Shopify (NASDAQ: SHOP | SHOP Price Prediction) and Amazon (NASDAQ: AMZN) just reported earnings that frame two opposite philosophies in commerce. Shopify arms independent merchants with payments, software, and AI tools.

Amazon owns the marketplace, the warehouses, the ad network, and increasingly, the chips powering generative AI. Both quarters were strong. The question is which model converts that strength into durable returns.

Merchant Engine Roars While AWS Hits a New Gear

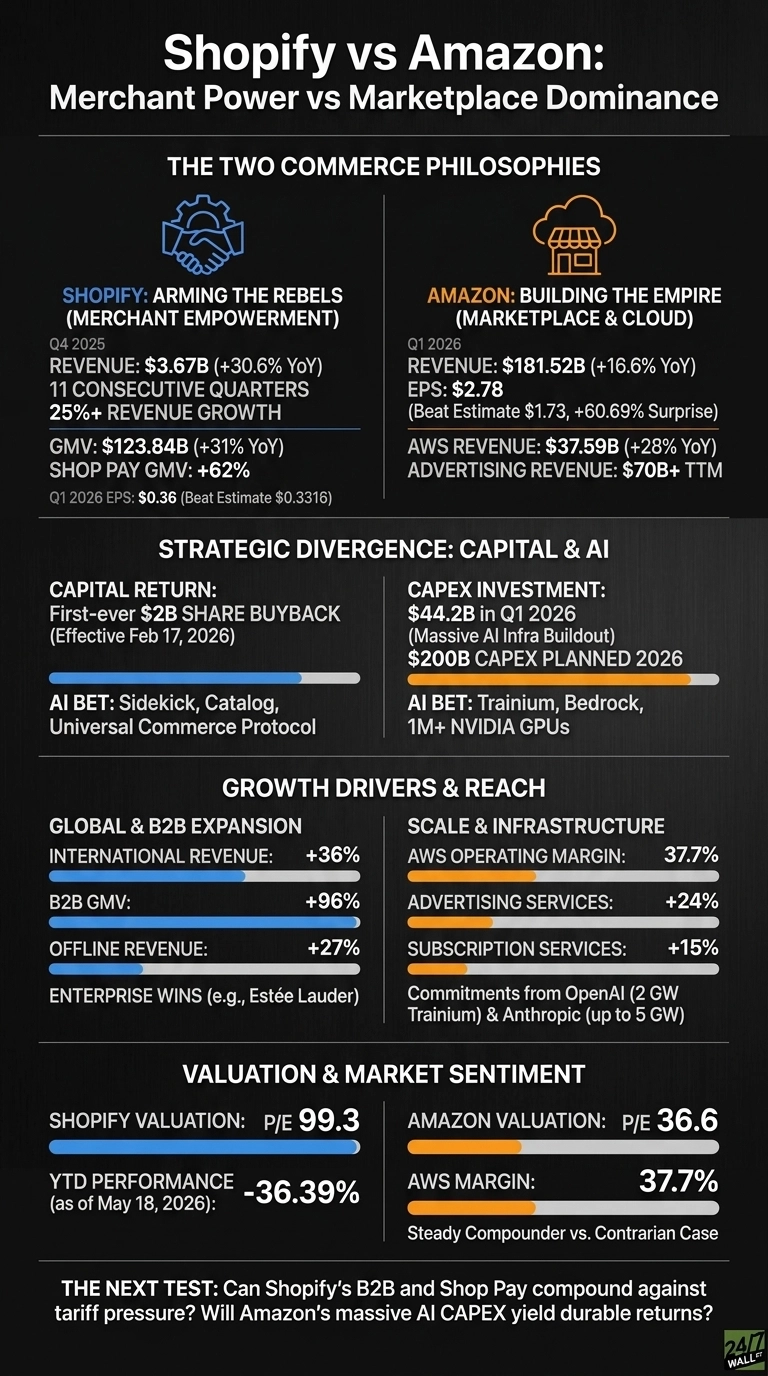

Shopify’s Q4 2025 earnings report showed revenue of $3.67 billion, up 30.6% YoY, marking 11 straight quarters of 25%+ growth. GMV hit $123.84 billion, and Shop Pay GMV jumped 62%. B2B GMV nearly doubled at +96%, a quiet but important signal that wholesale brands are routing through Shopify rather than building their own stack. Q1 2026 then beat with EPS of $0.36 against a $0.3316 estimate.

Amazon’s Q1 2026 told a different story. Revenue reached $181.52 billion, +16.6% YoY, and EPS came in at $2.78 versus $1.73 expected, a 60.69% surprise. AWS grew 28%, its fastest pace in 15 quarters, and advertising crossed $70 billion TTM. CEO Andy Jassy framed the moment plainly: “We’re in the middle of some of the biggest inflections of our lifetime.”

| Business Driver | Shopify | Amazon |

| Main growth engine | Merchant Solutions +35% | AWS +28% |

| Capital posture | First-ever $2B buyback | $200B capex planned 2026 |

| AI bet | Sidekick, Catalog, Commerce Protocol | Trainium, Bedrock, 1M+ NVIDIA GPUs |

Arming the Rebels vs Building the Empire

Shopify is doubling down on enabling other people’s brands. International revenue rose 36%, offline grew 27%, and enterprise wins like Estée Lauder show the platform reaching upmarket. Free cash flow of $715 million at a 19% margin gave management room to authorize that maiden buyback.

Amazon, by contrast, is spending like a hyperscaler at war. CapEx ran $44.2 billion in a single quarter, and trailing free cash flow dropped to $1.2 billion. The payoff is visible in commitments from OpenAI for roughly 2 GW of Trainium capacity and Anthropic for up to 5 GW. The risk: if AI demand wobbles, those returns get tested fast.

The Next Test Is Whether Capex and Consumers Cooperate

Shopify guided Q1 2026 revenue growth in the low thirties with FCF margin in the low-to-mid teens. I will be watching whether B2B and Shop Pay can keep compounding while tariff pressure on small merchants intensifies. The stock is already down 36.39% year to date, suggesting investors are nervous about that exact setup.

Amazon guided Q2 2026 sales of $194B to $199B. You should keep an eye on AWS margins, currently a remarkable 37.7%, and whether ad services continue absorbing retail softness.

Why Amazon Screens Steadier, While Shopify Sets Up a Contrarian Case

Amazon screens as the steadier compounder on current numbers. The 31x trailing P/E feels reasonable for a business compounding AWS, ads, and chips together.

Shopify trades at a 98x multiple, which leaves no room for a consumer stumble. For turnaround-oriented analysis, that 36% YTD drawdown in SHOP is the kind of setup contrarians often study. Another quarter of clean merchant growth would meaningfully strengthen the thesis.

Contact [email protected] for any questions or corrections.