Webull (NASDAQ:BULL | BULL Price Prediction) posts blistering top-line growth while its stock sits in the bargain bin.

Q1 2026 revenue jumped 36% YoY to $159.93 million, customer assets ballooned 90% to $24 billion, and equity notional volume more than doubled to $261 billion. Yet shares are down 19.43% YTD and trade at just $6.26. Can this active-trader platform reach $25 per share by 2030?

Why Webull Shares Are Stuck Despite Booming Growth

The market is punishing Webull for the cost of growth. Operating expenses surged 68% YoY against revenue growth of 36%, marketing more than doubled to $49.41 million, and the company swung to a $21.72 million GAAP net loss from a profit a year earlier.

Adjusted operating profit fell to $14.82 million from $28.66 million. The stock is down 10.57% in the past week, 9.28% over the past month, and 49.11% over the past year. Add PFOF regulatory overhangs and China-related government inquiries, and you have a stock that, despite a beta of just 0.604, is bleeding for specific fundamental reasons.

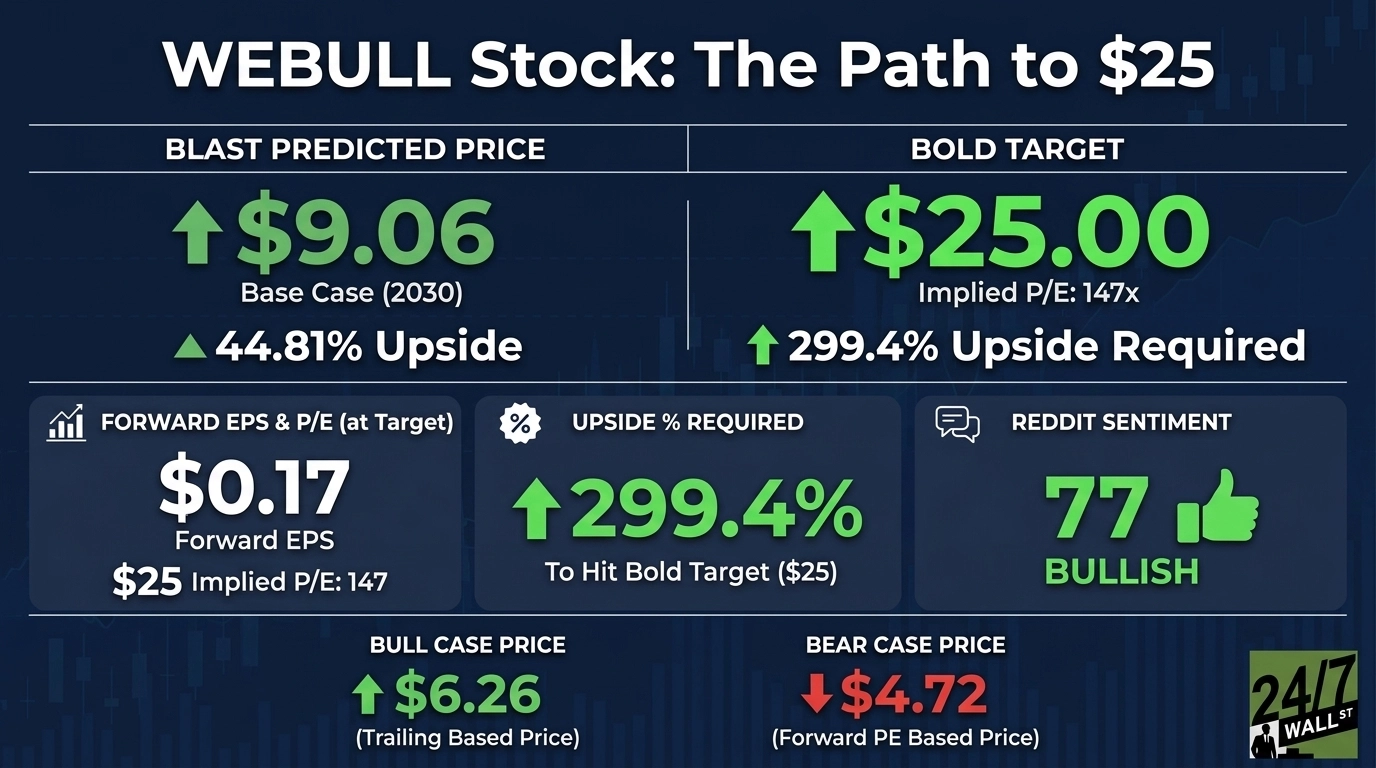

Wall Street Sees 91% Upside. Our Model Says 44%

The consensus target sits at $12, with 3 buys, zero holds, and zero sells. That implies roughly 91.69% upside from today. Our internal model is more measured: a base case of $9.06, representing 44.81% upside with a 90% confidence score and a buy rating.

Our optimistic 1-year scenario reaches $20.15; the 5-year bull case stretches to $109.69. With three analysts at 100% bullish and Webull printing revenue growth above 35%, the Street is closer to right than our base case, but neither has fully priced international optionality.

The Path to $25 Per Share

Reaching $25 from today’s price of $6.26 requires a gain of 299.4%. With forward EPS of $0.17, a price of $25 implies a forward P/E of 147. Our base case of $9.06 already implies 39x, meaning the bold target requires 108x of additional multiple expansion on today’s earnings power.

The realistic path is EPS growth that collapses that multiple. Our 247Factor adjustment of 1.257 reflects 100% bullish analyst consensus, a 1.15x technology sector multiplier, and low-volatility beta.

CEO Anthony Denier said in Q1 he is “proud to report a strong start to our second year as a public company” with “meaningful progress” on the Vega Analyst AI tool and license coverage across the entire European Economic Area.

Three catalysts can compound earnings: the FINRA PDT rule change on June 4, 2026 unlocking active trading, the $24 billion customer asset base driving interest income, and institutional flow already at 9.5% of equity notional volume. Primary risk: a PFOF crackdown would cripple the $84.39 million order flow rebate engine overnight.

Where Webull Trades Today vs Its Earnings Power

At $6.26, BULL trades at a forward P/E of 37x against forward EPS of $0.17. Alpha Vantage pegs the forward multiple at 28x on a slightly different estimate. Either way, shares sit 34% below the 52-week high of $18.32 and only modestly above the $4.50 low. For a business compounding revenue near 46% annually on a $3.29 billion market cap, that is depressed, not expensive.

$25 Is a Stretch, But Here’s Why It’s Possible

$25 by 2030 demands a 299.4% gain from today. That is a stretch.

To get there, Webull needs three things: EPS scaling toward $0.50+ through international and B2B leverage, the PFOF model surviving regulatory scrutiny intact, and operating discipline returning so expense growth no longer doubles revenue growth. A serious PFOF rule change would derail the entire thesis. We’ve outlined the blueprint for how Webull could reach $25 in 2030.

Contact [email protected] for any questions or corrections.