Megacap tech is wobbling, and money is looking for somewhere cheaper to land. With NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) pushing eye-watering multiples and software names trading like the AI build-out is already finished, the smarter rotation is happening one layer down the stack: the physical power and data center capacity that every hyperscaler is fighting over. Stocks under $30 that own that bottleneck are suddenly the most interesting trade in the room, because they offer real contracted cash flow at a fraction of the price tag of the chip kings.

With that backdrop, here is one stock trading under $30 that fits the institutional rotation into picks-and-shovels AI infrastructure.

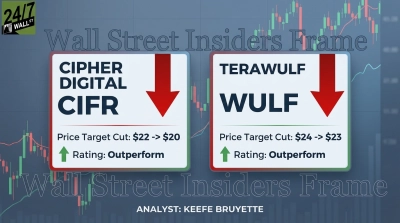

Cipher Mining (NASDAQ: CIFR)

Cipher Mining (NASDAQ:CIFR), now operating as Cipher Digital, develops industrial-scale data centers leased to hyperscalers for high-performance computing workloads, after pivoting away from its bitcoin mining roots.

Shares closed at $23.02 on May 26, 2026, comfortably under the $30 ceiling and up 55.96% year to date and 563.4% over the past year. For a retail investor, that is still a sub-$25 entry into a company with a $9.4 billion market cap and roughly 409 million shares outstanding, which is rare in pure-play AI infrastructure.

The fundamentals tell a transition story. Q4 2025 revenue came in at $59.71 million, missing the $85.46 million consensus but still rising 41.4% year over year, with adjusted EPS of -$0.14. Full year 2025 EPS landed at -$2.15, swollen by a $410.27 million warrant liability swing. Wall Street is looking past the noise: the average analyst target sits at $30.53, with 5 strong buys and 9 buys and zero sell ratings, while forward earnings carry a 85x multiple.

The bull case is straightforward. Cipher has roughly $11.4 billion in contracted revenue across three signed data center campus leases, anchored by a 15-year, 300 MW deal with Amazon Web Services at Black Pearl and a 10-year, 300 MW lease with Fluidstack and Google at Barber Lake. Management expects $787 million in average annualized net operating income once the leases turn on, with both sites targeting October 2026 energization. Behind that sits a 3.3 gigawatt development pipeline and $3.73 billion of completed bond financing, including a Black Pearl offering that was 6.5x oversubscribed. CEO Tyler Page framed it bluntly on the Q1 call: “We are no longer an aspirational HPC developer. We are a company with signed contracts, billions of capital raised, and multiple data center construction projects progressing toward completion.”

The risks are real. Total liabilities ballooned to $3.46 billion from bond financings, the accumulated deficit hit $1.0 billion, and debt to equity stands at 3.44. Tenant concentration is heavy on AWS and Google, and the Odessa mining PPA expires in July 2027. Insider activity has also been one-directional: CEO Page sold 400,000 shares on May 12, and COO Patrick Kelly sold 48,000 shares at $19.36 the same day. That said, institutional flows have moved the other way, with Vanguard lifting its stake by 43.2% in Q4 to over 32.6 million shares. None of this kills the thesis, but it does argue for sizing positions thoughtfully.

For investors hunting a discounted entry into the power-and-data-center layer of AI rather than overpaying for chips or software, Cipher looks like one of the cleanest under-$30 pure plays available.

Share price under $30 is never, on its own, a reason to buy anything. Cipher carries real construction execution risk, heavy leverage, and a still-raw transition from miner to landlord. Do your own work, read the filings, and weigh the contracted cash flow story against the balance sheet before deciding whether the rotation thesis fits your portfolio.

Contact [email protected] for any questions or corrections.