For most of President Donald Trump’s second term, the White House viewed the Federal Reserve as the economy’s biggest obstacle rather than its biggest ally. Trump repeatedly blasted former Fed chair Jerome Powell for keeping interest rates too high for too long, arguing elevated borrowing costs were choking off housing, business investment, and consumer spending. At various points, Trump even floated the idea of firing Powell outright — an extraordinary public pressure campaign against a central bank designed to operate independently.

That made Trump’s choice of Kevin Warsh look straightforward at first glance: install a chair more willing to cut rates and help juice economic growth heading into the 2026 midterms. But inflation has a nasty habit of rewriting political scripts. And now, surprisingly, Warsh may soon face pressure to do the exact opposite of what Trump wanted.

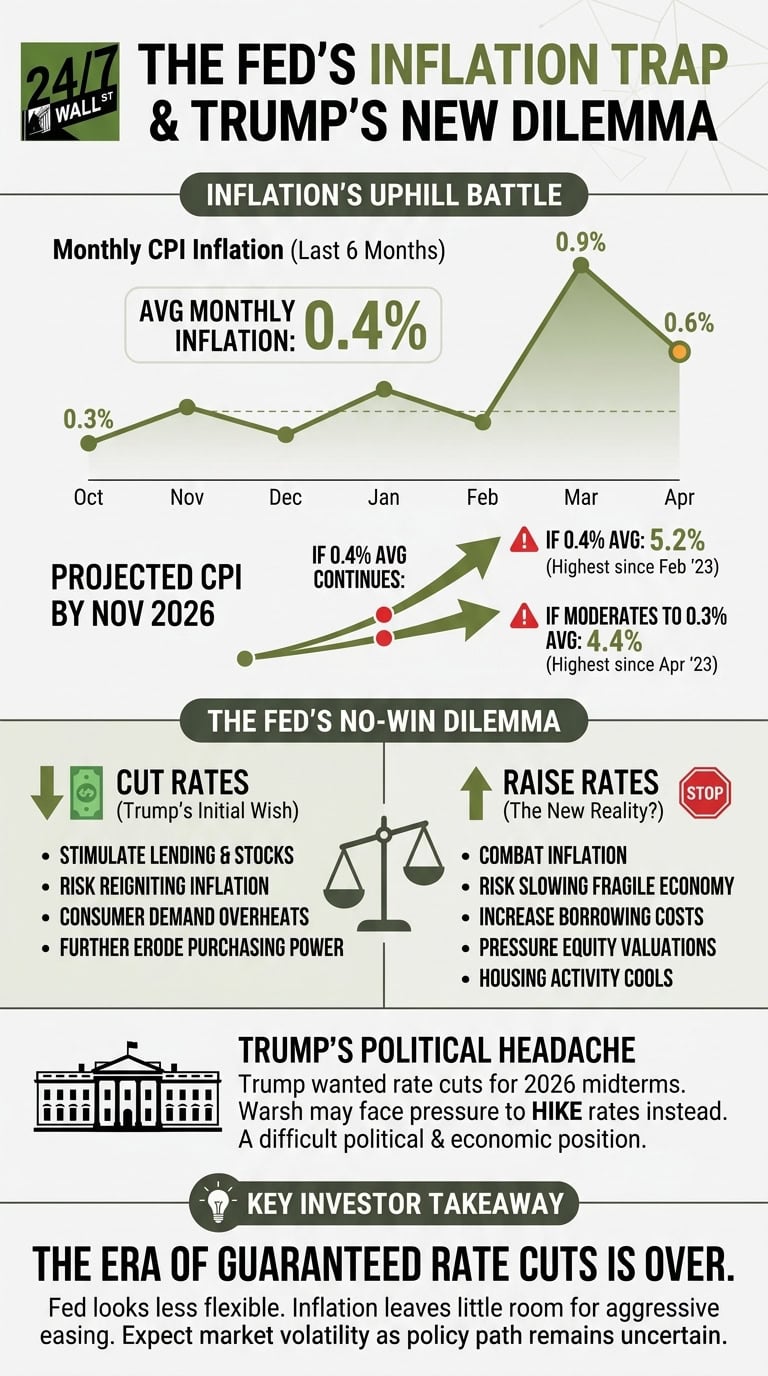

Inflation Is Moving in the Wrong Direction

The latest inflation trend is difficult to ignore. According to the Bureau of Labor Statistics’ Consumer Price Index data, CPI inflation has averaged 0.4% month over month during the last six months. More concerning are the recent spikes — March CPI rose 0.9%, followed by another 0.6% increase in April.

According to data from BoA Global Research and Bloomberg, if inflation continues following this trend of averaging a 0.4% monthly rise, the CPI could hit 5.2% by the November elections. Even if it moderates to 0.3%, it would land at 4.4%, its highest level since April 2023. The hotter path would send inflation above 5% for the first time since February 2023 — more than double February 2026’s inflation reading.

That matters because inflation compounds quietly before consumers fully notice it. Grocery bills creep higher. Credit card balances become harder to pay down. Auto loans and rents consume a bigger share of paychecks. Regardless of how you look at it, persistent inflation acts like a tax increase on households.

And the Fed’s core mandate remains price stability.

Inflation is back, and it’s putting the Fed in a corner that could crush the White House’s economic plans. The era of easy money is over—and the timing couldn’t be worse for the midterms.

Inflation is back, and it’s putting the Fed in a corner that could crush the White House’s economic plans. The era of easy money is over—and the timing couldn’t be worse for the midterms.

The Fed’s Dilemma Just Became Trump’s Problem

Trump’s criticism of Powell centered almost entirely on rates being too restrictive. Cutting rates was supposed to stimulate lending, lower mortgage costs, and support stock prices. Investors initially expected Warsh to deliver one or perhaps two rate cuts in 2026 after taking over the Fed chairmanship.

Instead, markets are now beginning to debate whether the next Fed move could actually be a rate hike.

That is a difficult political and economic position for Warsh. If he cuts rates while inflation is accelerating, borrowing may increase further, consumer demand could stay overheated, and prices might rise even faster. Purchasing power has already been strained after several years of elevated inflation, and another leg higher would further erode household budgets.

That said, raising rates carries its own risks. Higher interest rates would increase borrowing costs for businesses and consumers just as economic growth is already showing signs of fatigue. Housing activity remains sensitive to mortgage rates — and they just rose to their highest levels since last August — while credit card APRs above 20% continue squeezing consumers.

Let’s also remember the stock market backdrop. Much of the rally since Trump’s inauguration has depended on expectations of easier monetary policy and continued artificial intelligence-driven spending. If Warsh raises rates instead, equity valuations could face pressure almost immediately.

Key Takeaway

In short, Kevin Warsh inherited a Federal Reserve that looks far less flexible than many investors — and perhaps Trump himself — expected just a few months ago. Inflation running at a sustained 0.4% monthly pace leaves little room for aggressive easing. Even a moderation to 0.3% monthly inflation would still place CPI near 4.4% by November.

Granted, inflation forecasts can change quickly if consumer demand weakens or energy prices retreat. But Warsh now faces a no-win balancing act: keep rates steady or cut them and risk reigniting inflation, or raise rates and potentially slow an already fragile economy ahead of critical midterm elections.

For investors, the message is clear — the era of assuming rate cuts are guaranteed is already over.

Contact [email protected] for any questions or corrections.