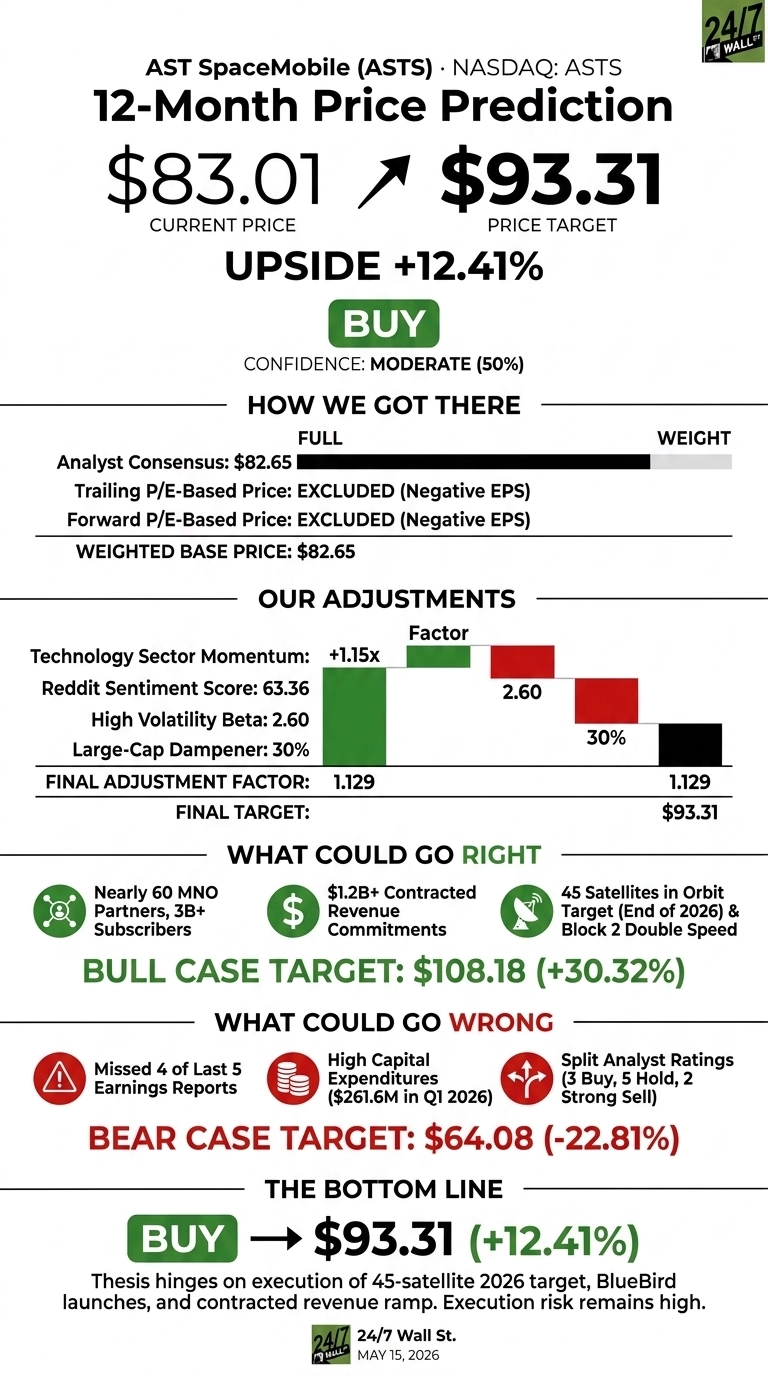

AST SpaceMobile (NASDAQ:ASTS) has whipsawed investors with a 27.02% one-week rally, even after a brutal Q1 double miss. Our 24/7 Wall St. price target for AST SpaceMobile is $93.31, pointing to 12.41% upside from the current $83.01 share price. We rate the stock a buy with moderate confidence, and the bull-case path to triple digits is genuinely in play.

| Metric | Value |

|---|---|

| Current Price | $83.01 |

| 24/7 Wall St. Price Target | $93.31 |

| Upside | 12.41% |

| Recommendation | BUY |

| Confidence Level | 50% (moderate) |

A Volatile Quarter With a Sharp Recovery

ASTS has been one of the market’s wildest rides. The stock is up 216.23% over the past year and 14.29% year to date, yet still sits 36% below its 52-week high of $129.89.

Q1 2026 revenue of $14.74 million missed the $36.58 million consensus by 59.72%, and EPS came in at -$0.66, a 223.21% miss driven by an $88.65 million induced conversion expense and $55.35 million in stock-based compensation.

Shares dropped 11.62% on the report. Reddit sentiment cratered to 11 (very bearish) midday, then recovered to 73 (bullish) within hours as investors refocused on management’s reaffirmed $150 million to $200 million full-year guidance and the mid-June BlueBird 8, 9, and 10 launch.

The Case for $108+

The bull case rests on execution. AST has nearly 60 MNO partners covering over 3 billion subscribers, over $1.2 billion in contracted commitments, and a $175 million prepayment from stc Group. Management is guiding to approximately 45 BlueBird satellites in orbit by year-end 2026, with 2027 revenue approaching $1 billion, according to CEO Abel Avellan’s call commentary.

Block 2 BlueBirds are expected to nearly double the 98.9 Mbps peak speeds of Block 1, and AST holds approximately 3,900 patent and patent pending claims.

Avellan framed the opportunity directly: “AST SpaceMobile is accelerating manufacturing, regulatory progress, commercial partnerships, and government programs, furthering our position as the only technology positioned to capture the massive direct to device broadband opportunity in full.” Our model’s bull case projects ASTS at $108.18 over 12 months, a 30.32% total return.

What Could Go Wrong

The bear case is real. ASTS has missed 4 of 5 earnings reports, average one-week post-earnings reaction is -9.88%, and CapEx hit $261.6 million in Q1 alone. Wall Street is split: 3 Buy, 5 Hold, 2 Strong Sell. Our bear scenario sees the stock falling to $64.08, a 22.81% drawdown.

Bulls would counter that the ballooning stock-based comp and induced conversion charges are non-cash and reflect aggressive hiring to scale manufacturing. The balance sheet remains a fortress at $3.03 billion in cash with shareholders’ equity up 367.96% year over year.

AST SpaceMobile Price Prediction 2026-2030

Our 24/7 Wall St. price target of $93.31 reflects a buy rating with moderate confidence. The decisive factor is the BlueBird launch cadence: contracted revenue is real, the spectrum portfolio is unmatched, and the path from 45 satellites to commercial service is now visible.

The setup looks constructive if BlueBird 8-10 launch successfully in June and management hits the lower bound of guidance. The thesis weakens if Q2 revenue slips below $25 million or another major capital raise materializes.

Looking further ahead, here is where our model projects ASTS could trade as the constellation scales and commercial service ramps.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $93.31 |

| 2027 | $102.50 |

| 2028 | $110.75 |

| 2029 | $117.80 |

| 2030 | $124.20 |

These projections assume AST executes on its 45-satellite 2026 target and approaches the $1 billion 2027 revenue mark. Significant upside could materialize from Golden Dome defense awards, while regulatory delays or further dilutive capital raises would skew outcomes toward the $60.88 bear case.

Contact [email protected] for any questions or corrections.