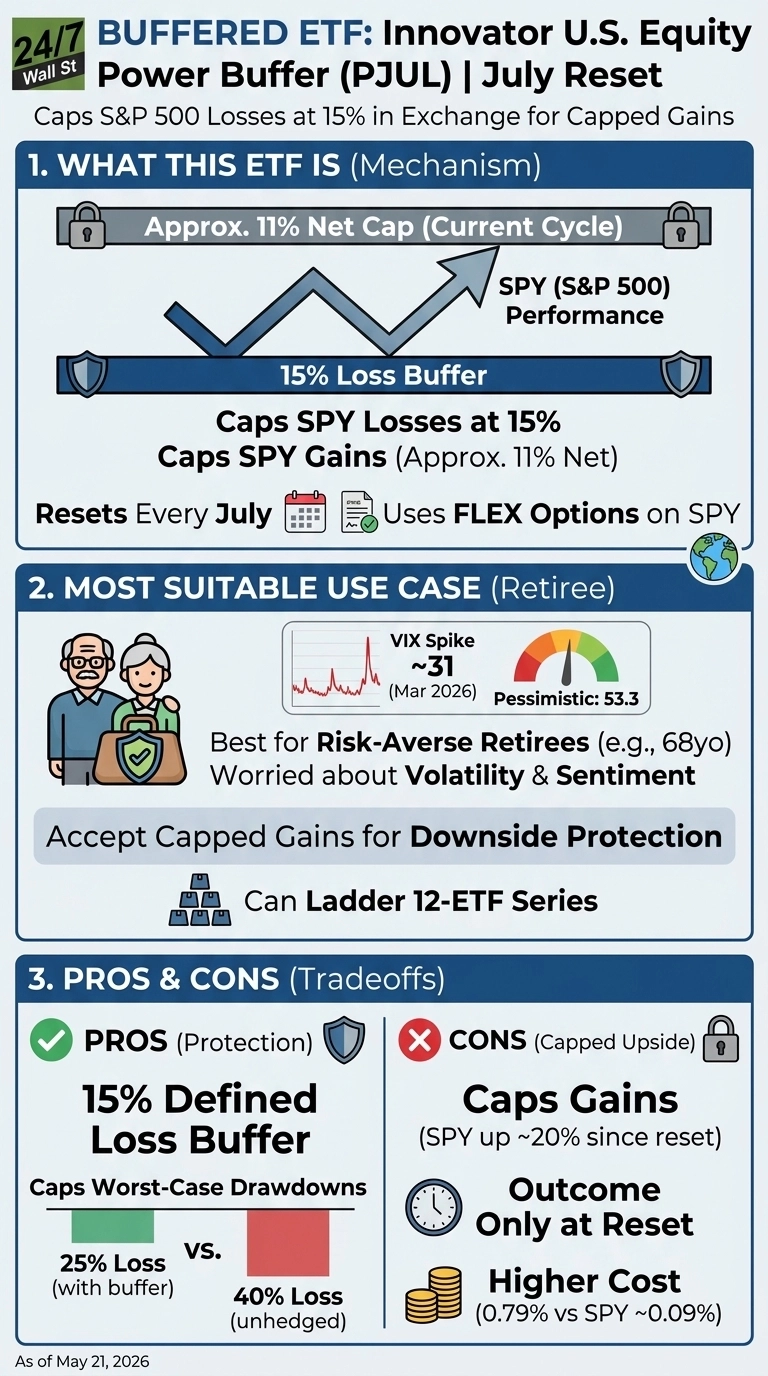

A 68-year-old retiree with $400,000 in equities heading into 2026 has a real problem: SPY ran up 27% in the past year, but the VIX still spiked to almost 31 in late March, and the University of Michigan consumer sentiment sits at 53.3, deep in pessimistic territory. The Innovator U.S. Equity Power Buffer ETF, July Series (PJUL) is built for exactly that investor. PJUL tracks SPDR S&P 500 ETF Trust (NYSEARCA:SPY) upside to a cap and absorbs the first 15% of any loss across a 12-month outcome period that resets every July.

How the buffer is actually built

PJUL holds a customized basket of FLEX options on SPY, engineered to deliver a well-defined payoff matrix. Long call options establish the baseline upside participation, short call positions finance the insurance ceiling, and an out-of-the-money put spread constructs the core 15% protection buffer. This mathematical strategy only delivers its intended objective if an investor holds shares from one specific July reset period straight through to the next. Purchasing shares mid-cycle means paying a premium for a buffer that may have been partially exhausted; liquidating prematurely forces you to accept whatever those options are priced at that afternoon, rather than the advertised outcome.

For the active performance block running from July 1, 2025 through June 30, 2026, Innovator locked the hard upside cap at precisely 12.09% gross, which drops to 11.30% net when accounting for the 0.79% expense ratio. The initial 15% cushion against SPY losses remains the lone operational constant; the maximum return ceiling resets every July based on prevailing equity options pricing.

Does the math work this cycle?

SPY has surged roughly 21.2% since its previous July reset date. An early PJUL allocator who entered at that inception point captured the full 11.3% net cap but watched the unhedged index sprint nearly 10 percentage points further down the track without them. On a $200,000 core portfolio allocation, that lagging trajectory represents nearly $19,800 of surrendered upside during a single outcome cycle.

The inverse performance path illustrates the exact worst-case scenario that anxious retirees are actively trying to avoid. During a severe 40% correction across the broad S&P 500, an unprotected $200,000 equity stake plummets directly to $120,000. Conversely, the structural 15% buffer insulates principal by capping losses at 25%, preserving that exact same retirement position at roughly $150,000. The underlying insurance architecture is executing its defensive mandate perfectly; its opportunity cost simply looks elevated today because the market violently breached the cap.

Tradeoffs the fact sheet softens

- Cap risk in strong markets. The 2025 to 2026 cycle is the textbook example. SPY closed at about $741.25 on May 21, 2026, well past the cap level. Any further upside in SPY through June 30 belongs to options counterparties, not PJUL shareholders.

- Holding period rigidity. The defined outcome only exists at the reset endpoint. Mid-period NAV swings can look nothing like the published cap and buffer, which trips up investors who treat PJUL as a tactical trade.

- Cost stack versus alternatives. PJUL charges 0.79% versus SPY at about 9 basis points. The 10-year Treasury at 4.6% offers a different form of downside protection with no equity exposure at all.

Where it fits and where it does not

Innovator runs a 12 ETF series, one for each calendar month, which lets an investor ladder entries so that one tranche resets every 30 days and the portfolio is never fully exposed to a single outcome window. That is the structurally sound way to use the product family.

PJUL fits a retiree who has already decided that giving up roughly half of a bull market is an acceptable price for capping the worst case at a 25% equity loss instead of a 40% one. It does not fit an investor who still needs portfolio growth to fund a long retirement, who can tolerate equity volatility, or who would be equally comfortable with a USMV low-volatility allocation paired with intermediate Treasuries yielding 4.57%. The buffer is real, and so is the cap, and this year that cap has a clear dollar cost.

Contact [email protected] for any questions or corrections.