With megacap AI software names trading at triple-digit cash-flow multiples, value-oriented investors are quietly rotating into the physical layer of the buildout: power, land, and data center capacity. The U.S. is projected to need at least 50 gigawatts of electric capacity for AI by 2028, and that bottleneck is where unsexy infrastructure plays under $30 a share are starting to look mispriced compared to the software stocks they ultimately power.

With that in mind, here is one stock trading under $30 that has already locked in roughly a decade of hyperscaler cash flow, yet still sits well below Wall Street’s consensus target.

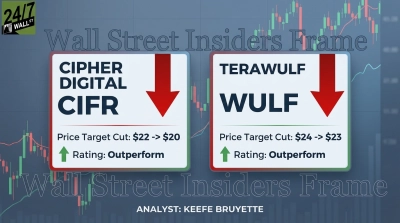

Cipher Mining (NASDAQ: CIFR)

Cipher Mining (NASDAQ:CIFR), recently rebranded as Cipher Digital, develops industrial-scale data centers and is pivoting from bitcoin mining into high-performance computing infrastructure leased to hyperscalers.

Shares still trade below $20 now, up 31.98% year-to-date and a staggering 415.34% over the past year. For a retail investor, that price keeps Cipher comfortably under the $30 ceiling while leaving room to the $30.53 average analyst target and the $40.50 high target from Morgan Stanley.

Fundamentals reflect a company mid-transformation. Market cap sits near $7.97 billion on 409 million shares outstanding, with a debt-to-equity of 3.44 and a negative trailing P/E of -10. Analyst coverage skews bullish: 5 Strong Buy and 9 Buy ratings, with zero Holds or Sells. Jefferies upgraded the stock to Strong-Buy on May 15, and HC Wainwright reiterated a Buy with a $30 target.

The bull case rests on contracted cash flows. Cipher has signed approximately $9.3 billion in contracted HPC revenue across 600 megawatts via two landmark leases: a 15-year, 300 MW lease with Amazon Web Services at Black Pearl generating roughly $5.5 billion at a ~100% NOI margin, and a 10-year, 300 MW lease with Fluidstack and Google at Barber Lake worth ~$3.8 billion at a ~86% NOI margin. Both projects target October 2026 energization, after which management expects approximately $669 million in average annualized net operating income from October 2026 to September 2036, climbing to roughly $754 million by 2035. Capital providers are voting with their wallets: the Black Pearl bond was 6.5x oversubscribed with about $13 billion in orders.

CEO Tyler Page framed the setup bluntly on the Q4 2025 call: “2026 is a year of execution for Cipher as we fully transition the business into a leading infrastructure platform.” Beyond the two anchor leases, the company is sitting on a 3.4 gigawatt development pipeline, including Stingray, Ulysses, and Reveille, all targeting energization between 2026 and 2028.

The key risk is the near-term income statement. Q4 2025 revenue of $59.71 million missed the $85.46 million consensus by 30.13%, and the company posted a GAAP net loss of $734.20 million, swollen by a $410.27 million warrant liability swing and $96.06 million in losses on miners held for sale. Total liabilities ballooned to $3.46 billion from $173 million a year earlier, and rent does not commence until October 2026, leaving roughly two more quarters of ugly headline numbers. Tenant concentration in AWS and Google/Fluidstack adds execution risk.

Even with those caveats, paying under $20 for a company with multi-gigawatt pipelines and long-term power agreements directly with hyperscalers looks like a credible backdoor on the AI buildout without paying software multiples.

Cipher Digital’s contracted cash flows, oversubscribed bond demand, and 3.4 GW pipeline make the under-$30 entry point interesting, but the GAAP losses, debt load, and construction timelines are real. Investors should pair this with their own diligence on the October 2026 energization milestones before sizing any position.

Contact [email protected] for any questions or corrections.