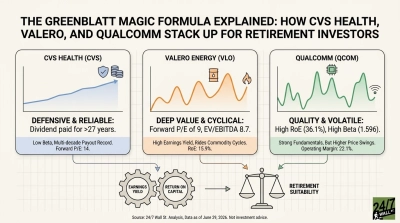

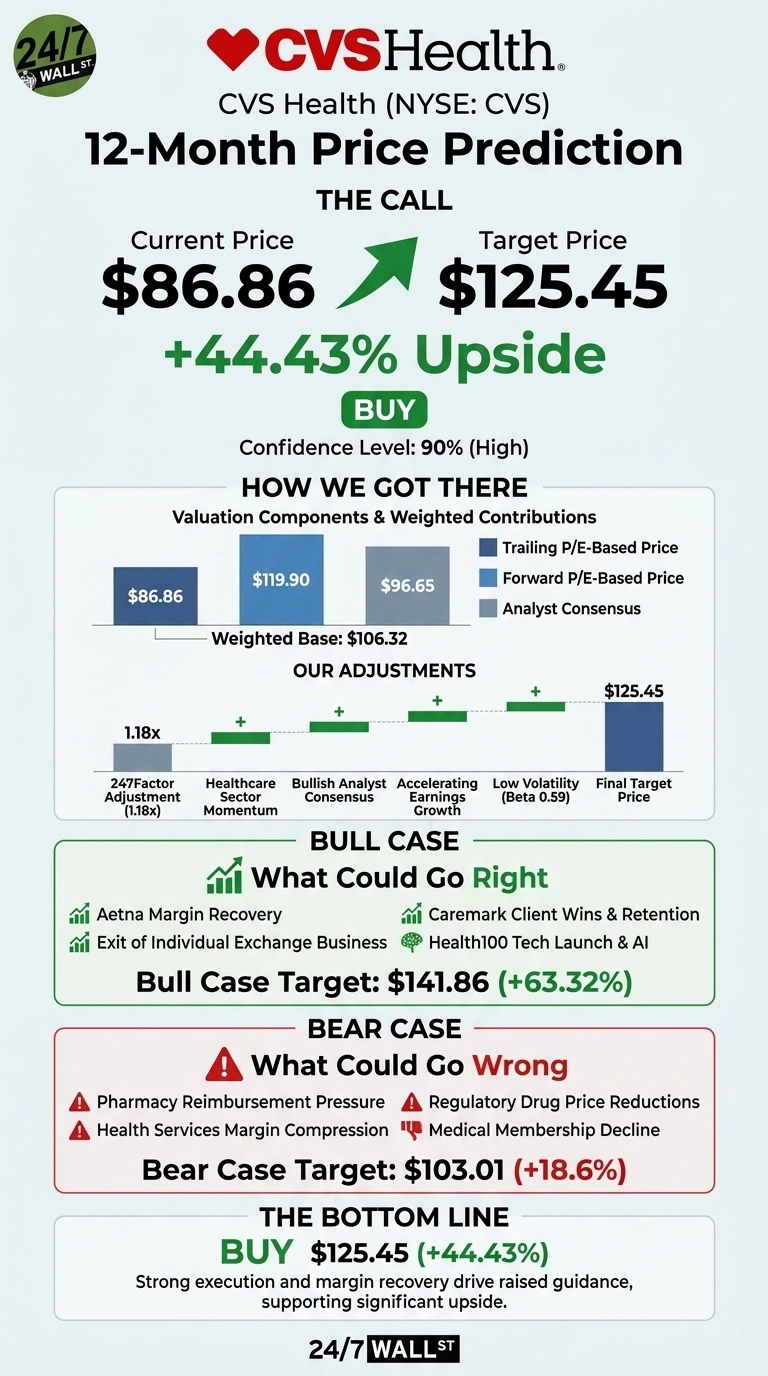

Our 24/7 Wall St. price target for CVS Health (NYSE:CVS | CVS Price Prediction) is $125.45, pointing to meaningful upside from where shares trade today. The stock closed at $86.86 on May 6, after a 7.65% single-day pop on Q1 earnings. Our model implies 44.43% upside over the next 12 months, and we are issuing a buy rating with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $86.86 |

| 24/7 Wall St. Price Target | $125.45 |

| Upside | 44.43% |

| Recommendation | BUY |

| Confidence Level | 90% |

Aetna’s Margin Snapback Just Reset the CVS Story

CVS has been one of the strongest large-cap healthcare names of the past year, gaining 35.88% over the last 12 months and 19.53% in just the past month. Shares now sit near the 52-week high of $88.63 after rebounding sharply from the $56.29 low.

The catalyst was a clean Q1 2026 earnings report on May 6. CVS posted adjusted EPS of $2.57 against a $2.21 consensus, the fourth straight beat. Revenue rose 6.2% to $100.4 billion. The headline was Aetna: Health Care Benefits adjusted operating income jumped 52.6% to $3.04 billion, with the medical benefit ratio improving to 84.6% from 87.3%. Management raised full-year adjusted EPS guidance to $7.30 to $7.50 and operating cash flow to at least $9.5 billion.

The Bull Case

The bull case is straightforward. If Aetna’s MBR continues compressing and the individual exchange exit removes a money-losing drag, FY2026 EPS could land near the high end or above the $7.50 guide. Caremark is winning clients with high-90s retention, and the Health100 launch on Google Cloud opens a new tech-enabled engagement layer.

Morningstar’s Julie Utterback raised her fair value to $105 from $97 after the earnings report. The Street consensus sits at $96.65 with 24 buys, 3 holds, and zero sells. BofA raised the firm’s price target on CVS Health to $100 from $95 and keeps a Buy rating on the shares after the company reported a Q1 beat with revenue, EBIT, and EPS above consensus expectations. Further, UBS raised the firm’s price target to $100 from $97 and keeps a Buy rating on the shares.

Our bull case scenario points to $141.86, a 63.32% total return.

What Could Go Wrong

Risks are real. Pharmacy reimbursement pressure is compressing PCW margins, with that segment growing just 0.2% YoY. Health Services margins face client price improvements, and regulatory drug price cuts loom. FY2025 included a $5.7 billion goodwill impairment plus $1.22 billion in legacy litigation charges, dragging GAAP EPS to $6.75.

That said, those were largely non-cash and non-recurring items tied to the Health Care Delivery rationalization, and bulls would note CVS is investing through the cycle. Our bear case still lands at $103.01, suggesting downside looks limited.

I’d Buy It Here

The 24/7 Wall St. price target of $125.45 reflects a buy at 90% confidence. The key factor tipping the scale is Aetna’s margin recovery executing ahead of plan, which gives the raised guidance real credibility. I’d be a buyer here if you believe the MBR can hold below 86% through year-end. I’d stay on the sidelines if pharmacy reimbursement pressure starts bleeding into Caremark’s renewals. CEO David Joyner framed it well: “Our positive performance is driven by strong execution across our enterprise.”

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $125.45 |

| 2030 | $240.46 |

These projections assume CVS continues executing on Aetna margin recovery and Caremark retention. Significant upside or downside could result from a Medicare Advantage rate shock or PBM regulatory action.

Contact [email protected] for any questions or corrections.