Automation and supply chain software has quietly become one of the most resilient corners of the market, and a recent pullback has dragged several high-growth names back into reach for retail investors. Stocks trading under $30 in this space are worth a fresh look right now because the operational story (rising annual recurring revenue, expanding margins, AI-driven product cycles) is moving faster than the share prices suggest. When growth keeps compounding but the stock keeps drifting, the entry math gets interesting.

With that in mind, here are two automation and supply chain stocks trading under $30 that analysts believe still have meaningful upside from current levels.

Samsara (NYSE: IOT)

Samsara (NYSE:IOT | IOT Price Prediction) runs a connected operations platform that puts fleet telematics, equipment monitoring, and AI safety tools into the hands of the world’s largest physical operators.

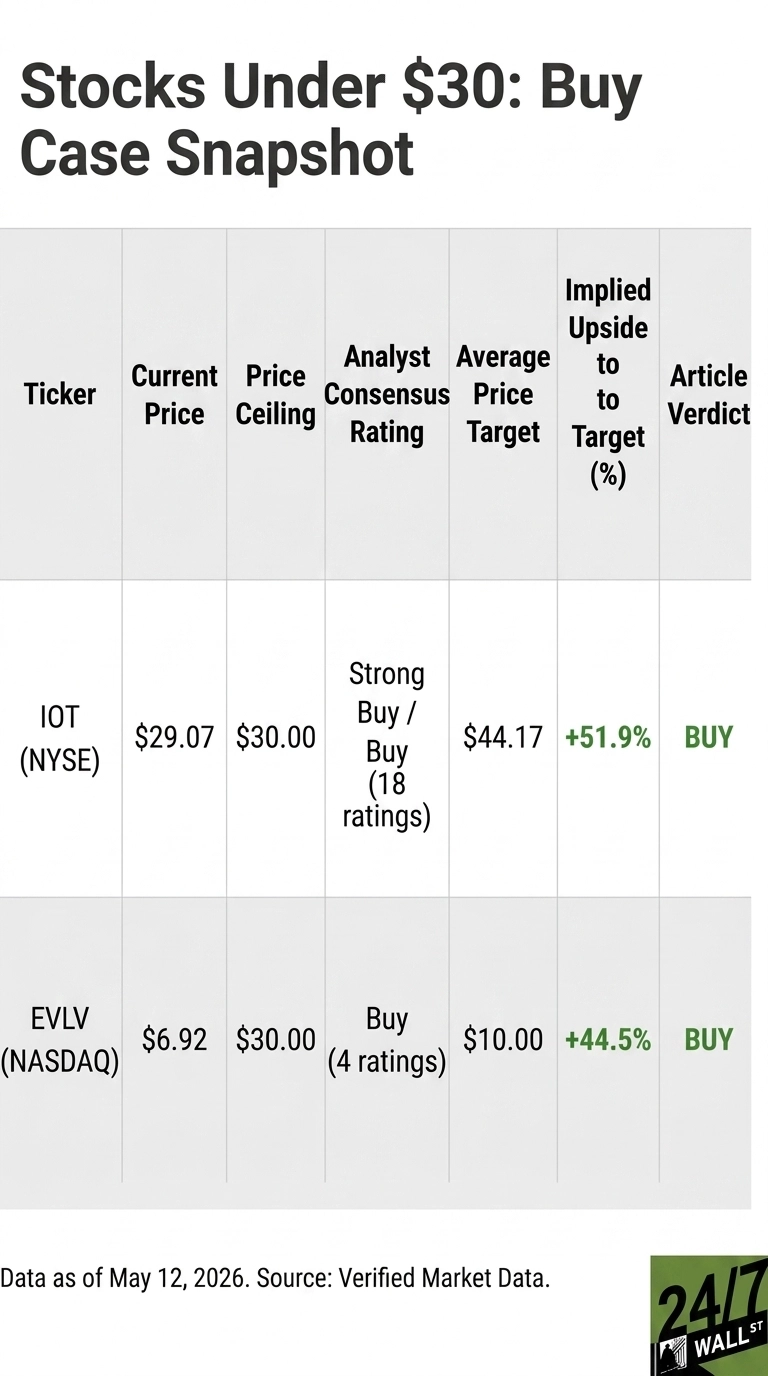

Shares recently changed hands at $29.07, well inside the $30 ceiling and down 32.86% over the past year even as the business has accelerated. For a retail investor, that gap between fundamentals and price is the entire pitch.

The Q3 FY2026 report did a lot of heavy lifting. Revenue grew 29.2% year over year to $415.98 million, non-GAAP EPS came in at $0.15 against a $0.1187 consensus, and Samsara delivered its first quarter of GAAP profitability. ARR hit $1.75 billion, up 29%, and Wall Street’s average target sits at $44.17 with 15 Buy and 3 Strong Buy ratings.

The bull case is straightforward: durable 29% growth, an 800 basis point jump in non-GAAP operating margin to 19%, and enterprise traction that CEO Sanjit Biswas summed up by noting that “our $100K+ ARR customers now represent over $1 billion in ARR, growing 36% year-over-year.”

The risk worth respecting is valuation. Forward earnings still print around 44x and the price-to-sales ratio sits at 10.67, leaving little room if enterprise sales cycles stretch or industrial demand softens on tariffs. Even so, the combination of accelerating profitability and a one-year drawdown makes IOT one of the more compelling growth-at-a-reset stories under $30.

Evolv Technologies (NASDAQ: EVLV)

Evolv Technologies (NASDAQ:EVLV) sells AI-powered weapons-detection screening on a subscription model, with Evolv Express deployed across schools, stadiums, hospitals, and workplaces.

The stock trades at $6.92, up 55.86% over the past year and giving smaller accounts genuine optionality on a niche AI security theme without a massive dollar commitment.

Fundamentally, FY2025 revenue came in at $145.9 million, up 40.5%, and operating cash flow swung to a positive $18.67 million. Management raised FY2026 revenue guidance to $172 million to $178 million and guided to positive full-year adjusted EBITDA. Analyst coverage is thin but uniformly constructive, with 4 Buy ratings and an average price target in the range of $9.13 to $10.00 depending on the source.

The bull case rests on the recurring revenue flywheel. ARR climbed to $120.5 million, up 21%, and roughly half of 2026 deployments are expected under a pure-subscription model. CEO John Kedzierski struck a confident tone, saying “AI-based weapons screening will continue to become increasingly prevalent.”

The risk side is real and should not be glossed over. Q4 missed both top and bottom lines (revenue of $38.50 million against a $43.71 million estimate), gross margin compressed to 48.4% from 57.5%, and Evolv disclosed a material weakness in internal controls. For risk-tolerant investors comfortable with execution warts, the raised guidance and subscription mix still make this a credible small-cap automation play.

The Bottom Line

A share price under $30 is a starting filter, never a thesis. IOT offers a cleaner compounding story with valuation risk, while EVLV pairs faster top-line growth with governance and execution issues that demand careful diligence. Do your own research, size positions thoughtfully, and weigh how much volatility you are actually willing to absorb before acting on any name in this group.

Contact [email protected] for any questions or corrections.