premium Skin Care mix, and emerging-market penetration in India, MEA, and Greater China underpin the multi-year story.

External analysts agree. Simply Wall St’s DCF model pegs PG as 21.3% undervalued, citing a P/E of 21x versus a fair ratio of 24x. Jim Cramer recently flagged the stock as a hedge against economic slowdown given its valuation. The dividend, now at $1.0885 quarterly with a 3% yield, marks PG’s 70th consecutive annual increase.

The Risks Worth Watching

The bear case is real. Tariffs represent a $400 million after-tax headwind, and management flagged FY2026 results toward the low end of guidance. Q3 core gross margin compressed 100 basis points. Zacks issued a Sell rating, citing moderating sales growth and premium valuation. Insiders have sold roughly $39.7 million in shares over the past 90 days.

Bulls argue margin pressure reflects deliberate reinvestment in innovation and demand creation, and that gross productivity savings of 210 basis points partially offset tariff and mix headwinds. Our bear case scenario lands at $151.07, still a 6.21% positive return.

Procter & Gamble Price Prediction 2026-2030

The 24/7 Wall St. price target is $163.50, a buy with 90% confidence. The combination of a defensive sector profile, a beta near 0.4, and analyst consensus of $163.77 on a stock that has absorbed tariff fears tips the scale. The setup favors investors seeking compounding dividends and downside protection, while FY2027 oil-driven cost shocks beyond what management has telegraphed remain the key risk to monitor.

Here is where our model projects PG could trade, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $163.50 |

| 2027 | $176.00 |

| 2028 | $190.00 |

| 2029 | $206.00 |

| 2030 | $224.36 |

These projections assume PG continues executing its integrated growth strategy and productivity plan. Significant upside or downside could result from tariff escalation, raw-material shocks, or accelerated emerging-market expansion.

Contact [email protected] for any questions or corrections.