The AI buildout has a power problem. Hyperscalers are racing to deploy GPUs, but the U.S. grid is short on megawatts, and operators with energized land and signed interconnect agreements have become the chokepoint nobody wants to talk about. The Energy Information Administration’s latest outlook flags data center growth concentrated in the West South Central region (Texas) as a primary driver of commercial electricity demand, and the industry consensus is that the U.S. needs 50+ gigawatts of additional electric capacity for AI by 2028. Stocks under $30 with direct exposure to that gap are worth a hard look right now.

With that in mind, here is one stock trading under $30 that analysts believe is positioned to capitalize on the looming power shortage, even as most AI investors keep chasing the obvious chip names.

Cipher Digital (NASDAQ:CIFR)

Cipher Digital (NASDAQ:CIFR), recently rebranded from Cipher Mining, is a former bitcoin miner that has pivoted into a developer and operator of high-performance computing data centers powering hyperscaler AI workloads.

Shares closed at $24.59 on May 28, 2026, just under the recent 52-week high of $25.56. For a retail investor, that price tag still buys exposure to a company with a $10.07 billion market cap and a backlog that dwarfs current revenue. The stock is up 66.6% year to date and 634% over the past year, yet Reddit chatter remains concentrated in a single r/wallstreetbets thread with consistently “low” activity. That is the textbook definition of overlooked.

Fundamentals are messy on the surface and powerful underneath. Cipher booked Q4 2025 revenue of $59.71 million, missing the $85.46 million consensus by 30.13%, and reported a GAAP net loss of $734.2 million driven largely by a $410.27 million non-cash warrant liability swing. Adjusted EPS came in at -$0.14. The real story sits in the contract book: a 15-year, 300 MW lease with Amazon Web Services at Black Pearl worth roughly $5.5 billion at a ~100% NOI margin, plus a 10-year, 300 MW Fluidstack lease backstopped by Google at Barber Lake worth roughly $3.8 billion. Combined, that is $9.3 billion in contracted HPC revenue and ~$669 million in average annualized NOI.

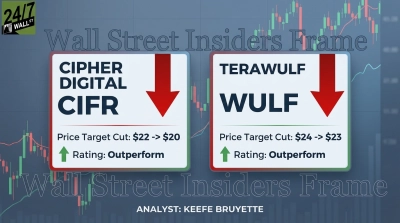

Wall Street has noticed. The analyst consensus target sits at $30.53, with 14 buy or strong-buy ratings and zero sells. Morgan Stanley carries a $40.50 target, Jefferies upgraded to strong-buy, and Keefe, Bruyette & Woods raised to $27 with an outperform rating.

The bull case is straightforward. Both Black Pearl and Barber Lake are targeting October 2026 energization, flipping Cipher from a cash-burning developer into a contracted-revenue infrastructure operator almost overnight. Behind those two sites sits a 3.2 GW pipeline across six additional projects, and bond offerings funding construction were roughly 6.5x oversubscribed, a clear signal that credit markets believe the lease economics. CEO Tyler Page told investors “2026 is a year of execution for Cipher as we fully transition the business into a leading infrastructure platform”.

The risk that cuts against the thesis: leverage and concentration. Total liabilities ballooned to $3.46 billion from $173 million a year earlier on high-yield bond issuance, the accumulated deficit hit $1.0 billion, and revenue depends on two tenants. Any construction slip at Black Pearl or Barber Lake hits the stock hard. Insider activity is also mixed, with the CEO and COO consistently disposing of shares from March through May 2026.

Even so, with $9.3 billion in contracted revenue against a $10 billion market cap and energization months away, Cipher Digital is one of the cleanest sub-$30 ways to play the AI power gap.

A low share price alone is never a reason to buy or avoid a stock. Cipher carries real execution risk, heavy debt, and a balance sheet that can swing violently on non-cash charges. Do your own research, weigh the dilution and tenant-concentration risks against the contracted backlog, and size any position accordingly.

Contact [email protected] for any questions or corrections.