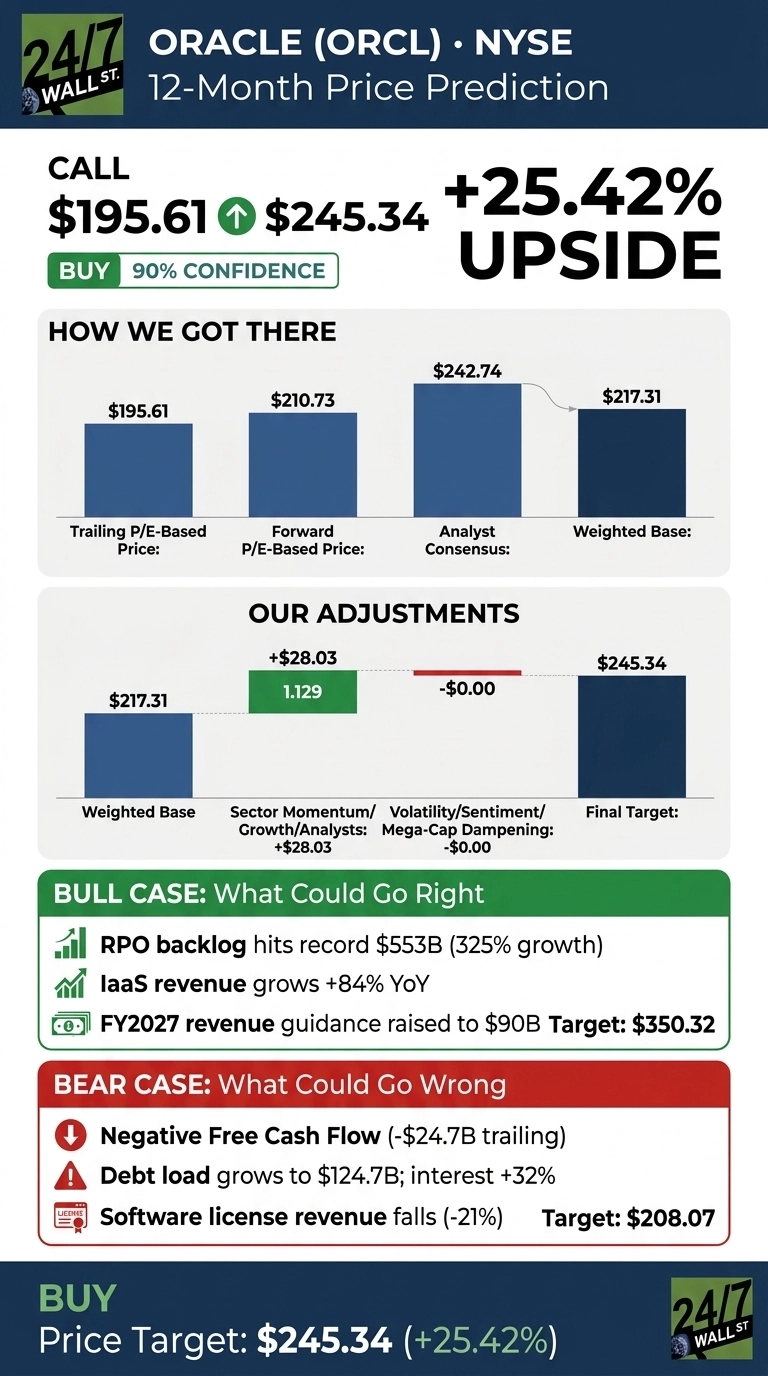

Our 24/7 Wall St. price target for Oracle (NYSE:ORCL | ORCL Price Prediction) is $245.34 over the next 12 months, implying 25.42% upside from $195.61. The recommendation is buy, with a 90% confidence level driven by a record contracted backlog and accelerating cloud infrastructure economics. This is one of the highest-conviction setups in mega-cap software right now.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $195.61 |

| 24/7 Wall St. Price Target | $245.34 |

| Upside | 25.42% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Volatile Year Reset by a Blockbuster Q3

Oracle shares are up 20.01% over the past month and 21.24% over the past year, but the ride has been wild. The stock peaked near $343.01 in late 2025 before bottoming around $134.57 in February as investors questioned the capex bill. Today, Oracle sits 29% below its 52-week high.

The Q3 FY2026 report on March 10, 2026 changed the narrative. Revenue hit $17.19 billion with EPS of $1.79, the first quarter in over 15 years with organic revenue and non-GAAP EPS both growing 20%+. IaaS revenue jumped 84% to $4.89 billion, and Remaining Performance Obligations exploded 325% to $553 billion. Management raised FY2027 revenue guidance to $90 billion.

Why Bulls See a Breakout Ahead

The bull case rests on contracted revenue. RPO has marched from $138 billion at the end of FY2025 to $553 billion three quarters later. Safra Catz’s roadmap calls for OCI revenue of $18 billion this year, scaling to $32 billion, $73 billion, $114 billion, and $144 billion across the next four years. Co-CEO Clay Magouyrk noted “Multi-cloud database revenue grew 531% year over year. AI infrastructure revenue grew 243% year over year” in Q3.

Wall Street has 7 Strong Buy and 28 Buy ratings versus just one Sell, with a consensus target of $242.74. Our bull case scenario points to $350.32 by May 2027, a 79.09% return if AI capacity utilization keeps gross margins above 30% and the OCI ramp tracks guidance.

The Risks Worth Watching

The bear case starts with the balance sheet. Non-current debt sits at $124.7 billion, up from $85.3 billion at fiscal year-end, with interest expense climbing 32%. Free cash flow is -$24.74 billion trailing as capex runs at $50 billion. Software license revenue also fell 21% in Q2, and a small group of mega AI contracts concentrates risk.

Bulls would counter that capex is the moat. CFO Doug Caring highlighted “the uncoupling of CapEx with capital requirements from Oracle Corporation” via customer prepayments and partner-funded capacity. Our bear case scenario still produces $208.07 a year out, a 6.37% positive return.

Where Oracle Stands Today

The 24/7 Wall St. price target of $245 reflects a stock that has already absorbed the worst of the capex panic and now trades at a forward P/E of 24 on accelerating growth.

The bull thesis strengthens if RPO continues converting into reported cloud revenue at current rates. The thesis weakens if the FY2027 $90 billion revenue target slips or interest expense outruns operating income growth. The model’s output carries 90% confidence.

Looking further out, here is where our model projects Oracle could trade, assuming the OCI ramp and current margin trajectory hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $245 |

| 2027 | $285 |

| 2028 | $320 |

| 2029 | $350 |

| 2030 | $380 |

These projections assume Oracle continues executing on its multicloud and AI infrastructure strategy. Significant upside or downside could come from the pace of GPU supply, customer concentration shifts, or a slowdown in AI training demand.

Contact [email protected] for any questions or corrections.