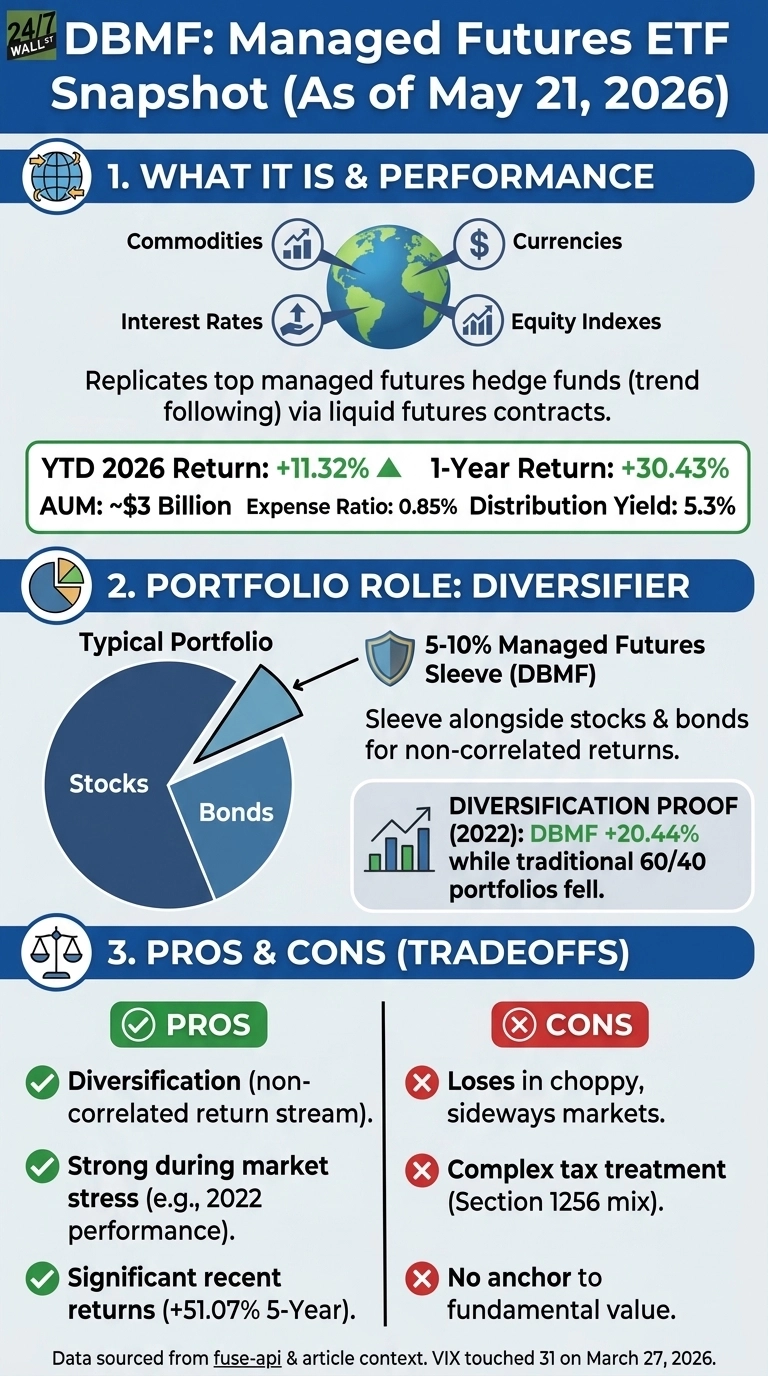

For retirees who watched bonds fail to cushion equity losses in 2022, the iMGP DBi Managed Futures Strategy ETF (NYSEARCA:DBMF) has changed the conversation by gathering roughly $3 billion in assets and delivering what the 60/40 portfolio failed to deliver then and is again outpacing in 2026: a return stream that does not move in lockstep with stocks and bonds. Managed futures funds spent most of the 2010s as an academic curiosity, a category retirees were told about and rarely bought. DBMF is up 11% year to date, while a 60/40 mix of the S&P 500 and the U.S. Aggregate Bond Index has returned roughly 5%, based on SPY at 9% and AGG at 0%.

What DBMF Actually Owns

DBMF is designed to replicate the pre-fee performance of the largest managed futures hedge funds by taking long or short positions in 10 to 15 highly liquid futures contracts across commodities, interest rates, currencies, and equity indexes. The fund reverse-engineers the average exposures of the CTA hedge fund universe, then expresses them via cheap, liquid futures rather than paying the 2-and-20 fee structure underneath. The return engine is trend following. When the dollar rallies for months, the fund is long dollars. When crude oil grinds lower, it is short crude. The strategy makes money when markets move in sustained directions and loses money when they chop sideways.

The fund charges an expense ratio of 0.85% and pays a distribution yield of 5.2%, the latter sourced largely from Treasury collateral backing the futures positions rather than from the trading strategy itself.

Testing the Diversification Claim

The core rationale for holding this unique strategy stems from its performance throughout 2022, when traditional equities and investment-grade fixed income collapsed simultaneously for the first time in modern financial history. DBMF delivered a stellar 21.5% total return during 2022, whereas standard balanced asset portfolios suffered catastrophic, double-digit losses. That specific market cycle effectively pushed managed futures strategies back onto the radar for income-focused retirees who had falsely assumed that conventional bonds would permanently insulate them from equity drawdowns.

Current performance metrics strongly reinforce the need to diversify the thesis. DBMF has gained 30% over the trailing twelve months and 51.4% over a five-year horizon, a multi-year window during which the passive bond benchmark AGG generated virtually flat performance. The VIX aggressively touched 31.21 on March 27 during a sudden liquidity shock that managed futures algorithms were perfectly formatted to exploit. DBMF is not engineered to outpace pure equity indexing over time; SPY surged 91.0% over that five-year stretch compared to DBMF’s 51.1% advance. Ultimately, this alternative structure is optimized to serve as an uncorrelated portfolio stabilizer alongside core equities.

DBMF vs. KMLM and the Tradeoffs

Its closest peer is the KFA Mount Lucas Managed Futures Index Strategy ETF (NYSEARCA:KMLM), which follows a rules-based index across 22 futures markets rather than mimicking hedge fund positioning. KMLM has returned 13% year to date and 16% over the past year, narrowly leading DBMF in 2026 but trailing materially over 12 months. The two funds often diverge by 5 to 10 percentage points in a given year because their methodologies weight markets differently.

Three constraints are worth naming. Trend following loses money in choppy, range-bound markets, and DBMF can post negative years even when stocks rise. Distributions are taxed as a mix of ordinary income and 60/40 capital gains under Section 1256, which complicates tax planning. And the strategy has no anchor to fundamental value, meaning past performance offers little signal about the next 12 months.

Where It Fits

DBMF functions best as a 5% to 10% portfolio satellite alongside a traditional mix of equities and fixed income, calibrated to inject meaningful diversification without entirely dictating overall performance outcomes. A 65-year-old retiree managing a $1 million nest egg split 60/40 could cleanly carve out $50,000 to $100,000 for alternative trend-following strategies while fully accepting that the position will likely drift during flat, range-bound macro environments. Allocators anticipating capital appreciation that moves in lockstep with the S&P 500, or a predictable monthly income stream mirroring a traditional bond portfolio, should strictly focus their capital elsewhere.

Contact [email protected] for any questions or corrections.