SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) stock spent much of late 2025 looking like a fintech comeback story before giving back gains in 2026. Doubling from current levels would require a move to roughly $36.44, well above the 52-week high of $32.73. Our model says that is a stretch in the next 12 months, even with the bull case fully intact.

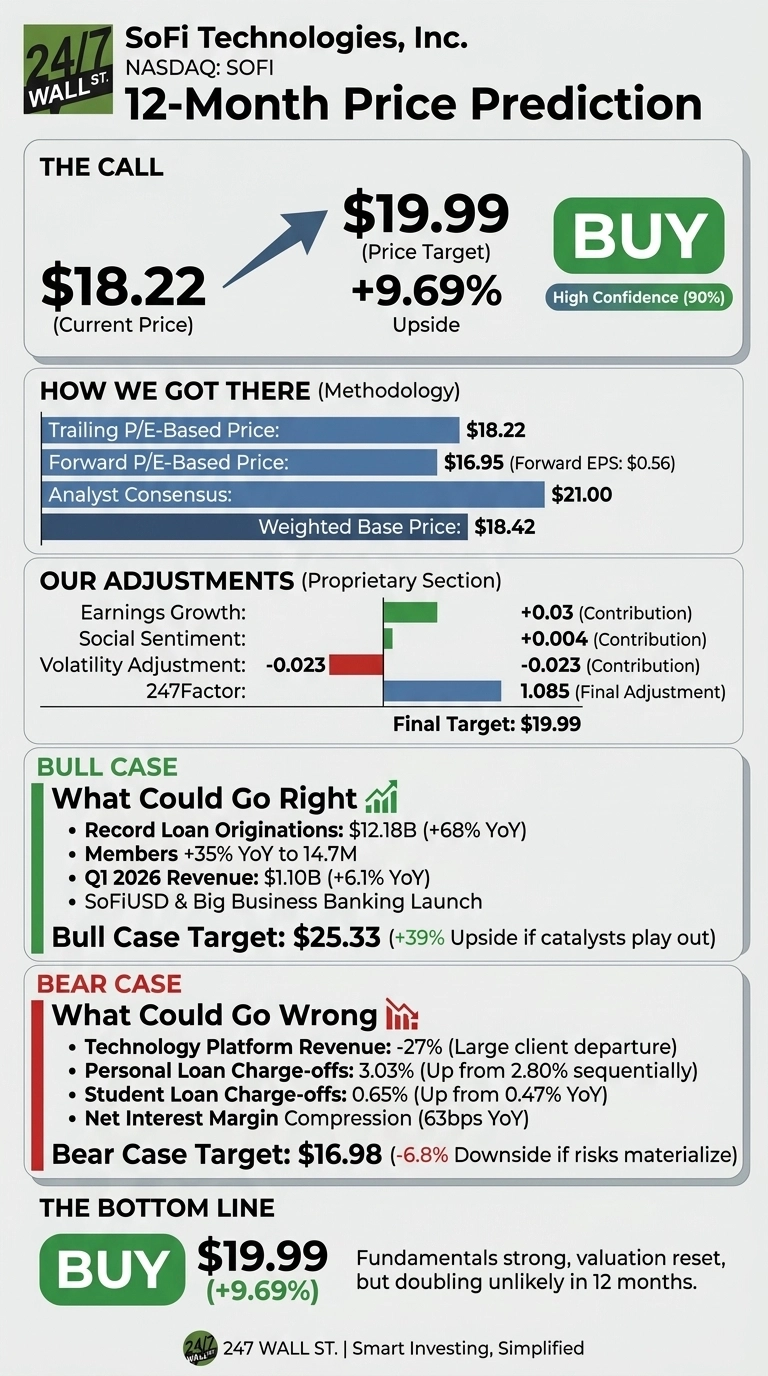

The stock currently trades at $18.22. Our 24/7 Wall St. price target is $19.99, implying 9.69% upside over the next 12 months. The recommendation is buy, with confidence level 90%, which qualifies as high conviction.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $18.22 |

| 24/7 Wall St. Price Target | $19.99 |

| Upside | 9.69% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Sharp Pullback From Last Fall’s Highs

SoFi shares are down 30.4% year to date after starting 2026 near $26.18. The stock has rebounded recently, up 17.36% over the past month and 38.34% over the past year, but still sits roughly 36% below its 52-week high.

Fundamentals have not cooperated with the bears. Q1 2026 revenue came in at $1.10 billion, beating consensus by roughly 5%, with EPS of $0.12 in line with estimates. Net income jumped 134.45% year over year to $166.7 million, members grew 35% to 14.7 million, and loan originations hit a record $12.18 billion. The market shrugged. That disconnect is the entire setup.

The Case for $25 and Beyond

Our bull case for SoFi over the next 12 months is $25.33, a 39% gain. CEO Anthony Noto cited an “18th consecutive quarter of the Rule of 40 with a score of 72%“, with Q1 adjusted net revenue up 41% year over year. Management’s 2026 guide calls for $4.655 billion in adjusted net revenue and $0.60 in adjusted EPS, with medium-term adjusted EPS CAGR of 38% to 42% through 2028.

SoFiUSD, the first stablecoin from a nationally chartered bank, the Mastercard settlement partnership, the new Big Business Banking unit, and the relaunched SoFi Plus subscription each open distinct revenue streams. Loan Platform Business commitments grew by $3.6 billion with three new partners.

Strong-buy and buy analysts together count eight ratings against four sells. A full doubling to $36 would require multiple expansion plus blowout 2027 EPS.

What Could Go Wrong

Our bear case is $16.98, roughly 6.8% downside. Net interest margin compressed 63 basis points on asset yields year over year, the Technology Platform segment shrank 27% after a large client departure, and personal loan charge-offs ticked up to 3.03% from 2.80% sequentially. The forward P/E of 30 and trailing P/E of 40 leave little margin for error.

CFO Chris Lapointe said the all-in charge-off rate excluding delinquent sales was “4.4%, which was the same as last quarter and down roughly 40 basis points from the first quarter of 2025”.

The Technology Platform decline reflects a single client. The NIM remains “above 5% for the foreseeable future”. Retail sentiment has wobbled, with the most recent Reddit data showing a bearish shift on May 29-30.

Bullish Setup, But Don’t Expect a Double

The 24/7 Wall St. price target of $19.99 with a buy rating and 90% confidence reflects a clear view: SoFi’s fundamentals are stronger than the price action suggests, but a true doubling to $36 inside a year is not the base case. The growth story is intact, valuation has reset, and insider activity is net buying across 48 recent transactions.

Investors seeking exposure to the digital bank story get a sharply discounted entry relative to last fall. Those who want NIM stability and a clean Technology Platform earnings report before adding risk. The easy money was made in 2025, but the longer arc still favors patient holders.

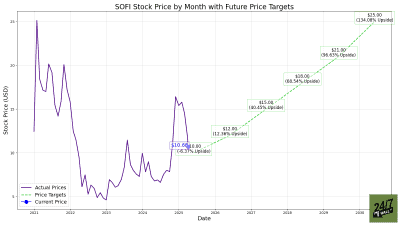

SoFi Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $19.99 |

| 2027 | $22.50 |

| 2028 | $24.10 |

| 2029 | $25.00 |

| 2030 | $25.75 |

These projections assume SoFi continues executing on its 30% revenue CAGR and 38% to 42% EPS CAGR targets. Significant upside could come from stablecoin adoption and Technology Platform reacceleration. Significant downside could come from a credit cycle turn or sustained NIM compression.

Contact [email protected] for any questions or corrections.