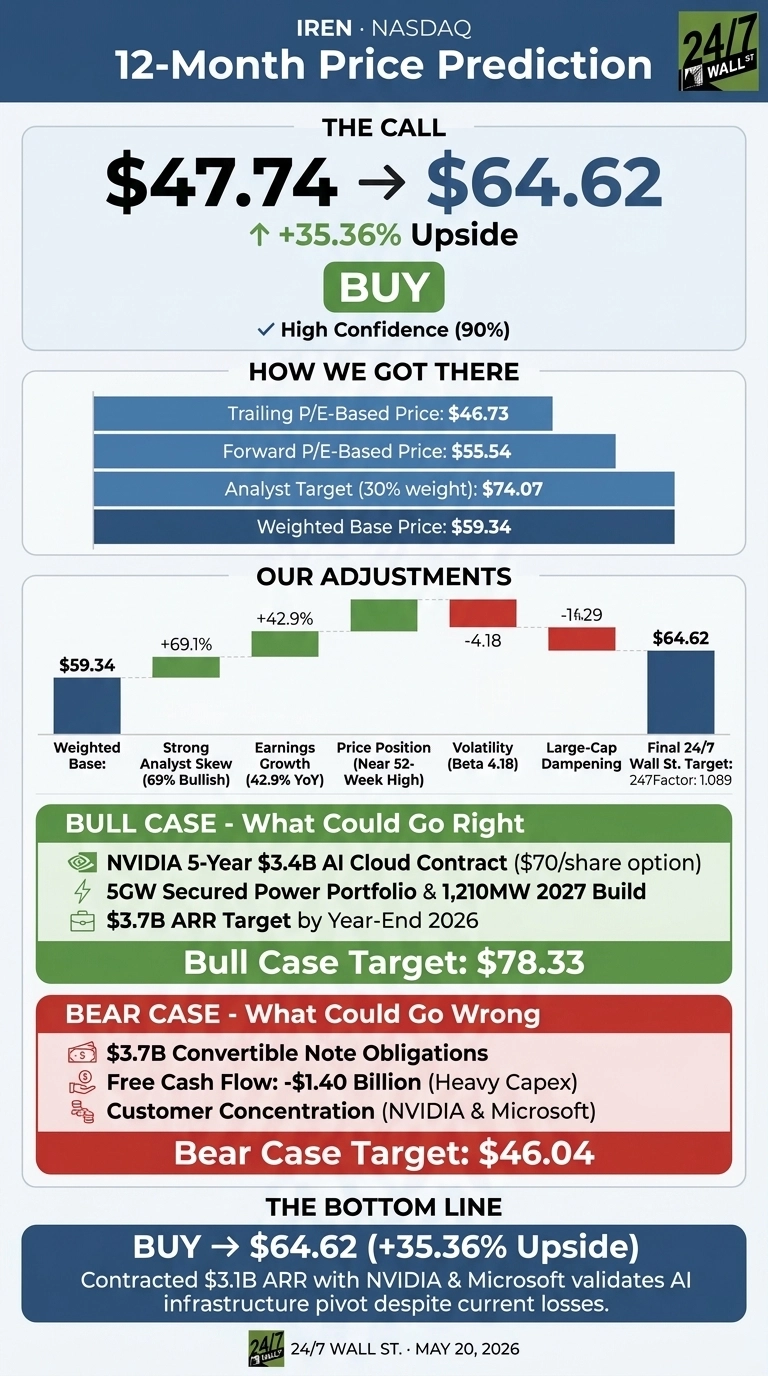

Our IREN (NASDAQ:IREN) call is constructive. Shares closed at $47.74 on May 19, 2026, well off the post-earnings high near $60.80 but still up 459% over the past year. Our 24/7 Wall St. price target for IREN is $64.62, implying 35.36% upside over the next 12 months. Our model carries a constructive rating on IREN with high (90%) confidence.

| Metric | Value |

|---|---|

| Current Price | $47.74 |

| 24/7 Wall St. Price Target | $64.62 |

| Upside | 35.36% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Rough Stretch Masks a Bigger Story

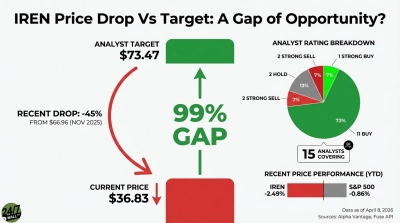

IREN has been violent in both directions. Shares fell 15.59% over the past week and dropped 5.39% on May 19 alone, yet IREN remains up 26.4% year to date. The 52-week range of $8.28 to $76.87 tells the story of a stock repriced by the AI infrastructure narrative.

Q3 FY26 revenue of $144.80 million missed the $219.29 million consensus, and IREN booked a $247.80 million net loss largely from $140.40 million in impairments on decommissioned mining hardware.

The real signal lies underneath: AI Cloud Services revenue jumped to $33.60 million, nearly doubling sequentially from $17.30 million, while IREN locked in a 5-year, $3.40 billion AI Cloud contract with NVIDIA on top of the $9.70 billion Microsoft deal.

Why Bulls See a Breakout Ahead

The bull setup is tangible. IREN guides to $3.70 billion in ARR by year-end 2026, with $3.10 billion already under contract. The NVIDIA partnership includes rights to purchase 30 million IREN shares at $70, a potential $2.1 billion equity injection.

CEO Daniel Roberts said the deal “further validates IREN’s key role in the AI infrastructure ecosystem.” With 1,210MW in build for 2027 and a 5GW secured power portfolio, the consensus Street target of $74.07 looks reachable. Our bull-case path runs to $78.33, or 64% upside.

The Risks Worth Watching

Two consecutive revenue misses matter. Q3 came in 33.97% below consensus, and free cash flow ran to negative $1.40 billion. Convertible notes payable sit at $3.69 billion, and a chunk of the ARR target remains uncontracted.

Bulls would argue the headline loss reflects one-time impairments tied to retiring ASIC mining gear, and that adjusted EBITDA margin of 41% supports the transition narrative. Customer concentration in Microsoft and NVIDIA, plus ERCOT interconnection risk in Texas, keeps execution central. Our bear-case path lands at $46.04.

The Bottom Line

The 24/7 Wall St. price target is $64.62, with a buy rating and 90% confidence. The deciding factor is contracted demand: $3.10 billion in ARR backed by NVIDIA and Microsoft is too large to ignore at a $16.7 billion market cap.

The constructive case strengthens if AI Cloud revenue continues to roughly double sequentially through fiscal 2027. The thesis weakens if Sweetwater or Childress timelines slip, or if convertible refinancing terms harden.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $64.62 |

| 2027 | $66.24 |

| 2028 | $83.28 |

| 2029 | $93.62 |

| 2030 | $99.49 |

These projections assume IREN executes on the NVIDIA ramp beginning in early 2027 and converts the remaining uncontracted ARR. Material upside or downside hinges on power delivery at Sweetwater and Childress.

Contact [email protected] for any questions or corrections.