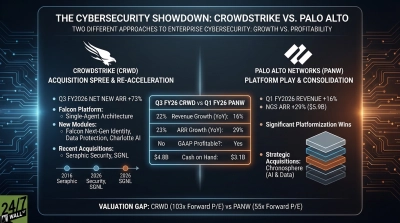

Cybersecurity M&A is reaccelerating in 2026 as platform consolidation, AI disruption, and hyperscaler appetite collide. Cisco/Splunk and Google/Wiz reset the deal calculus, and CrowdStrike’s January 2026 purchase of Seraphic Security and Zscaler’s February 2026 acquisition of SquareX kicked off a browser-security arms race. OpenAI’s Trusted Access for Cyber program in April 2026 effectively anointed Palo Alto, CrowdStrike, and Zscaler as platform consolidators, squeezing sub-scale pure plays. Below are five pure-play vendors most positioned as 2026 acquisition candidates. Treat each entry as an investment thesis.

1. SentinelOne

SentinelOne (NYSE: S | S Price Prediction) is the most-discussed takeout name in the cyber field. The endpoint vendor crossed $1.06 billion annual recurring revenue (ARR) (+23% year over year) in its most recent quarter and posted a record 7% non-GAAP operating margin, yet shares trade at $16.33, down 14.7% over one year and 61.6% from 2021 levels. Market cap stands near $5.6 billion on a 5.64× price-to-sales multiple, well below those of peers like CrowdStrike and Zscaler.

Endpoint protection is core to any platform roll-up. Federal differentiation via newly earned GovRAMP High status sweetens the strategic case for Cisco, Palo Alto, or a hyperscaler. Analyst targets average $18.50 with 24 Buy ratings against 13 Holds. Note that founder-CEO Tomer Weingarten has previously walked away from sale talks, and the company is executing operationally, which reduces urgency.

2. Tenable

Tenable Holdings (NASDAQ: TENB) fits the classic leveraged buyout (LBO) profile: durable cash flow, decelerating growth, sub-scale platform. Q1 FY2026 delivered revenue of $262.06 million (+9.58% year over year) and a 320 bps operating-margin expansion to 23.6%, with FY26 free-cash-flow guidance of $285 million to $295 million. Recurring revenue runs at 96% of total.

The stock trades at $21.31, down 32.4% over 12 months, on a forward P/E near 11. Tenable was reportedly explored by Permira in 2024. Vulnerability management is increasingly bundled into broader platforms, making Tenable a natural tuck-in for Palo Alto, or a fresh take-private for Thoma Bravo or Permira. However, a $338 million buyback authorization and Gartner Leader status could push the board to hold out for a steep premium.

3. Rapid7

Rapid7 (NASDAQ: RPD) is the most distressed name on this list. Shares trade at $6.37, down 74.7% over one year and 91.9% over five, with market cap collapsing to $426 million. Q1 FY2026 revenue of $209.69 million declined 0.27% year over year, ARR fell 0.6% to $832 million, and FY26 guidance implies a 2% to 3% revenue contraction. And $597.6 million of convertible senior notes are classified as current liabilities.

That combination of cheap valuation, balance-sheet pressure, and decent SIEM/XDR assets makes Rapid7 the highest-probability private-equity buyout, carve-up, or strategic tuck-in. Jana Partners has previously pushed for a sale. The risk here is that the convertible note overhang complicates clean LBO math, and the analyst consensus target is $7.25, with 21 Holds signaling muted Wall Street conviction.

4. Varonis Systems

Varonis Systems (NASDAQ: VRNS) owns the data-security and data security posture management niche, the hottest M&A subsector behind Rubrik and Cyera comps. SaaS ARR jumped 69% year over year to $683.2 million, and SaaS revenue rose 82% to $161.06 million. Total Q1 FY2026 revenue grew 26.9% year over year, with management raising FY26 revenue guidance to $731 million to $737 million.

Despite the operational momentum, shares trade at $28.00, down 38.2% over 12 months. AI workloads are turning data security into a board-level priority, making Varonis a natural fit for Microsoft (already a Purview integration partner), Palo Alto, or CrowdStrike. Yet a forward P/E near 167× reflects an expensive SaaS transition that any strategic acquirer would need to underwrite, alongside active securities litigation tied to prior forward guidance.

5. Qualys

Qualys (NASDAQ: QLYS) is the prototypical private equity take-private candidate: cash-flow rich, decelerating, and clean. FY2025 produced $669.1 million in revenue, $198.3 million of net income, and $304.4 million of free cash flow (+31%). Q1 FY2026 GAAP operating margin reached 35%, and the company holds a 29.4% profit margin and 37.7% return on equity.

Growth is the catch. Calculated current billings growth decelerated from 13% to 6% in Q4 2025, and shares trade at $91.53, down 30.82% over one year. A forward P/E near 13 fits cleanly with a Thoma Bravo-style take-private. Founder-CEO Sumedh Thakar has shown no public appetite for a sale, and any deal involving Qualys could face antitrust scrutiny over vulnerability-management overlap if paired with Tenable.

Conclusion

Five themes tie this list together:

- Depressed valuations against operational fundamentals

- Platform pressure from Palo Alto Networks, CrowdStrike, Zscaler

- Hyperscaler appetite for data and identity layers

- PE dry powder targeting sub-$6 billion software

- AI redrawing the build-versus-buy line

Anthropic’s Claude Code Security tool in February 2026 underscored that point-solution moats are eroding. Antitrust scrutiny, premium expectations, and financing conditions remain the key swing variables. While no deal is a sure thing, each of these targets offers a compelling strategic blueprint for a takeover.

Contact [email protected] for any questions or corrections.